The Long Grind

How great assets escape their consolidations, and what it tells us about crypto.

Investors are exhausted. Five years grinding below the November 2021 highs has shifted the dominant narrative. Crypto is broken. The original thesis was wrong. This time is different.

This time is not different. This is what generational compounders look like in the middle of their consolidation.

The easy question is whether this has happened before. The harder question is what ends it.

The easy question first. Yes, it has happened before, and it has happened to household names. The stocks everyone wishes they owned. The stocks every YouTube short with a stock-tip account uses as an example.

There is a pattern behind those home runs that does not show up in the short form content.

The pattern

Innovation trigger. Something new appears. An idea big enough to reorganise an industry.

Blowoff top. Price runs ahead of any coherent thesis.

Initial unwind. The original story is discredited. The reinforcing loop of price into perception into fundamentals into more price flips into reverse.

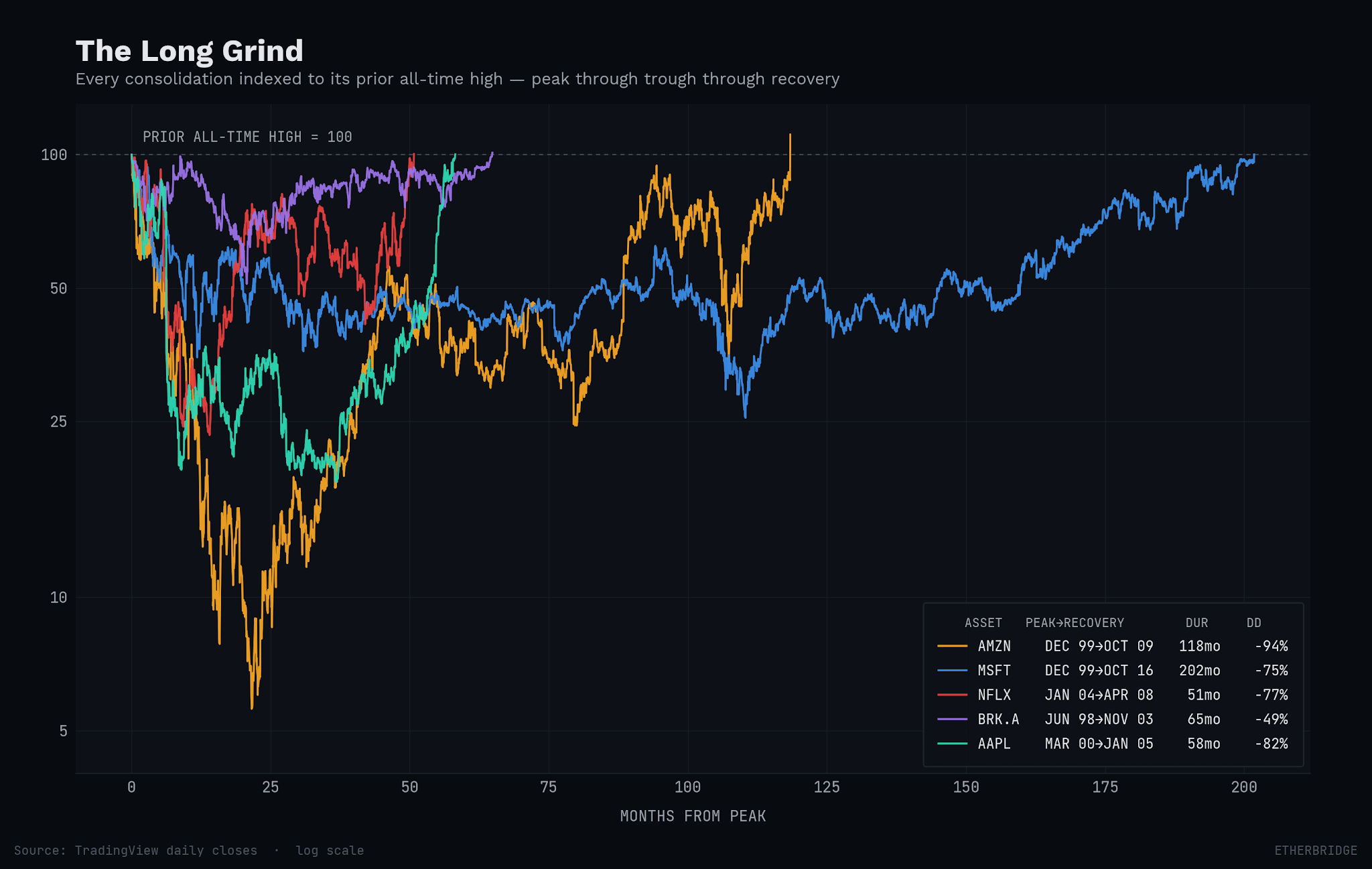

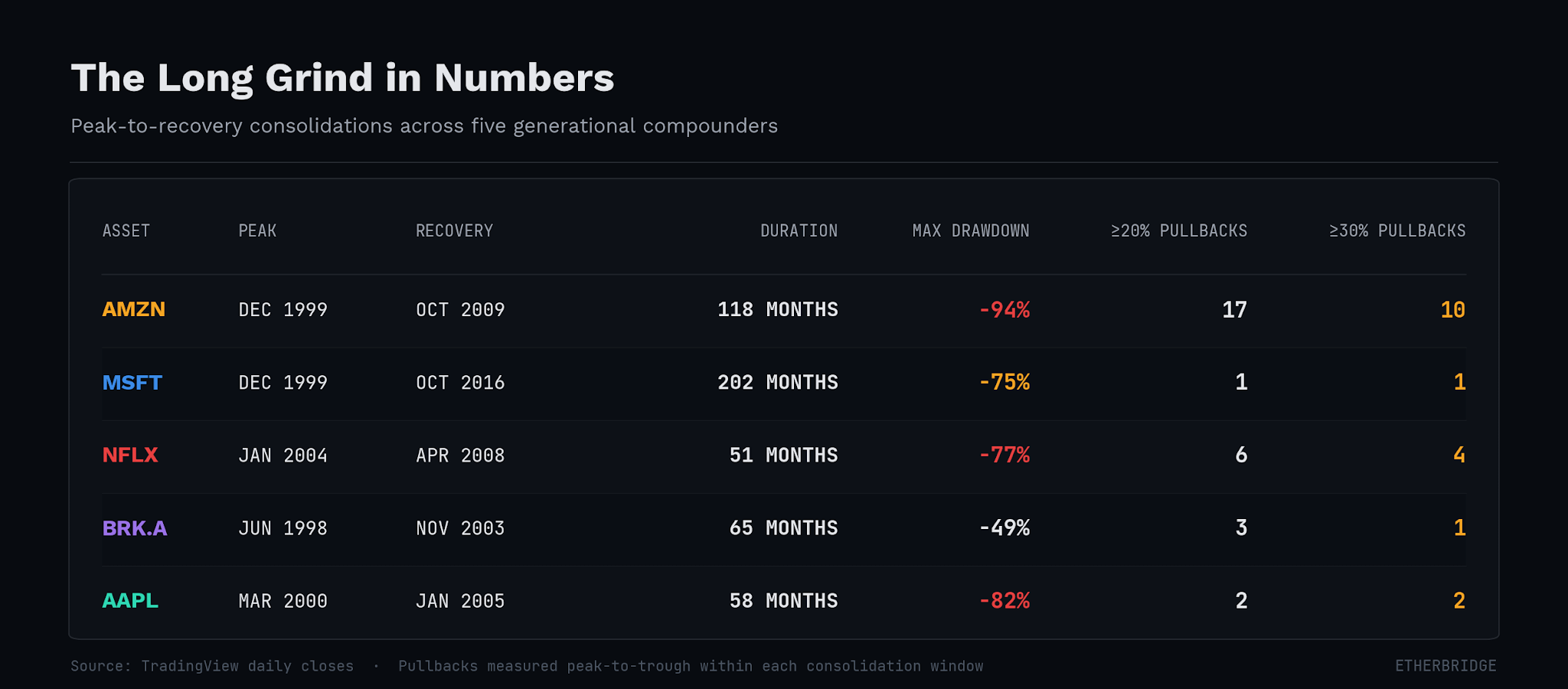

The long grind. The asset is rebuilt, diversified, stress tested. The market argues about what it even is.

Mid-consolidation drawdowns of 50 to 60 percent. Shares transfer from the impatient to the patient. Interpretation transfers with them.

Resolution. Comes only when secular forces force the market to update its definition of the asset.

There are many names for this pattern. The most popular is the Gartner Hype Cycle.

You have seen the YouTube shorts. “If you bought 100 shares of Amazon in 1997…” The shorts never tell you what it felt like in 2001, or what the same chart looked like in 2008. The unsexy part is what this piece is about.

The consolidation is a conviction test. The drawdowns within the multi-month range are brutal. Each drawdown is an opportunity to blow up your account, and a transfer of fast money focused on the voting machine to convicted capital focused on the weighing machine.

Amazon went through 17 separate drawdowns of 20 percent or more on its way to becoming what it is today. Apple went through two drawdowns over 50 percent. Microsoft spent 17 years recovering. Nobody talks about these drawdowns because they do not help sell online courses or newsletter subscriptions.

The sound of capitulation

It is worth pausing on what was being written about each of these names at the lows. These were not fringe takes. They were the cover stories.

“Microsoft’s Lost Decade” - Vanity Fair on Microsoft, August 2012

“This is just the beginning.” - Steve Fortuna, Merrill Lynch, downgrading Apple after its 52 percent single-day crash, September 2000

“Short Netflix. Buy Blockbuster.” -Michael Pachter, Wedbush Morgan, sell rating with a $3 price target, 2005

“What’s Wrong, Warren?”- Barron’s on Berkshire Hathaway, December 1999

The same publications are writing the same things about crypto right now. The certainty is identical. The instinct is identical. The asset class is different. The urge to bury something while its identity is changing underneath remains strong in financial market commentary.

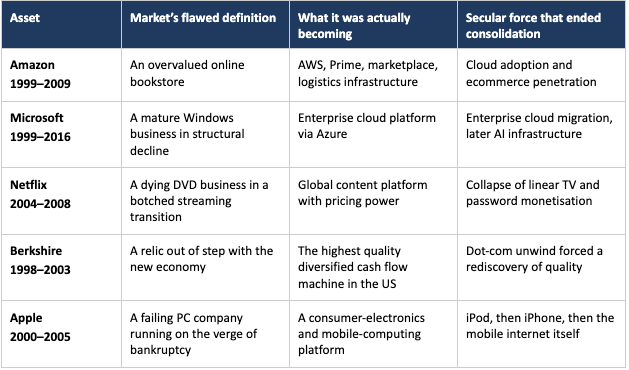

The market was holding an outdated definition

Each of these consolidations had the same shape. The market priced the asset as one thing. The asset was quietly becoming another. The consolidation ended when reality forced the market to update its priors.

Consolidations are workshops. They do not end because the chart wants to go up. They end because the world has changed enough around the asset that the old valuation no longer makes sense.

Why the market gets the definition wrong

Three reasons.

The original narrative anchors the market even after the business has moved on. New use cases compound quietly because they do not show up in headline metrics or form part of the old identity. Analysts are paid to model the existing business, not to imagine the next one.

Each mid-consolidation drawdown reinforces the old narrative being dead even while the new one is being built. The transfer of shares from impatient to patient is also a transfer of interpretation. The new holders carry the new thesis.

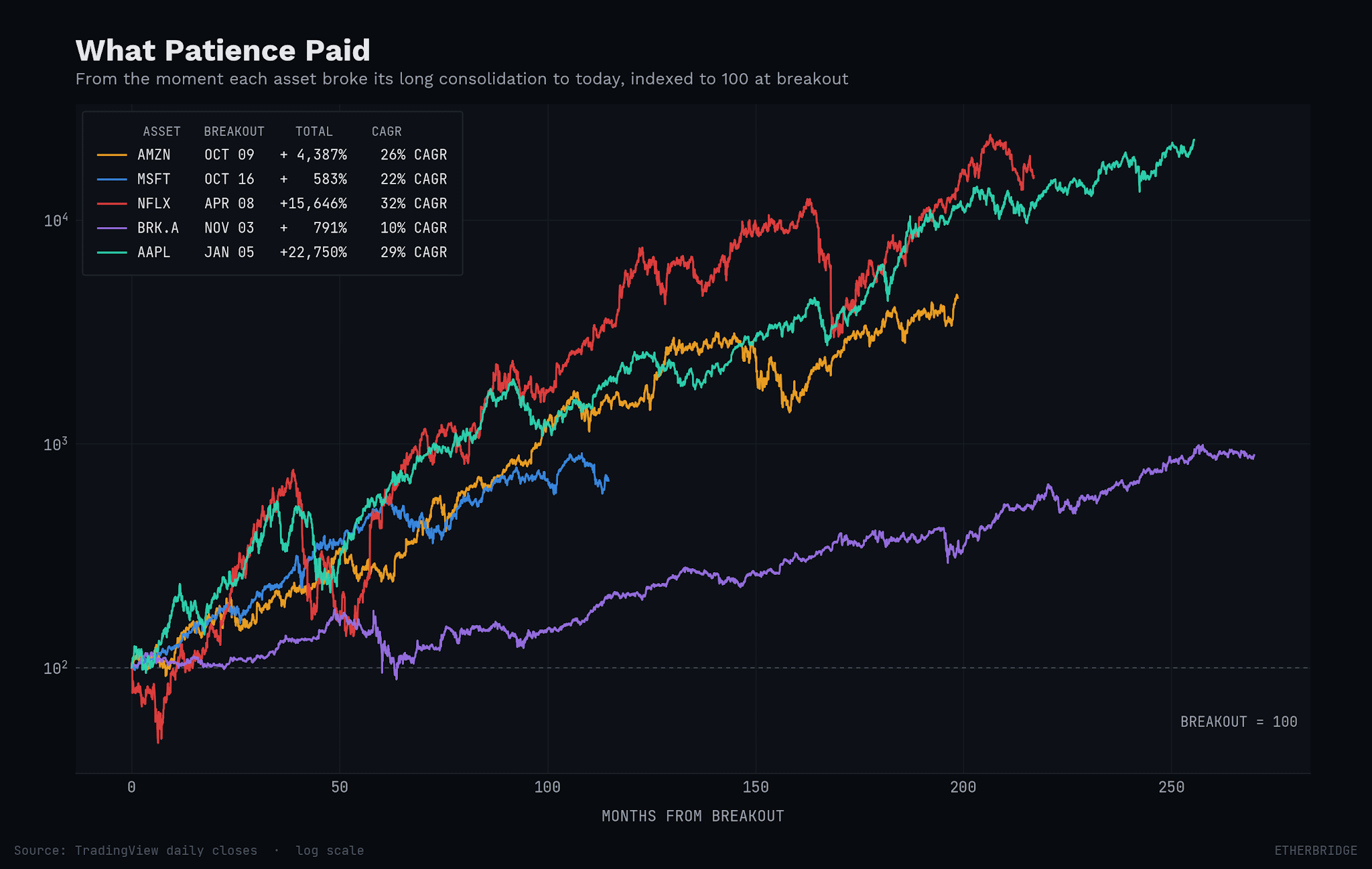

From the moment each asset broke its consolidation, the returns to patient capital were extraordinary. None of these compounders looked like compounders in 2001, or 2003, or 2012. They looked like the losers nobody would want to hold.

The Crypto Consolidation

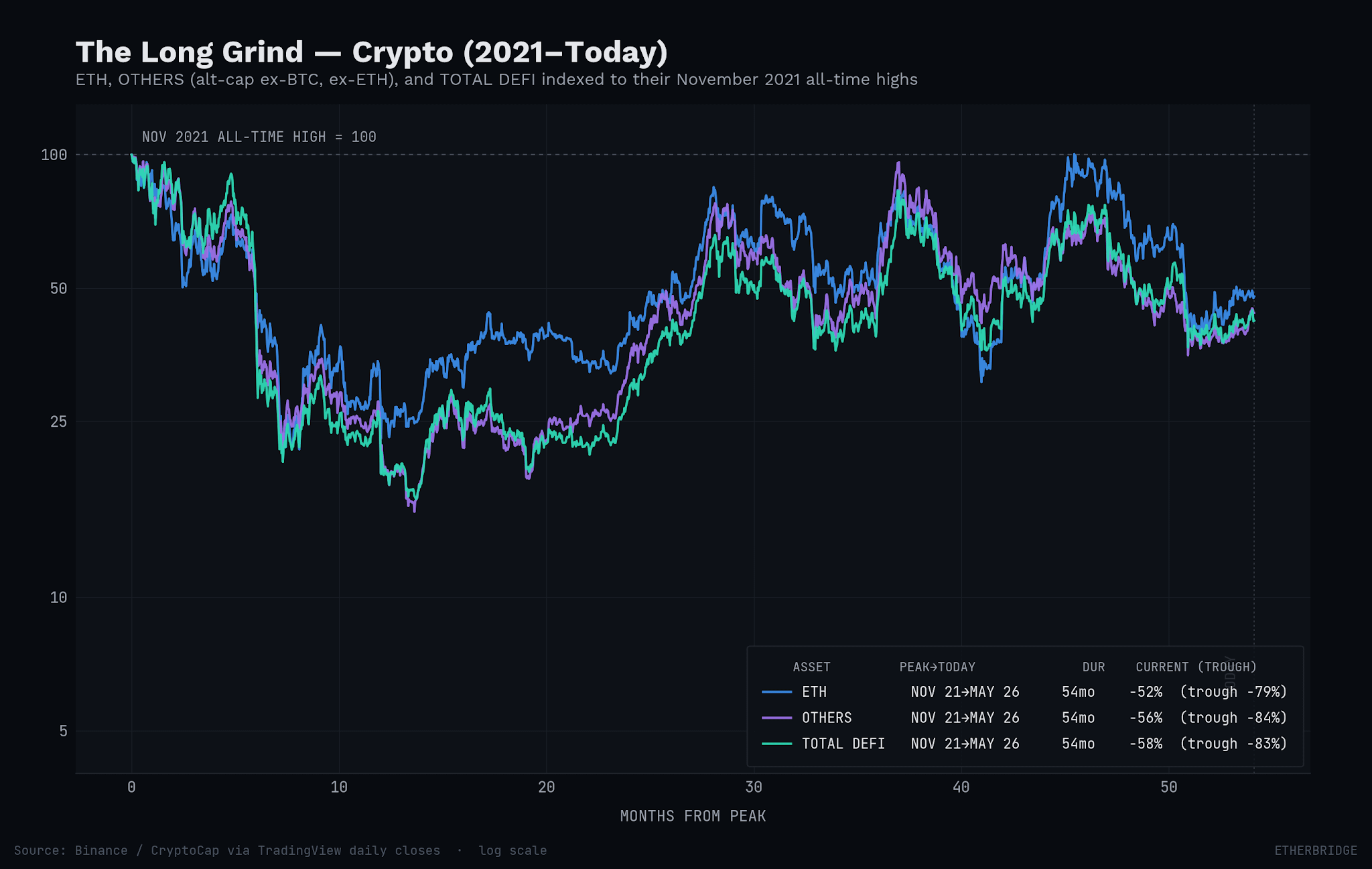

ETH, the broader altcoin market (OTHERS, ex-BTC and ex-ETH), and total DeFi all peaked on the exact same day. November 8, 2021, the day the “dot-crypto” bubble burst. All three troughed roughly 80 percent below those highs. All three have spent 54 months below the prior peak. Compared to the equity consolidations above, this is where Amazon, Apple, and Netflix were at the same elapsed time.

What the market thought crypto was

From inception to the peak of “dot-crypto”, crypto was an ideas industry. The asset class did not trade on fundamentals because there were no fundamentals to trade on. What traded was the promise. That money would be reinvented. That capital markets would be rebuilt. That ownership itself would be reimagined.

None of those promises were wrong. They were just unpaid and without receipts. Every token, from the most speculative memecoin to the most credible protocol, was priced as if the entire vision would arrive at once.

The consolidation has done its job. The promises that had no path have been priced out. The JPEG mania. The dog-coin casino. The yield farms paying 4000% in their own inflation. What remains is the part of the thesis that has started to deliver evidence.

What is actually being built

If we strip the asset class back to first principles we converge on a simple idea. Public blockchains are the best way to move money. They settle value instantly. They are global. They do not close on weekends.

Once you accept that, the framing of everything else changes. If public blockchains are the best way to move money, they are also the best way to move anything that behaves like money. Treasury bills. Money market funds. Gold. Equities. Anything with a balance that needs to move.

In 2021, crypto was a noun. A thing you bought. In 2026, crypto is a verb. It is something money does. Something a treasury bill does when it settles in twelve seconds instead of two days. Something a share of Apple does when it trades onchain at three in the morning on a Sunday.

Stablecoins are crypto. Tokenized treasuries are crypto. Onchain equities are crypto. The agentic economy will be crypto, because AI agents need rails that are programmable, instant, and global. The existing financial rails are none of those things.

The category has stopped being a religion you belong to. It has started being the infrastructure you use.

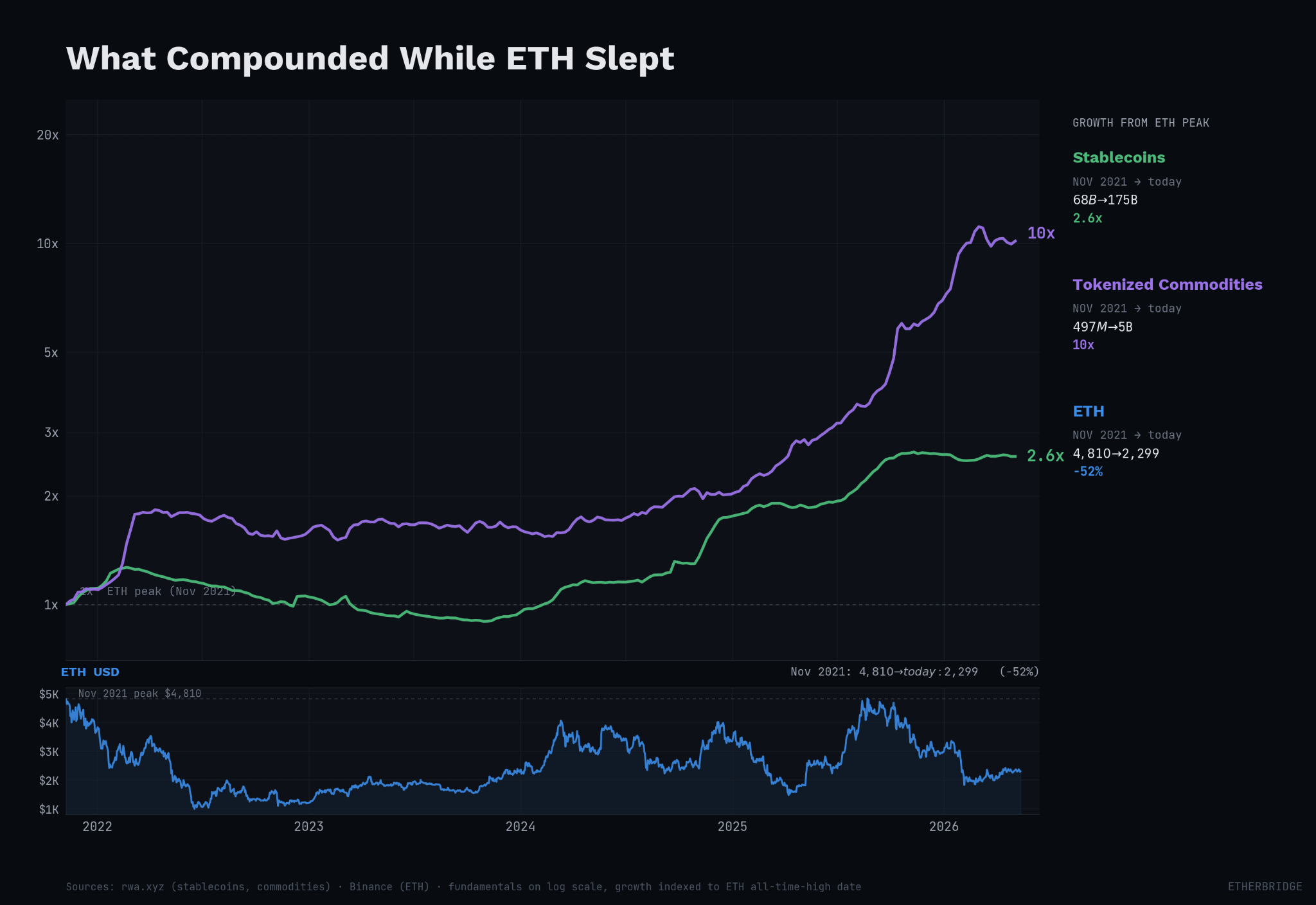

Stablecoins at $175 billion, up from $68 billion when ETH peaked. Tokenized commodities at $5 billion, up from $497 million. These are the two categories that existed at scale before the consolidation, and both have compounded straight up while the price asset has gone sideways.

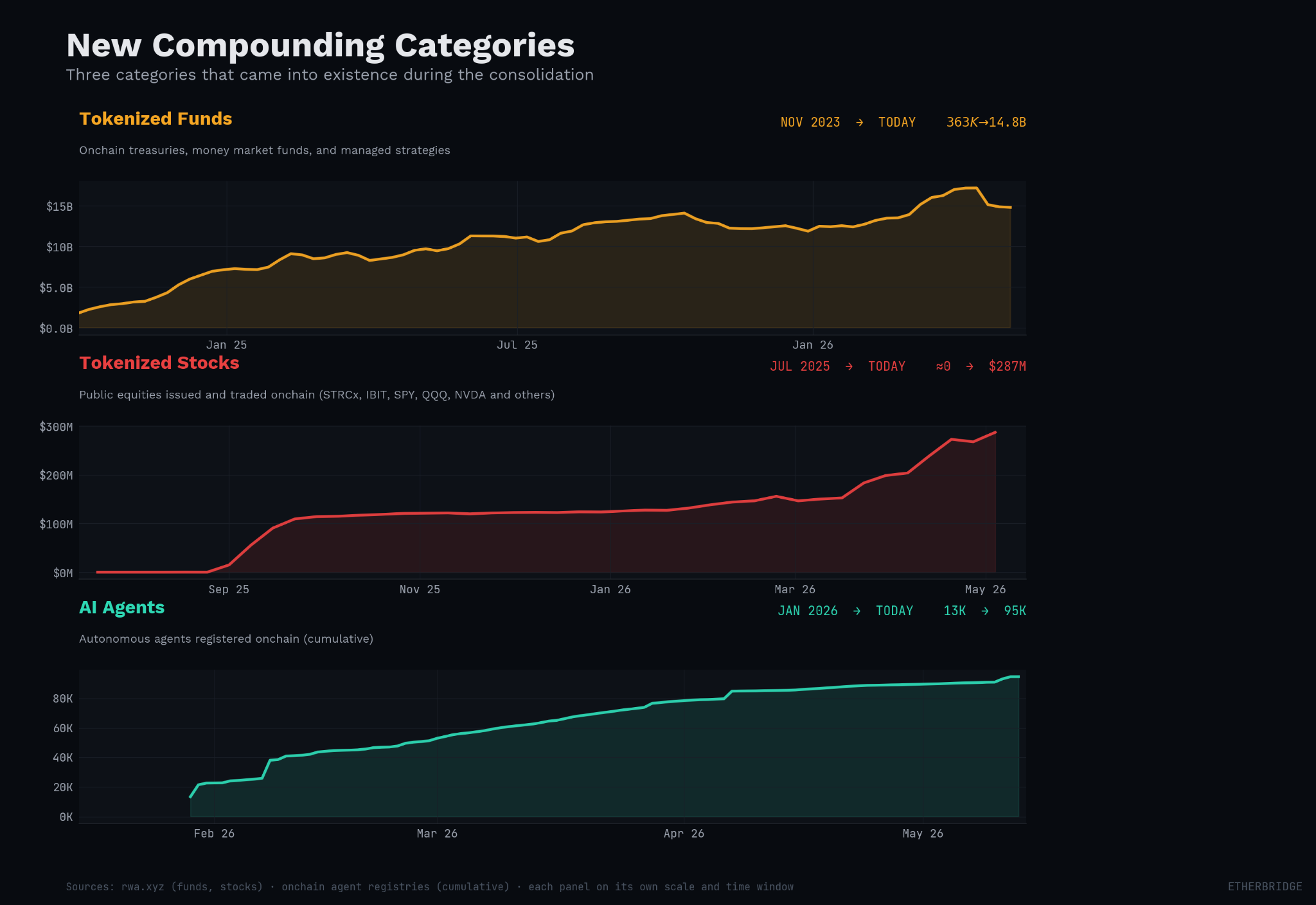

Three categories did not exist at scale at all. Tokenized funds at $14.8 billion. Tokenized stocks at $287 million. And almost 95,000 AI agents registered in the Ethereum Ecosystem. Each one has come into existence during the consolidation.

This is the receipts arriving. The market is still arguing about whether crypto is real. Meanwhile the rails are being laid and public blockchains as the first principles best way to move value are increasingly being adopted.

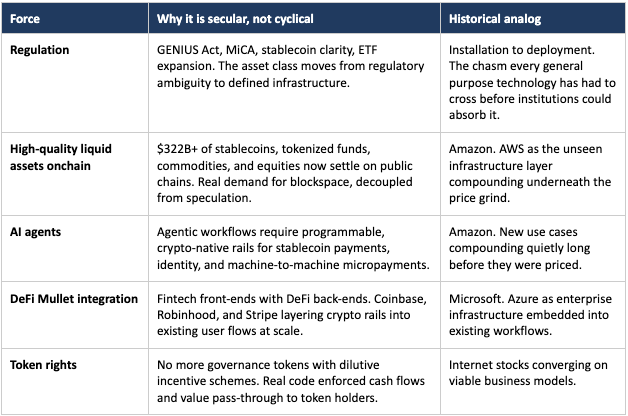

The five forces that resolve this consolidation

These are the secular pulls that, when the market is forced to price them, end the argument over what crypto is and become its defining identity.

These are the drivers that will change the identity of crypto. From speculative magic internet money anchored to the monetary debasement trade, to a productivity technology rewiring money and global capital markets.

Throughout the consolidation tokens transfer from impatient holders of the old thesis to patient holders embracing the new thesis.

Crypto as a regulated network of protocols, servicing trillions of dollars in high quality liquid assets and integrated firmly into the back end of institutional finance.

This is what generates the revenue. The network facilitates the money verbs. Pay. Lend. Borrow. Exchange. Transfer. Hedge. Settle. Agent-to-agent payments at machine speed.

Every transaction consumes blockspace. Blockspace is the product blockchains sell. Business logic is the product protocols sell.

The blockchains that turn the consolidation into compounders are the ones whose blockspace is most in demand.

The protocols that turn the consolidation into compounders are the ones whose business logic finds product-market fit, and whose token rights are code-enforced. Product-market fit means DeFi Mullet integration and real utilisation. Code-enforced rights mean value passes through to holders.

Two ideas need to be held in our heads at the same time.

The first is that many cryptoassets will never see their multi-year consolidation resolve to the upside. Most will not.

The second is that some will. The multi-year rally that follows will become the same dopamine-hitting short-form content future generations will see as true investment success, without ever mentioning the brutal consolidation period.

The key to distinguishing the winners from the losers is identifying cryptoassets that are beneficiaries or enablers of the emerging secular forces.

What that looks like in practice

I’m looking for dominance, not promise. The 2021 portfolio asked what a token could become. The 2026 portfolio asks what it is becoming, measurably, right now. Secular forces tend to concentrate dominance. Cloud computing did not produce ten AWSs. Streaming did not produce ten Netflixes. The consolidation resolves for the assets that win the category, not the assets that compete in it.

These are the questions I seek to answer everyday and use to construct my portfolio.

Which blockchains host the high-quality liquid assets actually being issued onchain. Stablecoins, tokenized funds, tokenized equities, tokenized commodities. Every asset issued onchain expands the network effect. Find the network effect, find the winner.

Which Chain Street applications show rising utilisation. Real users, real volumes, real fees.

Which Chain Street applications are winning the DeFi Mullet adoption, which protocols are institutional providers integrating into their backend.

Which blockchains are pioneering the standards for the agentic economy. Who is building the railroad equivalent for agentic economic actors.

Which blockchains are AI agents actually transacting on. Not the ones claiming to be agent-ready. The ones where agents are settling commerce today.

Which protocols have acknowledged token rights and put in place code-enforced value pass-through to token holders. Which protocols are making it worth an investor’s attention.

Building crypto exposure around these questions is how you survive the consolidation, forget what crypto was, ignore the day to day voting machine of market fluctuation and focus rather on where weight is increasing being built.

My next post will include a dashboard for tracking the five forces and answering the above questions. Two earlier memo’s map directly onto this framework and are worth reading alongside it.

How I think about valuing ETH. A framework for pricing the network on what it actually does. The capital it secures, the blockspace it sells, the settlement value flowing through it, rather than the narrative it carries.

The Token Rights screener. A working list of DeFi protocols with code-enforced token rights, their cash flows, and where they trade against fundamentals. This is the operational answer to the token rights force above. Which protocols are actually making themselves worth owning.

While it’s easier to look away, seeking to understand is the only path to a more enlightened and empowered world. Change is now exponential and blockchain technology sits at the centre transforming money, finance and what it means to sovereign. Join me in exploring this new world by subscribing.

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments. Collective Investment Schemes (CIS) are generally medium to long term investments. The value of participatory interests may go down as well as up. Past performance, forecasts or commentary is not necessarily a guide to future performance. As neither Lima Capital LLC nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice.