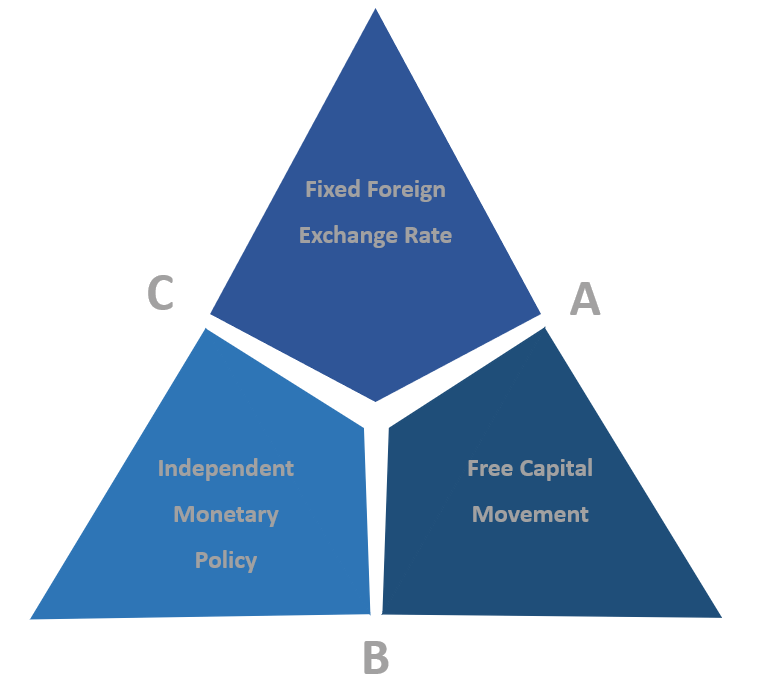

The Impossible Trinity

Market Recap

A Tough Week for Crypto

The Impossible Trinity

The impossible trinity, otherwise known as the impossible trilemma or the Unholy Trinity, is a concept in macroeconomics that states it is impossible for a country to have all three of the following at the same time:

a fixed foreign exchange rate

free capital movement

an independent monetary policy

This concept was developed in the 1960s by John Flemming and Robert Mundell; they based it on two things, a study of several central banks and governments throughout history who tried to implement all three simultaneously and the uncovered interest rate parity.

Trillemas have been used as thought experiments as far back as Ancient Greece to describe situations that have three equal solutions to a complex problem. Within blockchain design, there exists a trilemma between decentralisation, scalability and security which we have written about here and here. However, it is arguable that the impossible trinity is the most well known in modern times.

The following diagram can help visualise the impossible trinity:

When central banks have to make fundamental decisions about managing international monetary policy and goals, they can only choose one side of the triangle. This is because each side of the triangle is mutually exclusive to the others. As a policymaker, you can only satisfy two out of the three goals as the third will always contradict the first two. If you want to accommodate free capital movement and control your own supply of money, you cannot fix exchange rates. If you set exchange rates and control your supply of money, you cannot accommodate free capital movement. Finally, if you control capital movement and fix exchange rates, you cannot control the growth supply of your money.

Here is a practical example of the above:

Assume that the world interest rate is at 5%. Suppose the home central bank tries to set the domestic interest rate at a rate lower than 5%, for example, at 2%. In that case, there will be a depreciation pressure on the home currency because investors would want to sell their low yielding domestic currency and buy higher-yielding foreign currency. If the central bank also wants to have free capital flows, the only way the central bank could prevent the depreciation of the home currency is to sell its foreign currency reserves. Since foreign currency reserves of a central bank are limited, once the reserves are depleted, the domestic currency will depreciate.

The tradeoffs presented by this trilemma obviously profoundly affect the decisions you make as a policymaker. The challenge comes with deciding what side of the triangle to pursue. We have recent examples of all three, and this can help us better understand why central banks around the world are currently in the position they are in.

Side A: A stable exchange rate and free capital movement

The Eurozone and the Gold Standard are excellent examples of this side of the triangle. This has allowed the Eurozone as a whole to flourish; however, because specific countries within the Eurozone can't control their own monetary policy, they have run into problems like Greece did in its financial crisis. It was a deep-rooted problem that has taken years for Greece to overcome, and they have had to rely heavily on the ECB to help meet their debt obligations. This also, as a result, has placed additional stress on the Eurozone as a whole.

Side B: An independent monetary policy and free capital movement

This is the model most countries in the world currently work on. It has allowed them to maintain monetary sovereignty and try to encourage international trade. They have the freedom to increase or decrease interest rates. However, this has resulted in many countries artificially manipulating interest rates to remain more competitive globally and stimulate their economies. A big problem that they have run into is that once interest rates hit zero, central banks next biggest tool is quantitative easing, or the monetisation of debt. Since 2008 this has resulted in a significant increase in the balance sheets of central banks globally, which currently sits close to $30 trillion. This puts further pressure on the economy.

Side C: A stable exchange rate and independent monetary policy

There are a few examples of this in practice today. However, the biggest global example of this in practice was Bretton Woods. Under the Bretton Woods agreement, America would adopt a "Gold Standard", and others would, in turn, peg their own currency to the value of the dollar at a fixed rate. However, this didn't work as America started issuing more Dollars than they had gold reserves as they wanted to be able to influence their monetary policy. This resulted in a breakdown of the monetary relationship between America and many other world superpowers. In 1971 America went off the Gold Standard and instead focused on their own monetary policy and free capital movement.

All these options and examples above are characterised by a tradeoff. In reality though, most countries and their central banks have implemented a combination of all three in some way or another. While most have chosen independent monetary policy and free capital movement, they have also attempted to maintain a stable exchange rate. When remarking on pursuing all three policy goals of the trilemma, Milton Freedman, the famed economist, once said, "you get a pressure cooker with a disabled safety valve. It is simply not sustainable."

There is not necessarily one correct answer; it really depends on a country's own unique circumstances. However, pursuing all three is just not going to work.

But where does bitcoin fit into the equation? Bitcoin falls under side B. Bitcoin has implemented its own monetary policy and allows for free capital movement. It has forgone a stable exchange rate, and as a result, bitcoin's price is a function of demand relative to supply. This also helps explain bitcoins volatility. One thing also to note is that bitcoin, while adopting its own monetary policy, is currently unique in that it is a non-discretionary form of monetary policy. No other country in the world presently has that type of monetary policy in place.

While all currencies are subject to the same rules, there is a way that you can ensure there is at least a high chance of long-term viability for your currency. That is to only pick two sides of the triangle. Central banks across the globe have been trying to pursue a combination of all three in some capacity, resulting in the situation we are in today. While still to be proven successful, Bitcoin has at least decided only to pursue two sides of the triangle.

Lima Capital’s Offerings are Expanding

The regulated investment advisor of the Etherbridge Fund, Lima Capital LLC and financial services advisory and consulting company Bakari AG today announce the launch of their new Voyager High Yield DeFi Fund—the first of its kind. The product offers the benefits of blockchain-based investment opportunities through the security of a mutual fund, secured by institutional crypto custody provided by Trustology.

The low US$ interest rate environment has driven investors to search for alternative yield opportunities, and with the explosion in demand on Decentralised Finance (DeFi) protocols leading to higher interest rates, attractive risk-adjusted opportunities can be found in this technologically sophisticated market. The barrier to entry, however, has been high. There are many regulatory, operational and security issues to solve before delivering a DeFi-based investment solution. With these issues solved by the experienced teams at Lima Capital LLC and Bakari AG, Voyager is unique in its offering.

The Voyager High Yield DeFi fund follows a conservative strategy that minimises risk exposure while capitalising on blockchain-enabled income opportunities. This is achieved through the utilisation of proven DeFi protocols to earn interest on US$ pegged stablecoins; assets that do not inherit the volatility associated with cryptocurrencies i.e. bitcoin (BTC) or ether (ETH), but that still make use of the underlying networks.

Learn more and read the full announcement here

Notable Articles and News Stories This Week:

SEC Threatened to Sue Coinbase Over Lending Product, CEO Says

U.S.-based cryptocurrency exchange Coinbase says the Securities and Exchange Commission (SEC) has threatened to sue over its yet-to-be-launched “Lend” program.

Coinbase said it had been in discussions with the SEC over its program for almost six months. Despite these ongoing discussions, Coinbase says the SEC issued a “Wells Notice,” according to a blog post on Tuesday. Lend aims to provide eligible customers a 4% annualised percentage yield by lending out USD coin (USDC) to “verified borrowers.”

Coinbase says the SEC won’t explain its issue with the Lend program. “Rather, they have now told us that if we launch Lend they intend to sue,” according to the exchange’s post.

Read more here

Institutional Investors Dominated the DeFi Scene in Q2: Chainalysis Report

The decentralized finance (DeFi) market appears to no longer be the domain of retail actors alone as the institutional investment footprint in the crypto market segment continues to attain more significant levels.

According to blockchain intelligence firm Chainalysis, institutional investors played a major role in De adoption in Q2 2021.

In its soon-to-be-released “Global DeFi Adoption Index” report, Chainalysis stated: “Large institutional transactions, meaning those above $10 million in USD, accounted for over 60% of DeFi transactions in Q2 2021, compared to under 50% for all cryptocurrency transactions.”

Read more about the report here

El Salvador Purchases First 200 BTC, President Bukele Confirms

In a world-first, a sovereign state has purchased bitcoin. El Salvador is the first country in the world to recognize Bitcoin as legal tender, and the law was officially ushered in on September 7th. Despite opposition from local groups, the government believes crypto will be a net positive for the economy and society. The purchase is part of a new $150-million Bitcoin fund passed last week by El Salvador’s Congress. The fund will be used to facilitate conversions from BTC to United States dollars in the lead-up to the new law being implemented.

Read more here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.