What to Watch in 2023

Where We Are

Investors will remember 2022 as the first real credit crisis that bitcoin and the broader crypto space have suffered. In historical terms, it was a significant year. The ensuing deleveraging eliminated many entities that got overzealous in the bull market and didn't adjust their strategies to new market conditions. Almost the entirety of those now-insolvent entities were centralised conduits to the world of blockchain and digital assets. This reset, whilst painful, is a necessary evil in the trajectory of a new and novel general-purpose technology. We expect similar problems to manifest in future market cycles because these problems are deeply human and have very little to do with the underlying technology itself.

We are pleased to note that the Etherbridge Fund didn't have direct exposure to any of these incidents as we avoided positions in tokens such as LUNA and FTT. Another safety measure is ensuring funds are kept in cold custody, and client assets are never lent out to companies such as Celsius or BlockFi.

In the most recent cycle, we also had another industry first; it was the first time credit from institutional finance became intertwined with the innovation cycle. Crypto market cycles are primarily driven by the innovation cycle and the speculation that ensues when a new 0-to-1 development is brought to life. Blockchain's general-purpose nature means that over a multi-decade timeline, we will see numerous incremental advancements that will propel the market to dizzying new heights and create the conditions for brutal corrections; this is even more evident when liquidity is freely able and cheap. As investors, the main priority in a market such as this is to maintain a level head and focus intensely on the technology itself.

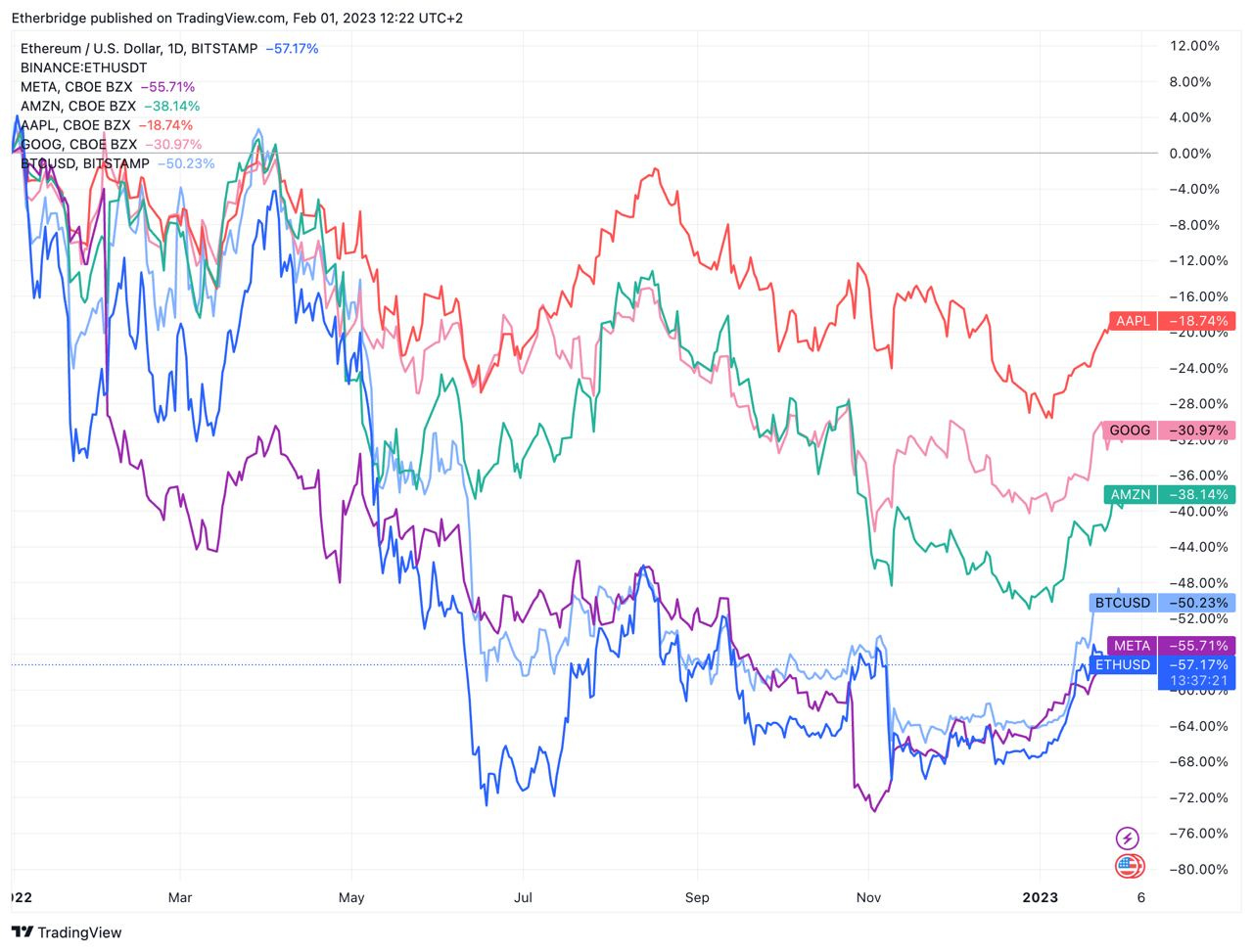

Financial assets felt real pain in 2022; there was almost nowhere to hide as global equities (-19.36% MSCI World Index) and bonds (-14.34% Vanguard World Bond ETF) had one of their worst year-on-year performances with U.S. bonds, specifically having their worst recorded year ever. The technology sector (-33.22% Nasdaq-100) saw some of the most significant drawdowns in public equities. We witnessed the unravelling of the Covid darlings trade with companies such as Netflix (-51.32%), Peloton (-78.86%) and Zoom (-62.9%) experiencing heavy losses. The damage was even worse for longer-duration, new frontier technologies such as those captured by the ARK Innovation ETF (-67.30%).

Even large multi-billion dollar technology stocks such as Apple (-27.11%), Amazon (-49.78%), Meta (-64.24%) and Google (-38.73%) weren't able to close the year with a positive return. With this in mind, the performance in digital assets on a relative basis wasn't surprising, with blue chip digital assets such as Bitcoin and Ethereum down -64.45% and -67.64% for the year, respectively.

Something worth pointing out is the relative performance of bitcoin and Ethereum verse these well-known stocks since the beginning of the Covid-19 pandemic.

Beyond the doom and gloom of the headlines, we saw massive leaps in blockchain networks' capabilities and capacity. Challenging technical upgrades such as the Ethereum Merge went through successfully. The merge, which saw a switch from a Proof of Work to a Proof of stake consensus, is analogous to changing an Airbus A380's engines mid-flight. It was an exceptional technical achievement, flexing the academic pedigree and human capital working on these technologies. Advancements in scaling, cryptography and interoperability will pave the way for the coming cycle of innovative projects and ideas.

We remain focused on selecting quality blockchain and smart contract applications that will help shape the future of finance and various online services. Recent advancements have eliminated many of the technical constraints of the previous cycles at a time when the broad market is significantly drawdown and distressed. This part of the cycle offers some of the best risk-to-reward opportunities.

Where We Are Going

The vision of public blockchains and the applications built on them is to create payment solutions and financial services that reduce the reliance one places on trusted third parties for the provision of these services. Yet, the industry still has a long way to go, and this can be seen by a centralised crypto service provider such as Coinbase having 103 million customers compared with the 7 million users of the entire DeFi industry.

It takes a while for the "common sense" of users to gravitate to the new norm. Common sense of the internet era is trusting intermediaries to manage the state of assets and online activities, using emails and passwords to log into services, and being comfortable with the lack of transparency these entities offer. The CeFi credit crisis of 2022 may be the catalyst to force this paradigm shift toward using DeFi products and services.

The reality is that blockchain and smart contract applications haven't reached functional equivalence with the incumbents they seek to disrupt. We see this as a combination of the following factors:

A lack of direct fiat onramps to DeFi applications.

Complex and low-functionality wallets and key management solutions.

A need for interoperability between blockchain networks and a heightened risk and complexity of participating on multiple chains.

High costs of transacting on-chain.

A general hesitancy to engage with something new or a general lack of education.

Solving these issues will allow blockchain and smart contract applications to reach parity with centralised incumbents, eventually resulting in a 10x better product offering. You may find this ironic, but we are going to use this opportunity to quote a crypto villain, Warren Buffet:

"In the short-run, the stock market is a voting machine. Yet, in the long-run, it is a weighing machine."

Whilst the voting machine of the market dismissed digital assets in 2022, we firmly believe that the weight of relentless development will continue to compound. Every hurdle or challenge identified by onlookers is just another potential business idea for the rapidly expanding human capital that continues to find a home in this industry.

Top Themes That Will Drive Markets in 2023

Upgrades to the User Experience (Account Abstraction and Danksharding)

Much of the development in the space feels somewhat intangible. Users hear about the next Ethereum hard fork, get all excited and then go back to using the technology. Nothing from their perspective has really changed or improved; both EIP 1559 and the merge are great examples of such upgrades.

Entering 2023, we have seen an increase in the conversation, financing and development around account abstraction, which will significantly change how users interact with blockchains.

On a network like Ethereum, there are two types of accounts, externally owned accounts (EOA) controlled by private keys and smart contract accounts controlled by code. If you have ever used a wallet on Ethereum, it's more than likely been an EOA.

Account abstraction will blur the lines between these two types of accounts and essentially create a merged version. Smart contracts, in this sense, will act as agents and have varying levels of permission and programmability not possible with basic EOAs.

Okay, so what does this mean? Account abstraction will revolutionise the experience of interacting with blockchains and smart contracts. It will provide a much-needed expressiveness to wallets that has been missing and help eliminate single points of failure.

A user will now be able to easily white-label specific integrations to avoid unapproved contracts, incorporate multi-sig approvals for transactions above a certain level, segregate funds into different pots and assign these pots additional permissions and authorisation requirements.

Account abstraction will play a significant enabling role for the next generation of adopters. This innovation will give blockchain wallets a similar feel and expressiveness to fintech banking apps. It will enable concepts like social recovery and smooth the onerous task of managing and securely storing private keys.

The other significant technical upgrade that will improve the user experience is EIP-4844 or Danksharding. EIP-4844 is the first step in the roadmap toward a fully sharded Ethereum mainnet. Sharding refers to splitting the blockchain into smaller portions to improve its overall efficiency. Think about it this way, Ethereum is currently a single-lane highway; every transaction that gets processed, executed and settled on Ethereum uses the same highway, and every validator needs to agree on every transaction.

Sharding will expand the number of highways and modularise validators across each new lane. Whilst sharding is the end state and some years out, danksharding is the first step in achieving this bigger mission. For a deeper explanation of danksharding and its difference from a fully sharded Ethereum, you can read Alchemy's description.

Whilst danksharding is only one step in the broad direction of greater efficiency, it will have tangible cost benefits for users of L2 solutions on Ethereum. The cheaper and more efficient these L2s get, the better their services become and the closer we converge on functional equivalence for financial applications.

Both danksharding and account abstraction will mark the first upgrades in years that genuinely change the user experience. Programmable wallets will give wallets a sophisticated account feel, and danksharding will collapse the cost of reaching settlement for transactions of value. Over the years, fads have drawn new users to blockchains, but combining these upgrades will ensure that we can better retain these users as trends come and go.

Scaling Blockchain Networks

We have been waiting for significant improvements in scaling smart contract platforms for a long time. Whilst Ethereum has obtained a certain level of success, it simply doesn't have enough capacity to meet demand. We even have a whole range of "Ethereum Killers" built in previous cycles to address this problem.

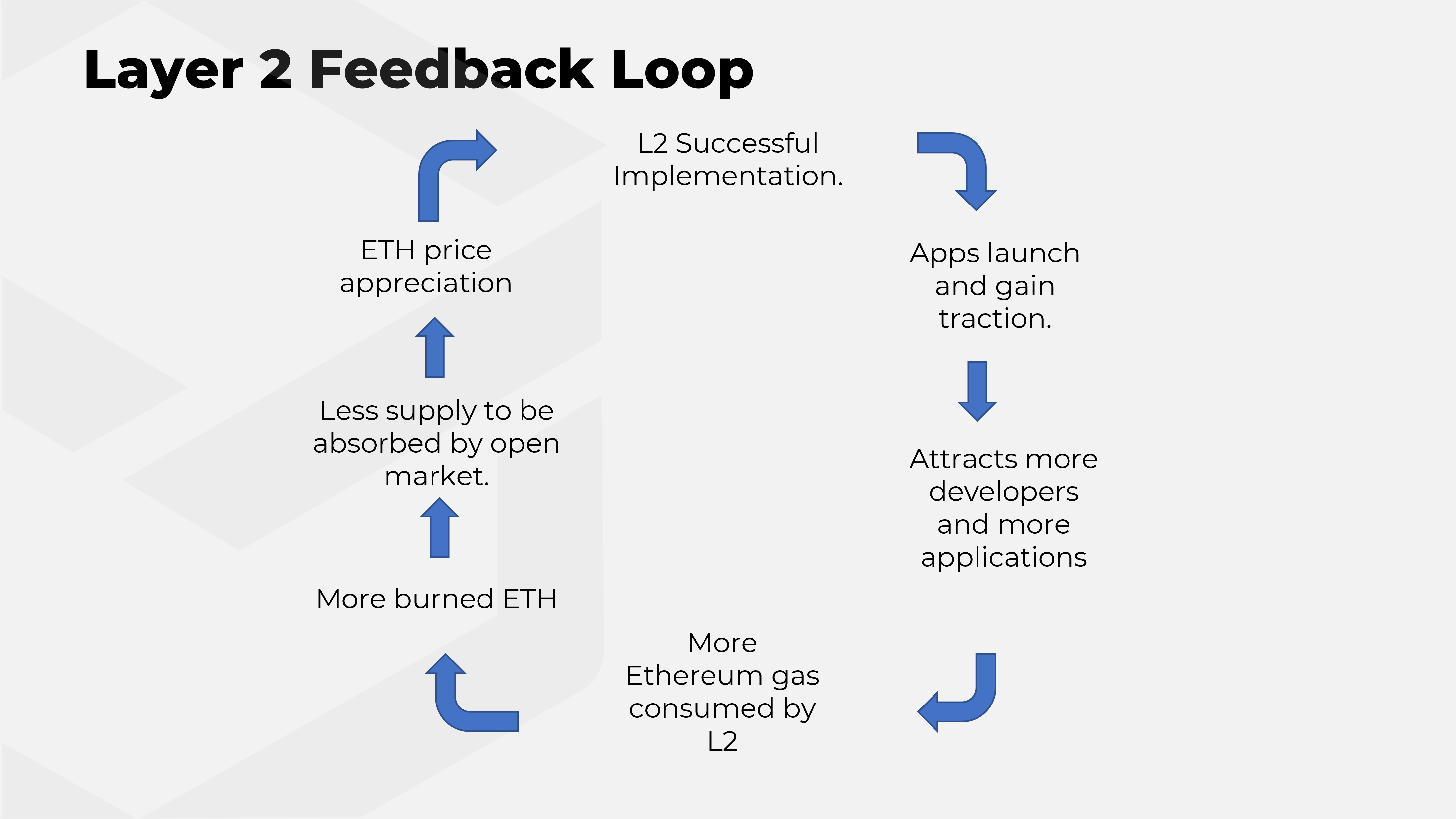

This cycle will be challenging for Ethereum Killers as Optimism and Arbitrum gain significant traction, and we wait for zero-knowledge proof solutions to launch truly functional products. For application developers, this means they can have all the security afforded by Ethereum with much of the throughput benefits obtainable on Solana and other alternative smart contract platforms.

We can see in the below image that L2 solutions on Ethereum have gone from using only 1% of gas fees to now accounting for over 4%. We expect this trend to continue and for L2 settlements to become the core consumer of Ethereum gas.

If we look at the composition of daily active users of L2s vs Ethereum and other EVM chains/non-EVM chains, we can see that they are beginning to take on a sizable market share.

L2 as a trade theme is undoubtedly a consensus trade for the year, and we expect to see tokens that govern these environments perform well on a relative basis verse the collection of Ethereum Killers. Success for EVM L2s means more consumption of Ethereum gas and, therefore, further downward pressure on Ethereum supply. We will continue to position as we did in 2022 and overweight ETH relative to a basket of Ethereum Killers.

Application-Specific Chains and Roll Apps

Within the blockchain innovation cycle, you can almost always find an idea or innovation before its time. Application-specific blockchains (App Chains) are one such example. Projects like Cosmos, Polkadot and Avalanche have been building toward this goal for some years now, but the difference today is that we can now practically envision deployable implementations of these ideas.

Until now, the industry has operated in a mindset grounded by generalist blockchains which provide general-purpose tooling for various potential applications. This form of architecture allows applications built on these chains to benefit from interoperability and composability with other applications.

An App Chain is just a blockchain with its own set of validators and node infrastructure, built around a specific use case. For example, we could see a Uniswap chain or an Aave chain. This degree of specialisation means that these applications can granulise their blockchain to best serve their particular use case.

The App Chain design also provides more flexibility for application developers as it changes their relationship with their end users. Dan Elitzer, in his piece "The Inevitability of UNI chain", explores the incentives for applications to build their own App Chains in detail, but we will summarise here:

Every application running on a general-purpose blockchain requires their end client to pay three different types of fees:

The Application Fee - The fee is charged for the service provided by the smart contract itself; in the case of Uniswap, the swap fee of 0,30%.

The Transaction Fee - This is the fee paid to the underlying blockchains validators to ensure the transaction is processed, executed and settled.

MEV - A fee which can be extracted by validators or market makers. These fees can be value extractive and increase the overall cost of a transaction without providing any benefit to the end user.

Today applications can only control the first fee, the application fee. Yet their end users need to absorb all three fees. Dan estimates the total cost for a simple swap on Uniswap is around 0,66%, so the governance of Uniswap doesn't even control 50% of the total cost for end users. This also makes it difficult for them to maximise token holder wealth while inspiring liquidity providers with a big enough fee share.

The incentives for applications to experiment with App Chains are evident, and we expect to see some blue-chip DeFi applications give it a go in 2023. dYdX, which was operating on its own Ethereum L2, is pioneering this move by building its exchange on its own Cosmos Appchain.

Cosmos is central to the App Chain movement and has a powerful narrative behind it as a leader for this new application architecture. Cosmos has been building toward this vision for many years and has already released key components such as Inter-Blockchain Communication (IBC) which will connect all Cosmos Appchains and eventually enable composability between these different chains.

Avalanche is another contender in the App Chain thesis. Recently Avalanche released their own version of IBC called Avalanche Warp Messaging (AWM), which, combined with their Subnets, has the potential to create an interconnected web of App Chains (Subnets). Ethereum layer 2's could also emerge as a hot pot for this new architecture. We have already seen successful implementations of roll apps with the likes of dYdx on Starkware.

Technically, there is a distinct difference between roll apps on Ethereum and App Chains or Subnets on Cosmos and Avalanche. Roll apps on Ethereum, whilst possible, are siloed and lack interoperability and composability with other roll apps, an issue we are sure will be resolved over time. Additionally, Ethereum L2s are still highly centralised when compared to Cosmos Appchains and Avalanche Subnets. However, the point is that both Cosmos and Avalanche are currently in a position to truly enable this new architecture without having to wait months or years for further upgrades.

This will also affect some of the underlying beliefs of investors in the space who have long bought into the "fat protocols thesis" outlined by Chris Burniske. It will significantly change the incentives for application developers and hopefully result in new unique products that can genuinely compete with centralised incumbents.

Decentralised Nasdaq:

As we have alluded to in the Where We Are Going Section, DeFi applications still leave much to be imagined. Don't get us wrong, DeFi carries many breakthroughs for the world of finance. Permissionless swaps on Uniswap have served as the heart of on-chain asset exchange. Lending platforms like Aave and Compound facilitated orderly liquidations in a year when many Wall Street-led centralised equivalents declared bankruptcy. MakerDAO continues to maintain DAI's peg to the US dollar successfully.

The building blocks are taking shape, but the industry lacks a reliable decentralised closed limit order book (CLOB) exchange. Most of our traditional exchanges manage order books and require market makers to participate and contribute liquidity for orderly exchange operations.

Uniswaps simplicity is both its greatest strength and weakness. The order book exchange is the holy grail for DeFi. The Automated Market Maker (AMM) model used by Uniswap produces a unique service that is great for exotic pairs and has aided in providing a venue for early-stage projects to launch and provide liquidity to token holders.

Uniswap v3 has further spurred Uniswaps' success and sheer dominance in the decentralised exchange landscape, but it still lacks the trading experience and pinpoint price execution of its CLOB exchange equivalents. Market making at size has also been difficult on the AMM model due to risks associated with impermanent loss, but this is improving too with projects like GammaSwap.

There is a massive opportunity for a decentralised version of the Nasdaq to emerge, and the infrastructure for such a thing to happen is almost there. We have already seen attempts, some more successful (dYdX) than others (SERUM), but certainly nothing that has been able to capture significant market share from centralised exchange operators.

When combined, there is a confluence of factors that may just result in a genuinely competitive decentralised exchange. Advancements in scaling, reduction in the cost of settlement, speeding up potential matching engines for exchanges, account abstraction providing a more useful and dynamic user experience and maturing infrastructure for App Chains could collectively enable a decentralised Nasdaq.

The Search for a Business Model

At the risk of sounding like we are complaining, this one is on the regulators. Since the ICO boom of 2017, smart contract applications have been searching for a business model that maximises token holder value.

We have seen a lot of mental gymnastics around token value accrual, which has led to inefficient and dilutive strategies such as liquidity mining. Many of these projects avoid experimenting with equity-like value accrual formulae because there still remain no securities laws that pertain to global smart contract services.

Regulators need to provide clarity on this front so that we can cut through the noise and enter a realm where token holder value is maximised. We are still a long way from seeing real and comprehensive regulation on this matter, but it is essential for the future of this space.

Unfortunately, regulators will need to apply themselves when creating this new set of regulations, as concepts like the Howey Test are archaic and unsuitable. The Howey Test is a framework for classifying an asset as a security and was created in 1946, more than 50 years before the rise of the internet. To think that this framework is applicable in our modern internet and a blockchain-enabled world is ludicrous. This will take time, and we can only hope to avoid policy errors on the path to fair and clear regulation for token issuers.

Clarity from regulators will create the conditions necessary for institutions and capital allocators to take a more serious look at these technologies whilst bolstering entrepreneurs' ability to best protect and create value for them.

Whilst the consensus in crypto markets is that regulation will be a net negative for the space, we would argue this perception is missing the bigger picture. In fact, we believe that fair and clear regulation could serve as a catalyst for a fundamentals-driven bull market for tokens.

Token projects have distinct advantages over their analogue competitors, especially in the world of financial services. Smart contract platforms serve as global public financial clouds offering entrepreneurs a Turing complete and composable technology stack to build out financial products. Redundancies of this network are shared, and the cost is socialised by the nodes that make up the ecosystem. Entrepreneurs can launch multi-billion dollar smart contracts for $100 - $50000, depending on the blockchain they decide to use and the complexity of the business logic in their smart contract.

With this in mind, we can expect the barriers to profitability of these projects to be relatively low. We are already seeing many projects generating millions of dollars in revenue and further a class of impressively profitable tokens. Our bias in the current climate (lack of regulation and lack of distinct business model) is to favour low-dilution tokens that produce a real yield.

Bringing It All Together

Our read on the digital asset market for 2023 is that we are entering the early stages of the next innovation cycle. Opportunity is flush in this part of the cycle as the paths of winners and losers begin to diverge, and a new breed of investable assets comes to the market. Investors need to constantly reassess whether ideas that were successful in 2021 will continue to gain traction or fade into oblivion.

Our focus will remain on projects and teams that continue to push development and show the ability to deliver on their technical roadmaps. Emphasising fundamental data points will provide a clear line of sight to the winners of this cycle.

Our portfolio is overweight infrastructure and DeFi, underweight Bitcoin and neutral on Web3 applications compared to a market capitalisation-weighted index of the entire digital asset market. DeFi is heavily underrated, and we expect this to be rerated in the latter parts of the cycle. We have concentrated positions in infrastructure investments in smart contract platforms and layer 2 solutions that provide both technical and economic sustainability.

Crypto is dead—long live crypto.

Notable Articles and News Stories This Week:

European Union Bank Again Uses Ethereum to Explore Tokenised Bonds

The European Investment Bank (EIB) is once again leveraging Ethereum in its quest to tokenise capital markets, this time while issuing the first-ever digital pound sterling (GBP) bond on a separate private blockchain.

EIB, the primary lender of the European Union, deployed the £50 million ($86.6 million) bond to a permissioned network underpinned by HSBC's tokenisation platform, Orion. The EIB is a public institution owned by the EU's 27 member states.

The bank opted for a private network for privacy and efficiency, according to a statement. In an effort to increase transparency, the bond was also recorded on Ethereum, a spokesperson told Blockworks.

This was done to provide evidence the issuance took place while still maintaining the anonymity of bondholders.

HSBC debuted Orion last November, when it first flagged intent to launch the tokenised GBP bond. BNP Paribas, HSBC, and RBC Capital Markets were named as joint lead managers of the bond, with those firms serving as custodians. Client assets will be stored in digital securities accounts kept on Orion, the bank said.

Read more about the bonds here

Australia To Tackle Crypto Regulation in Three Stages

In Australia, crypto startups are preparing for the government's multi-stage approach to regulating crypto, pitched to protect consumers from what it considers unsustainable business models.

The previous government failed to take the time to future-proof regulatory frameworks, leading to consumer exposure to recent risks, Treasurer Jim Chalmer's office said in a joint statement Friday.

"While the industry continues to develop and expand, crypto assets are still commonly associated with speculative trading, posing significant risks," an accompanying consultation paper reads.

Beginning with the first of its three-stage approach, the Australian Securities & Investments Commission, the country's main financial regulator, will begin bolstering the size of its crypto team.

Read more about the three-stage approach here

Fed Opts for Lower Rate Increase

In a widely anticipated move, the Federal Reserve moved to bump interest rates by a quarter of a percentage point Wednesday, marking the start of what markets hope will be a prolonged period of smaller hikes.

The US central bank cited Russia’s ongoing war in Ukraine, continued heightened inflation and a need to reach maximum employment as reasons for the slower-paced hike.

The move marks the Fed’s eighth consecutive rate increase, a strategy it hopes will curb the highest inflation the country has seen in more than four decades, but analysts remain worried a soft landing may be a tall order.

“The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time,” Federal Open Market Committee (FOMC) members wrote in a statement at the end of their two-day policy meeting Wednesday.

Read more about the decision here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.