Open Finance Mini Report

Market Recap

Gold Rallies This Week

Open Finance Mini Report

We have often referred to blockchain-based financial services as Decentralised Finance "DeFi". To some extent, many of the projects covered in this report are decentralised, but this limits the scope of what's actually going on in this vibrant ecosystem. In order to broaden the coverage of this report and avoid confusion, we will refer to this subsector of digital assets as open finance.

Open finance is a collection of basic conditional agreements called smart contracts that give expressiveness to our money. Smart contracts enable us to escrow, save, invest, spend, stream, borrow and trade with our money. This money encompasses the entire crypto taxonomy of money from centralised Stablecoins such as USDC to algorithmic stablecoins such as DAI, yield-bearing stablecoins such as aUSDC and cUSDC and even new internet commodity monies such as BTC or ETH. With time even central bank digital currencies "CBDCs" will benefit from open finance.

We strongly believe that open finance built on decentralised settlement engines such as the Bitcoin network or Ethereum are the future of finance for the following reasons:

Finance and technology are siblings who have grown up with one another. This idea that new companies that call themselves fintech are the first application of technology in finance couldn't be more untrue; if anything, they are at least the 3rd iteration of technology in finance. In reality, technology and finance have been interlinked and supportive of one another since the early 1900s. Blockchains are just the latest upgrade to the technology we use to facilitate financial services. Whether these services will be centralised or decentralised doesn't matter for now.

Blockchains eliminate the two most significant inefficiencies of our current internet infrastructure. The first is the high cost of transacting between intermediaries on the internet, and the second is the high cost of exiting/withdrawing assets from digital intermediaries. Solving these two problems will mean we get greater competitive forces when it comes to providing financial services on the internet. This greater degree of competition should lead to tremendous efficiencies for users over the long run.

Composability is a superpower of open finance; it is to software what compounding is to finance. Composable financial services mean that financial innovators can quickly combine and leverage any smart contract built on a blockchain to create their own innovative offerings.

Transparency is another superpower of open finance. When you use open finance applications, you can obtain high degrees of certainty over how your money or assets are used. This transparency gives us the ability to audit and observe these systems in real-time. So instead of waiting for quarterly earnings calls to realise your bank is insolvent, you can assess the financial position of any smart contract you wish to interact with from the comfort of your home. Over the long run, we see open finance as a regulators dream.

Access to open finance doesn't require permission; all a user needs is an internet connection, and with that, they can have access to money and all the expressions made possible by smart contracts.

Users will benefit greatly from transparency, easy access and more competitive forces in financial services. Entrepreneurs will benefit from composability and using software instead of administrative labour, bricks and mortar. Regulators will benefit from the real-time 24/7 ability to audit and monitor activities. Open finance is a win/win/win for almost all stakeholders except for incumbent financial services.

Open Finance Applications and Distributed Digital Intermediaries (A Primer)

The way open finance apps work is still a mystery to many; this is mainly because there isn't one single business model, token model or standard means of doing anything. We are very much in the discovery and experimentation stage of open finance. However, we are slowly beginning to see business models develop and exciting value accrual strategies coming to life.

Our simple framework for understanding these services and their tokens is as follows.

Every open finance app provides a service, e.g. the management of debits and credits, the matching of exchange orders or management of secured lending.

Every open finance app monetises its service in some way, shape or form, e.g., by charging a fee or providing access or discounts to token holders.

Like traditional businesses, many open finance apps carry residual interest in their treasuries. They can reinvest for growth, pay a dividend, or purchase their tokens off the open market.

Open finance apps are pretty similar to traditional financial service businesses when talking about value accrual, product-market fit, and strategic capital allocation of profits. They are, however, very different when we talk about governance, transparency of service, auditability and inclusion of stakeholders. Whether these differences provide meaningful competitive advantages is still to be determined, but we see this as an obvious advantage and asymmetric investment opportunity.

The Open Finance Landscape

As you read through the open finance landscape, keep the following in mind, open finance is a suite of financial services and products that follow rules. While complicated due to new terminology, all of these systems are simple in the rules they follow. These rules are written (in most cases) in open-source code.

Open-source is the fastest way to obtain "antifragility", every smart contract in open finance that holds any significant amount of money has an army of hackers looking for ways to exploit the contracts defences to extract the wealth held by the contract. This adversarial design environment means that developers have to build these systems to survive against numerous attack vectors which over the long run will bring robustness to the ecosystem.

Another thought to keep in mind is the assets that make up this open finance ecosystem and their astronomical volatility. If our traditional financial system experienced even half the amount of volatility we see in cryptoassets, it would break near instantly. It's been fascinating to watch open finance systems during large market drawdowns; even in the deepest and darkest moments of these drawdowns, all of the services remain operational.

Decentralised Exchanges

Decentralised exchanges sit at the centre of open finance, allowing users to exchange one asset/token for another. There are a variety of exchange mechanisms available in open finance, from the new innovative automated market maker (AMM's) to traditional order book exchanges. AMM's to date have been the popular exchange mechanism on the Ethereum network.

AMM's utilise a constant product function k = x*y which allows users to deposit two assets in equal weights into a pool and earn liquidity rewards for doing so. AMM's are far from perfect and, in almost all cases, end up constantly selling the outperforming asset and buying the underperforming assets, which gives rise to impermanent losses. In some cases, especially in highly volatile pairs, liquidity providers end up coming off second best as their liquidity rewards are less than the impermanent losses they experience.

However, AMM's are great for like-for-like pairs; for example, a USDC/USDT pool wouldn't experience much impermanent loss as arbitrators would quickly bring prices back into equilibrium. They are also great for early-stage projects which need to create liquidity for their token holders. Once a project issues a token, they need to provide a venue for these tokens to be traded; AMM's are a way for projects to do this without having to rely on market makers.

With the rise of high throughput blockchains such as Solana, we are starting to see the first real blockchain-based order book exchanges emerge. Serum appears to be the leader on this front, and many projects have come to utilise Serum's technology to create their own venues and user experiences.

Lending and Borrowing

Most if not all the lending that takes place in open finance is secured lending. The reasons, for now, are simple, open finance doesn't have a robust identity and reputation system as it stands. Without the ability to understand the creditworthiness of borrowers, we can't (or at least we shouldn't) provide under collateralised loans.

Secured lending still presents unique opportunities. At its most basic secured lending is the practice of lending money against some form of collateral where the lender earns an interest rate paid by the borrower. In the event the borrower is unable to meet their obligations, the collateral can be liquidated, and the lender can be made whole again. The overcollateralised nature of these loans means that there is no concept of counterparty risk as collateral can be easily liquidated. The risk of participating in this type of lending can be found in the design of smart contracts, the quality and liquidity of the assets supplied to pools and the operational efficiencies of the underlying blockchains and their oracle systems.

Many consider these projects peer to peer, but they can better be thought of as pool to pool, i.e. pools of lenders and pools of borrowers. Interest rates are set via a function of supply and demand for the asset of the pool. From a high level, where demand for the asset is high, interest rates will be high to incentivise lenders to provide more liquidity. Where demand is low, interest rates will be low, which incentivises borrowers to take advantage of cheap loans.

Asset Management and Yield

Asset management projects have taken many shapes and forms in crypto. Most of the asset management applications and protocols we see today are aggregators of various liquidity pools or lending opportunities.

Aggregating and batching the yield strategies of many within one protocol comes with many advantages, such as the ability to compound yields by regularly selling liquidity rewards and token rewards to reinvest. If individuals were to take on this challenge alone without the economies of scale and efficiencies offered by protocols such as Convex or yearn.finance, they would produce sub-optimal results.

Not only do asset management protocols offer a valuable service to those looking to earn yield, but they also offer a home to financial innovators who can easily propose new strategies and earn a share of that success.

Synthetic Assets and Derivatives

Potentially the largest addressable market for open finance can be found in the synthetic asset and derivative ecosystem. Many of these projects aim to create financial instruments in the form of ERC- 20 tokens that represent tangible or financial assets of the traditional world, such as gold or the S&P500.

Creating synthetic exposure to tangible or financial assets is nothing new, but creating these instruments on blockchains has proven to be more complicated than many expected initially. The majority of synthetic asset projects utilise collateral debt positions "CDP" to provide this synthetic exposure; whilst this has proved to be a workable route, it remains capital inefficient and creates poor user experiences. We see new implementations by projects like Float Capital that remove the threat of liquidations and complex CDP management with a more elegant novel mechanism.

Synthetic assets, especially those targeted at representing traditional securities, have run into regulatory hurdles and are awaiting clarity before continuing with development in this regard. Most of the synthetic assets we see today provide an easy means of shorting cryptoassets or provide opportunities for investors to run delta-neutral or similar hedging strategies.

The traditional derivatives market is enormous, and there's no doubt that as uncertain regulatory positions become clearer, these projects will really start to come to life by providing a global audience with access to any capital market on planet earth.

Core Open Finance Metrics

Total Users

Open finance adoption continues to show strong growth in 2021, with total users increasing from 1,172 million to 4,182 million, representing a 256% increase.

While much of this usage is driven by experimentation, many projects are cementing themselves as core pieces of the growing open finance ecosystem. The following metrics should shed some light on the scale of some of these services and illustrate the areas of usage and interest.

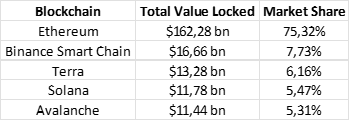

Total Value Locked

2021 saw a 1028% increase in total value locked in Open finance. We started the year with just over $20 billion locked up in various financial services climbing to highs of $270 billion.

As open finance continues to go multichain, we see increasing value locked up across the available smart contract platforms. Ethereum still holds the majority of the market share here, with 75% of the total value locked in the top 5 smart contract platforms.

Terra, Solana and Avalanche have seen explosive growth this year, and it's expected that they will continue to attract financial innovators and new users to their platforms.

Curve comes out as the dominant open finance project by total value locked for the year. Curve, which is an automated market maker similar to Uniswap and Sushiswap, specialises in like-for-like pairs such as stablecoin liquidity pools. Curve has directly benefited from the considerable growth of the open finance stablecoin ecosystem.

Total Exchange Volume

Decentralised exchanges have also benefited from general open finance adoption. In 2021 every month saw greater than $ 50 billion in exchange volume across numerous decentralised exchanges.

Over the past 12 months, decentralised exchanges have processed, executed and settled $981 billion in volume across 4,3 million unique trading addresses. Exchange aggregators such as 0x have also gained traction this year and makeup 15% of total exchange volumes.

Uniswap remains the king of decentralised exchanges, commanding 78% of all exchange volume. Sushiswap came in second with 7,7% of market share and then Curve with 5,7% of market share.

Total Outstanding Borrowed Volume

MakerDAO ends the year with the most outstanding borrowed volume on the Ethereum network ($9 billion) relative to Aave ($8 billion) and Compound ($7 billion). Please note these figures only represent borrowed volumes on Ethereum and do not include loans made on other chains; this means this chart understates Aave's total outstanding borrowed volume, which is closer to $11 billion.

Total AUM of Asset Management Protocols

Asset management protocols that provide high dollar-denominated yields have seen great success this year. Convex is the clear stand out for 2021, and its growth and dominance can be attributed to its mutually beneficial relationship with Curve Finance, the dominant stablecoin exchange and top open finance project by TVL.

Asset management protocols are an excellent example of the power of open finances composability. These projects leverage liquidity pools of exchanges and lending facilities to earn superior yield for users, shifting their allocations as better opportunities make themselves available.

Highest Earners

Most people who are new to crypto are shocked when they realise that there are many projects in the industry with a rich stream of cashflows. Total revenues in open finance can be split into three distinct categories supply-side revenue, demand-side revenue (uncommon) and protocol revenue.

Some projects such as Uniswap direct all revenues (exchange volumes * exchange fee (0,3%)) to their liquidity providers (supply-side revenue). The protocol itself doesn't take a fee and therefore has no protocol revenue. This is a strategic decision taken by the Uniswap community probably because the protocol holds a massive treasury that can be used for future development. Uniswaps total revenue for the year was $809 million, 100% of which was allocated to liquidity providers.

Other projects, however, do take a portion of fees to be held in the projects treasury or can be returned to token holders. DyDx burst onto the scene finding real product-market fit this year and the highest earner in open finance for token holders.

The highest earners represent a good mix of exchanges, asset managers and lending facilities. Please note protocol revenue is pre token distributions.

What to Look Out For in 2022

Open Finance is Becoming Chain Agnostic

2021 will be remembered for the rise of various smart contract platforms. Smart contract platforms provide settlement assurances with varying degrees of cost to security. Every smart contract platform is met with design tradeoffs between scalability, decentralisation, and security. 2021 has seen the rise of high throughput blockchains such as Solana and Avalanche that offer fantastic user experiences without the inefficiencies of decentralisation.

Whilst investors may look to invest directly into smart contract platforms; they can also look to the open finance sector to invest in this emerging multichain world. One can think of different smart contract platforms as separate nation-states that have different values and ways of reaching consensus over the state of their respective ledgers. Open finance projects have been taking advantage of this trend by spreading their service across different smart contract platforms.

This greatly lowers the risks associated with investing in open finance as they diversify their product across many possible future smart contract platforms. We expect this trend to persist into 2022 as cross-chain solutions continue to find new ways to make interacting between ecosystems seamless.

We can imagine a future where a user will open an application such as Aave and make requests for certain transactions, which will be executed at an optimal cost to security. The user, in this case, would be unaffected or unaware of the underlying smart contract platform being used.

Capital Allocation and Strategic Decision Making

2021 was all about growth and customer acquisition, 2022 will continue to build on these, but communities will have to get smarter with decision making if they want to survive the relentless competition of open finance.

We expect to see a lot more thought within communities as to how they can best utilise revenues to steer projects in a beneficial direction. Additionally, we have recently witnessed the rise of many new token incentive mechanisms pioneered by OlympusDAO, which have raised many questions in the industry as to what the best means of distributing one's token looks like.

Many of the projects have essentially been issuing very expensive equity "tokens" for very little community engagement and real buy-in. Many of the participants who help bootstrap these protocols aren't active in the community but rather participate as mercenary capital who will shift liquidity as opportunities become available. Perhaps these aren't the type of investors projects you want holding large amounts of tokens, primarily if projects use token voting to govern the future trajectory of the network.

In 2022 investors should pay careful attention to how projects distribute their tokens, whether this will be beneficial, and how communities allocate protocol revenues. Getting these two right is how these projects will accrue meaningful value.

Risks of Open Finance

Regulation

Financial regulators, especially those in the United States, have taken a rather negative stance on open finance. It's important to remember that these individuals aren't paid to take risks and therefore are in no hurry to give this young industry clarity. The language and general conversations around open finance have been riddled with miss understandings of the inner workings of many of these projects.

Currently, open finance projects will be required to comply with requirements expected of virtual asset service providers (VASP's). These requirements are detrimental to many of the core value propositions of open finance.

A lot of attention is on stablecoins which by design are superior to commercial bank deposits in many ways, yet regulators choose to ignore these innovations. A potential scenario for open finance regulation is strict laws around stablecoin issuance and usage. This could lead to projects like Circle's USDC having to whitelist SEC approved open finance projects. Anything not whitelisted just becomes a venue where USDC itself can't be used. This is purely speculation, and only time will tell us what direction to expect these regulatory bodies to take.

While countries like the United States of America have taken hard positions, other jurisdictions such as Luxembourg, Germany, Portugal, El Salvador, Bermuda, and many others have taken forward-thinking positions fostering fertile environments for entrepreneurs.

Functional Equivalence and Adoption

The past five years have sandboxed open finance development with a very lenient user base. Most of the early users of these financial services have been willing to deal with the inefficiencies inherent with early-stage technology.

As open finance diffuses through new user groups, it will be held to a higher standard. The early majority will quickly dismiss projects if their service offerings a sub-optimal when compared with fintech and traditional banking solutions.

The industry will have to work hard to scale to lower costs around settlement and focus heavily on ensuring that users have positive experiences when interacting with open finance.

Lack of Transparency and Best Practices

Whilst much of open finance is open source and transparent, there are just as many projects that lack transparency. This industry isn't localised, and it isn't easy to control and establish best practices. This creates a need for self-governance and regulation, not in the form of innovation inhibiting rules and licenses but rather an urge from within to make as much relevant information available to the public as possible.

Projects that make decisions behind closed doors or refuse to open source their contract designs should be avoided. Founders and team members of projects should strive to join communities such as Messari and add their profiles to the Messari registers. This doesn't mean that every project listed on a website like Messari is legitimate, but at least it signals to users a willingness to be open and comparable to similar projects.

Additionally, projects can create Dune Analytics dashboards that allow users to view the progress and financials of a project in real-time.

If you are a crypto project and would like to be registered on the Messari asset registry, or you are looking to create Dune Analytics dashboards, please feel free to reach out.

Notable Articles and News Stories This Week:

Federal Regulator Says Credit Unions Can Partner With Crypto Providers

Federally insured credit unions (FICUs) can partner with third-party digital asset service providers, the National Credit Union Administration (NCUA) announced Thursday.

“This includes facilitating member relationships with third parties that allow FICU members to buy, sell and hold various uninsured digital assets with the third-party provider outside of the FICU,” according to the statement from the NCUA. The NCUA is a U.S. regulator that oversees credit unions, acting as a counterpart to the Office of the Comptroller of the Currency (OCC), which regulates national banks.

The NCUA said it wants to offer clarity around the existing authority that FICUs have when it comes to building relationships with third-party digital asset providers. The NCUA said further guidance may be necessary as digital assets and technologies evolve, and the association will continue to study and address issues that arise.

Read more about the announcement here

Ray Dalio: Crypto Should Be Part of a Diversified Portfolio

Ray Dalio owns bitcoin and ethereum, he said during an interview with Yahoo Finance, and believes that crypto has a place in portfolios.

The founder of hedge fund manager Bridgewater Associates — and the firm’s CIO since 1985 — declined to specify how much bitcoin and ether he owns.

Though he indicated he doesn’t own a lot, he said he views it as an alternative money in an environment in which the value of the dollar is depreciating in real terms.

“I think it’s very impressive that for the last 10 or 11 years that programming has still held up,” Dalio explained. “It hasn’t been hacked … and it has an adoption rate.”

The hedge fund executive said he encourages diversification during the Yahoo Finance interview, noting that crypto is “a relatively small part of the portfolio.” He called cash the worst investment, noting its loss of buying power.

The Consumer Price Index (CPI) rose 0.8% in the month of November — the fastest pace since 1982 — putting inflation at a 6.8% increase over the year.

Read more of his comments here

ConsenSys Collaborates With Mastercard on New Ethereum Scaling System

Ethereum software firm ConsenSys has launched “ConsenSys Rollups” with the help of Mastercard’s engineering team to enable expansion on both the Ethereum mainnet and for private use, ConsenSys said Thursday.

“ConsenSys Rollups is an innovative modular software solution for permissioned blockchain applications focused on providing scalability and privacy capabilities that can be connected to any Ethereum Virtual Machine (EVM) compatible blockchain,” according to a company statement.

ConsenSys also said systems built using Rollups can reach a throughput of up to 10,000 transactions per second (TPS) on a private chain, compared to only 300 TPS on private chains without Rollups and 15 TPS on the Ethereum mainnet.

ConsenSys Rollups also offers “strong privacy protections to both enhance solutions for existing use cases and enable new use cases,” Madeline Murray, global lead of protocol engineering at ConsenSys, said in the statement.

Read the full story here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.