The Great Divergence

It's becoming more clear to me that we are reaching the end of the dot crypto era. We are ebbing and flowing through the chasm as I write this, and nobody is bullish enough.

There is an enormous gap in sentiment between retail speculators and institutional builders. This is a fascinating data point: crypto bros are depressed, while institutions lick their lips at their emerging blockchain strategies.

This disconnect of retail disillusionment amidst institutional enthusiasm isn't random. It's the signal. Crypto is maturing.

What is retail missing?

Our previous memo, titled “The End of the Dot-Crypto Era”, argued that we’re shifting from overhyped, niche “ dot crypto” experiments to the widespread adoption of blockchain technologies. The thesis is that every company, at least in finance, will eventually become a “crypto company”. Look at the internet’s arc, once everyone plugged in, “internet company” turned into a redundant label, the same is happening to crypto right now.

We are stumbling into a multi-year secular trend where high-quality, productive assets come onchain. Financial institutions, from legacy giants to startups are beginning to explore financial products uniquely enabled by public blockchains and smart contracts.

This marks a shift from today's fragmented, permissioned financial infrastructure to a unified, permissionless infrastructure. The result? Lower transaction costs, fewer innovation barriers, and a surge in financial experimentation. This is the dawn of a productivity boom in finance, the Internet of Value is emerging, and much like the internet of information collapsed the cost of communication and knowledge, the internet of value is here to collapse the cost of financial services.

Some institutions understand this, but others will fall into the trap of appeasing outdated compliance departments by building on private, permissioned networks where traditional bankers become the new validators. These approaches are bound to fail. The biggest winners will build on open, permissionless rails, not the closed intranets of yesterday.

This view has nothing to do with crypto ideologies and everything to do with networks, networks are about social scalability and connectivity. Institutions leaning toward closed, permissioned networks will eventually wake up to the realisation that the real benefit is tapping into the enormous interconnected network of potential clients and liquidity.

A compelling survey from Paradigm and Allium sheds light on how institutions are approaching crypto today. You can read their full report here.

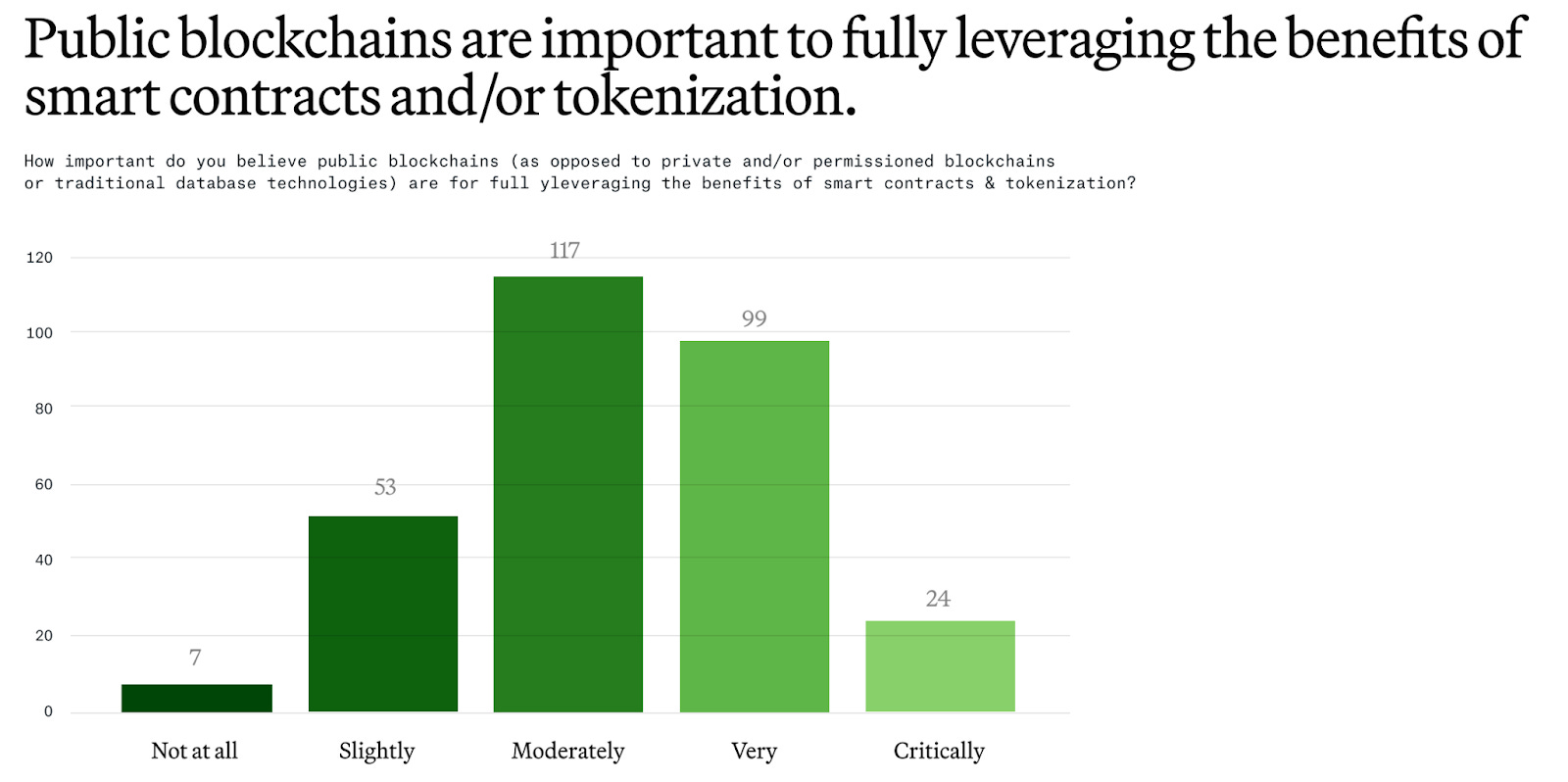

Institutions see faster settlement times, increased transparency and lower transaction costs as key benefits of decentralised finance.

Institutional excitement is high around the tokenisation of assets, stablecoins and decentralised exchange.

Institutional views on decentralisation vary, with some skepticism, yet most recognise public blockchains as critical for unlocking the full potential of smart contracts and tokenisation.

Institutions have been held back by a lack of regulatory clarity.

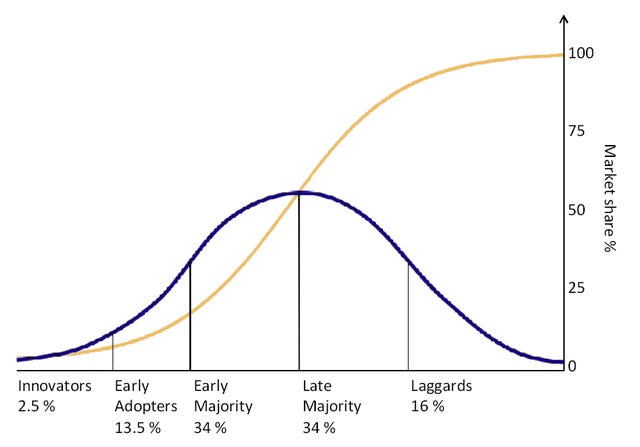

We are entering the parabolic phase of the crypto S curve, the innovators are in, the early adopters are in and the early majority are knocking on the door. Production capital is coming and it's coming fast. Regulation, the biggest headwind is slowly becoming a tailwind thanks to a crypto progressive US administration.

So far $246 billion in Real world assets are on chain. Today, these assets are limited to US dollar stablecoins, private credit funds and US treasuries.

US treasuries, stablecoins, and private credit funds serve as the natural entry points for onchain real-world assets. Yet, these are only the beginning. The potential market is vast, and we are merely scratching the surface of what’s possible. As the landscape evolves, we will see traditional asset classes such as equities, fixed income, structured products, mutual funds, private equity, and even real estate portfolios come onchain. Beyond these, a whole new array of financial instruments, currently beyond our imagination, is poised to emerge, ushering in an era of unprecedented experimentation and innovation.

Strangely, crypto markets have been mentally preparing us for this scenario. Anyone paying attention will acknowledge that crypto bull markets closely coincide with mass token generation events.

2017 brought the first example that most people would remember: the ICO boom. Back then, you needed BTC or ETH to purchase highly speculative tokens trying to leverage blockchain technology across industries from finance to supply chain management. BTC and ETH benefited enormously during this period, and most tokens were created on Ethereum.

Then came the 2020/2021 DeFi summer. Compound, a lending protocol, sparked a new bull run when it introduced the concept of liquidity mining or liquidity farming. Users could earn tokens simply by using the platform or supplying assets to liquidity pools. Once again, this wave primarily occurred on Ethereum.

Next was the 2021 NFT boom. Does anyone recall CryptoPunks or Bored Ape Yacht Club? Although short-lived, this craze was another mass token generation event, again dominated by Ethereum.

Finally, in 2023/2024, memecoin mania took over. After three mass token generation events on Ethereum, gas fees surged, discouraging many would-be participants and creating an anti-network effect. This pushed users to search for cheaper, more efficient platforms, and they converged on Solana. With a boost from pump.fun, Solana experienced an explosion in memecoin issuance.

All these mass token generation events have produced strong beta trades in crypto and propelled the venues for issuance to new highs. Bringing high-quality, productive assets on-chain will have a similar effect. More importantly, I expect this next wave to completely dwarf the test runs we saw in 2017, 2020/21, and 2023/24.

Market Conditions

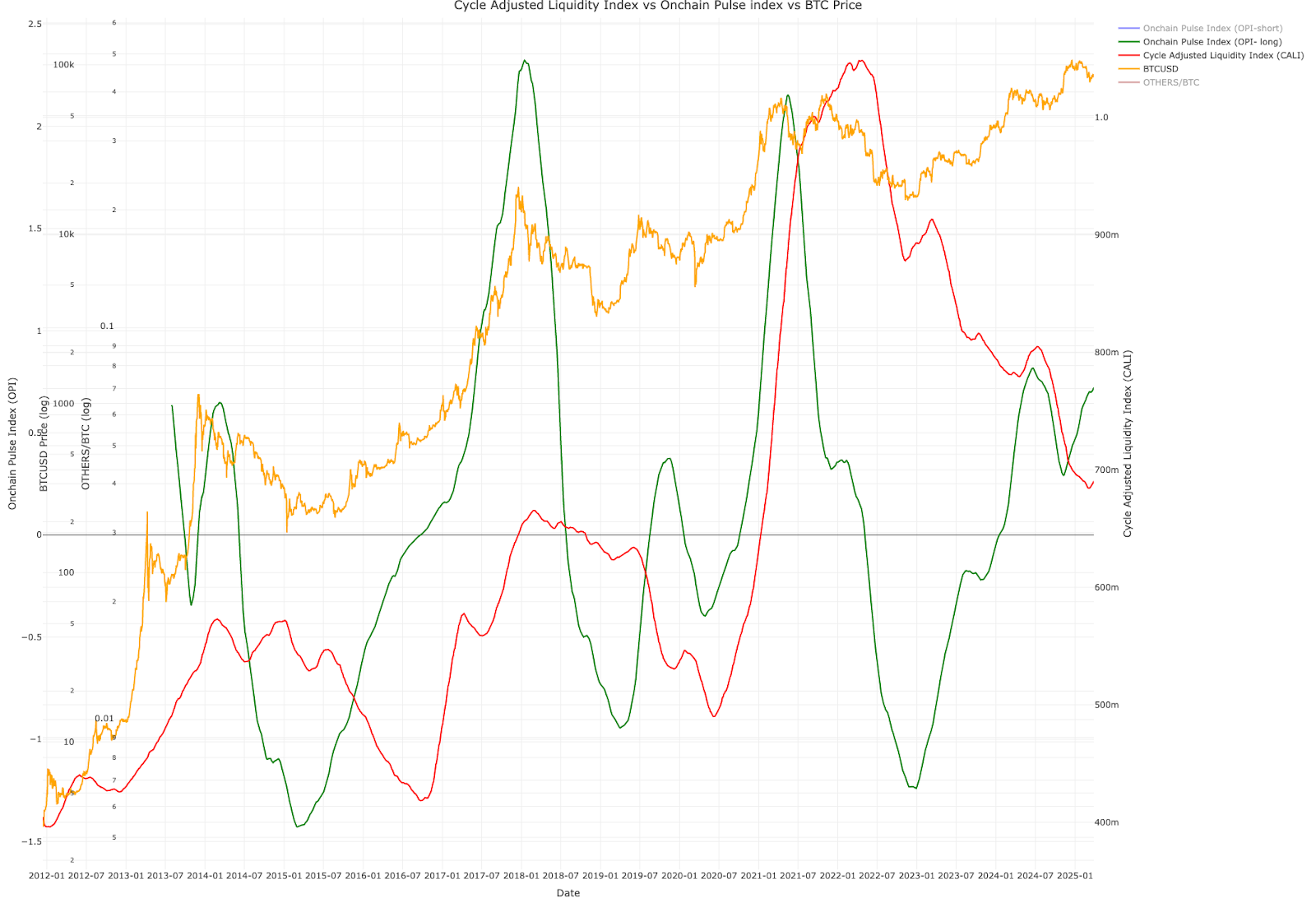

The picture for crypto over the next 12-18 months remains positive in our view, but economic conditions continue to weigh on crypto prices. Below we compare our Cycle Adjusted Liquidity Index (CALI) to our Onchain Pulse Index (OPI). A low CALI suggests low growth expectations and an economy starved for liquidity a high CALI suggests positive growth outlook and abundant liquidity. A low OPI suggests crypto is “cheap”, a high OPI suggests crypto is “expensive”.

This cycle has played out inline with historical bull and bear markets, the initial bottom was triggered by low in OPI (December 2022) but we still haven't seen the CALI bottom out, suggesting that poor growth outlooks and a lack of liquidity are holding back the second phase of the bull market. Previous expansions saw a combination of rising CALI and OPI, something we are yet to see this cycle.

Crypto isn’t exactly cheap here, but it's not grossly expensive either, when compared with historical market tops. Here is an equally weighted aggregate market value to realised value (MVRV) of the top 50 cryptoassets, currently holding at just above 1, suggesting that most cryptoassets are trading at or near their realised value.

We are certainly in the late stages of the bull market. Given the progressive movements on the regulatory front, I am confident that the market will give us attractive prices for selling in 2025 or 2026. But the timing of this has more to do with macroeconomic uncertainties and headwinds than anything crypto specific.

A lack of confidence doesn’t occur when bad things happen; it emerges in times of great uncertainty, we are in one of those times right now. America under Trump's leadership is pursuing an America first agenda, the stated goals of which is to revitalise American manufacturing, reduce trade deficits, and compel other nations to respect U.S. economic interests.

It will be interesting to see the markets reaction to announcements made on the 2nd of April, which the Trump admin is calling “Liberation Day”. The market desperately needs clarity on US trade policy and there's a good chance that with clarity some of the fears dominating the market will fade and positive sentiment could reemerge, this will translate to a bottom forming in CALI. This signal will give us conviction in the next phase of the cycle.

As always we remain focused on compounders, below is a snapshot of the top 10 crypto projects by network activity. Interestingly, Hyperliquid has taken the number 1 spot surpassing both Ethereum and Solana. Ryan Watkins from Syncracy Capital wrote a fantastic thesis for Hyperliquid that you can find here.

There’s a lot of concern around Ethereum and the voices of bears are growing daily. There are certainly reasons to be concerned about ETH. The most direct reason is its poor relative performance versus BTC, ETHBTC hit new lows in March of 0.022 and is down 74% in BTC terms since September of 2022. Additional worries stem from Ethereum's rollup-centric roadmap, which is siphoning fees to Layer 2 solutions, alongside a perceived lack of decisive leadership, further fuelling bearish sentiment.

I’m less worried about these concerns, for me the most concerning dynamic is the downtrend of Ethereum's share of network activity, since posting a high in June of 2018, Ethereum's network activity share has been down only. In defence of Ethereum the industry has grown significantly since 2018 and the last two years of network activity have been dominated by memecoin trading on Solana, a clearly unsustainable trend.

The coming wave of real world asset tokenisation will determine whether we get an Ethereum revival or not. From my perspective Ethereum continues to excel in network measures that truly matter. Put yourself in the shoes of the “head of blockchain at {insert bank}”, she wants to get involved in crypto, the bank she works at probably manages more assets than the entire market capitalisation of crypto.

Going onchain for her is scary, but she understands she is just plugging into a new network. She will want liquidity, she will want a well established decentralised validator set (Ethereum now has over 1m validators across 13900 nodes) and most importantly she will want to use tried and tested token standards as wrappers for her financial products. Ethereum in this context is in a league of its own, but only time will tell and we will see this reflect in network activity.

While it’s easier to look away, seeking to understand is the only path to a more enlightened and empowered world. Bitcoin, Ethereum and distributed ledger technology are complex systems. Etherbridge lowers the barriers to understanding this fast-growing digital economy.

Keep up to date with the world of digital assets by subscribing to the Etherbridge newsletter.

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments. Collective Investment Schemes (CIS) are generally medium to long term investments. The value of participatory interests may go down as well as up. Past performance, forecasts or commentary is not necessarily a guide to future performance. As neither Lima Capital LLC nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice.