2026

There is nothing more powerful than that of an idea whose time has come.

Coming in 2026, the crypto pendulum has swung firmly in the bulls’ favour. Crypto is hated, dismissed, and back to being a contrarian asset class filled with uncertainty. Prices, of course, continue to dictate sentiment, swinging opinion from ‘revolutionary technology’ to ‘nothing burger’. Humans gonna human.

I have been in this exact spot at least ten times before over my nine years in crypto, the whatsapp messages quickly transition from “what should I buy” to “I told you it was all nonsense”, “I guess digital gold didn’t get the memo” and my personal favourite “I have written it off, buying some gold now”.

This is how great opportunities emerge. Forward-looking expectations for cryptoassets are low, arguably lower than during the bust of ICOs, COVID, the collapse of Luna Terra, and the fraud of FTX.

With depressed prices, we have every possible dimension of fear, uncertainty and doubt, the same regurgitated narratives that appear every time reality falls short of near-term inflated expectations. “Quantum will kill crypto”, “Corporate Chains are going to eat crypto’s lunch”, “the technology can’t scale”, “whales are abandoning crypto”, “we are going back to a gold standard not a digital standard”, “regulators will never pass pro-crypto laws”, and “institutions will capture and tame crypto”.

But for anyone with the ability to zoom out and incorporate the larger picture of how crypto fits into the world, the conclusion that you will reach is that crypto’s future is bright, brighter than it has ever been. The industry is finally growing up and in its adult years, I expect that it will defy even the loftiest of expectations.

The foundations of the new financial rails have been laid, the predictions of the past are coming to fruition, the challenges are well established, and cryptoassets are increasingly integrated as a key portfolio component.

Let’s dive into some charts!

Bitcoin and the four-year cycle

The four-year cycle consensus is that price is set to break down further, and the pattern observed in 2022 is to be repeated throughout 2026.

To negate the 4-year cycle consensus, there are some key levels that need to be taken out, primarily the short-term realised price (the cost basis of short-term holders) of $98k . On the 14th of January, we tagged that level but failed to break through.

I disagree with this consensus view, as 2022 was a completely different macro environment and crypto has matured significantly.

Central bank balance sheets were peaking after a multi-year expansion. In 2026, they are bottoming out after a multi-year contraction.

We were also at a very different stage of the business cycle, as shown by ISM purchasing managers index (PMI) and the copper-to-gold ratio.

Business cycle slowdowns appear to be where risks of long and protracted drawdowns are most amplified, especially when preceded by a blow-off in crypto prices. The environment today is different from that of 2022, as seen in the contrasting Copper-to-Gold ratio and BTC.

Leading indicators of the business cycle are pointing toward expansion. Again suggesting the business cycle is going to accelerate, not slow down as it did in 2022.

Our crypto conditions index (CCI) is back in expansion suggesting supportive conditions. CCI has been in expansion since the 6th of December 2025.

CCI is a composite measure of broad liquidity, growth sentiment and credit risk.

A full historical view of the composite.

CCI also confirms that we are in a different macro environment than that of 2022.

Today.

One thing making investors uneasy and supporting the four-cycle theory is Bitcoin’s poor price performance compared to US equities and Gold. It appears that the 10/10 liquidation event in 2025 was a turning point.

Interestingly, prior bull runs were all preceded by sharp moves up in gold, once gold formed a top, bitcoin began to move higher. The same “bitcoin is dead” chants were heard from June 2020 through to October 2020. I have mapped QT and QE announcements for added context.

Bitcoin has been in a bear market relative to gold for a similar duration as previous bear markets.

This chart from Bitwise illustrates BTC/GOLD over time against its “liquidity fair value”, a regression-based estimate derived from global money supply growth. Showing that coming into 2026, BTC is trading at extremes relative to Gold and its relationship with global liquidity.

The Bitcoin/SP500 ratio is also at extremes.

BTC vs the equally weighted S&P 500 is retesting 2021 highs.

Ethereum

Ethereum, the network, is going from strength to strength as outlined in Chain Street (Part 1).

Ethereum is scaling with increasing activity.

Investors continue to incorrectly analyse Ethereum as a company. Putting something new in a familiar but inappropriate bucket. Here is my framework:

Ethereum is not a company.

ETH is not a share of the Ethereum network.

ETH is the collateral and payment token of the Ethereum network.

ETH has a fixed maximum issuance cap of 1.5%, which is a lower, more predictable inflation rate than fiat and gold. In times of high activity, issuance can turn negative. I explored this in detail in Time for ETH.

If ETH is anything that our words can describe, it is a commodity, or a form of money, essential to the security and functioning of the Ethereum network, including its universe of layer 2 blockchains.

Ethereum differs from open networks and systems of the past because its security as an infrastructure is directly linked to the value of ETH. ETHs $ Value and the percentage of ETH staked determine the cost to corrupt the Ethereum network.

For these reasons, we continue to hold the view that the success of the Ethereum network is tied to the ETH price. Higher prices signal more security, lower prices signal less security.

Historically, ETH has found a floor price at or near the value it secures in smart contracts, total value locked. This validates our thesis on ETH, albeit with a small sample size. Recent lows of $2630 once again bounced off the value ETH secures.

We are constructive on ETHBTC and view this pullback as a correction within a potentially larger move.

How ETHBTC resolves will be vital in determining whether we get a broadening out in crypto.

The Race to Bring the World Onchain has Begun, and Ethereum is the Clear Leader.

Ethereum leads in Stablecoins.

Ethereum leads in Tokenised Funds.

Ethereum leads in Tokenised Commodities.

Ethereum ($161m) lags slightly behind Solana ($170) in Tokenised Equities.

Although growth in bringing real-world assets onchain is strong, for it to really kick into high gear and ignite the mass token generation event I discussed in Adulthood and Underpants, we need to see the CLARITY Act pass.

Decentralised Finance

The applications of Chain Street are ready for prime time, but headwinds remain.

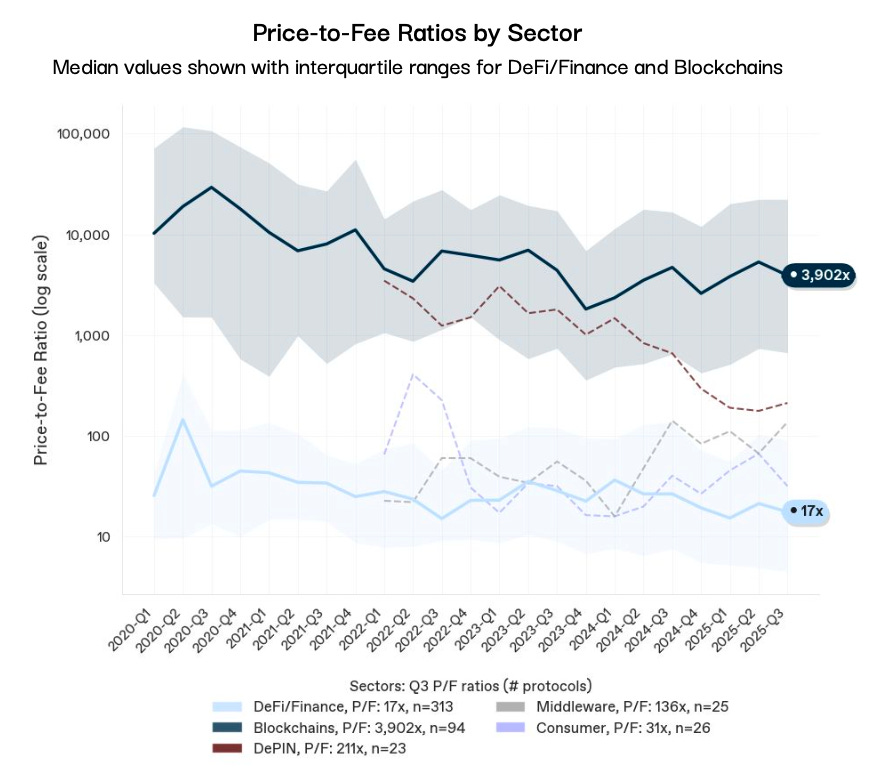

The biggest headwind is the confidence crisis in a protocol’s ability to return value to tokenholders. I have discussed this at length in Chain Street (Part 2). I am comforted that industry-leading protocols like Uniswap and Aave are tackling this problem head-on and remain constructive on token holder rights being top of mind in 2026.

The economics of blockchains are shifting value capture up the stack. As they should.

Since the peak of “dot-crypto”, price to fees of leading DeFi protocols have compressed to compelling valuations. Although we must temper these compelling multiples with the ongoing tokenholder confidence crisis. The median price to fees of DeFi protocols as a category have gone from over 100x to just 17x today.

As a subsector of the crypto investable universe, I think DeFi offers the most compelling opportunity. DeFi protocols now account 61% of onchain fees but only 6% of market capitalisation. A rerating is likely if the four-year cycle is indeed dead, ETHBTC continues to trend higher, and the tokenholder confidence crisis makes progress.

Moonshots in Crypto and AI crossover

I am, as I am sure many of you are, blown away by the progress being made in AI.

It seems like we are truly in the exponential age.

So my moonshots for 2026, the potential 10-100x baggers, are in the AI and blockchain crossover. In 2024, this sector of the crypto economy came to life but faltered in 2025.

The big picture idea is that we are in an industrial revolution powered by AI. I think there is going to be massive opportunities from resource markets for data, compute, bandwidth and storage to buying skilled agents and owning agent marketplaces.

I’m still trying to get my head around the opportunities in this category and will be sharing them over the course of the year in our Moonshots section (Coming soon).

Concluding Thoughts

If I took you back to the start of 2025 and showed you 12 months in advance all the news events and macro data, you still wouldn’t have made money in crypto. Relying on the four-year cycle would have been catastrophic, as the blow off top was nowhere to be seen. Going into 2026, I can’t say for sure how the year will shape up.

What I do know is that the conditions in early 2026 look starkly different from the bear markets of 2018 and 2022 and yes, that can shift quickly. We’ve moved from mania to maturity. Open public blockchains are advancing rapidly, scaling impressively while staying secure and decentralised. Real-world capital markets are coming onchain, bringing assets people actually care about and need, this will trigger massive adoption. Regulations are finally being drafted in ways that enable (rather than hinder) the deployment phase. And holding crypto in well-diversified portfolios is becoming mainstream rather than fringe.

There is nothing more powerful than that of an idea whose time has come.

While it’s easier to look away, seeking to understand is the only path to a more enlightened and empowered world. Change is now exponential and blockchain technology sits at the centre transforming money, finance and what it means to sovereign. Join me in exploring this new world by subscribing.

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments. Collective Investment Schemes (CIS) are generally medium to long term investments. The value of participatory interests may go down as well as up. Past performance, forecasts or commentary is not necessarily a guide to future performance. As neither Lima Capital LLC nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice.