It’s So Over, Right?

Crypto obituaries, signs of a bottom and bull market narratives.

I spent last week with the team in Mauritius. We spent our time discussing market conditions and thinking about the path forward for the asset class. This memo summarises those thoughts.

BTC and ETH have been in a bear market for six months, the broader asset class has been in a bear market since January of 2025. The crypto obituaries are rolling in almost everyday now, as with every obituary before 2026, the narratives behind these calls are compelling, especially when weak price action lends them credibility.

I have been around long enough and heard enough of these arguments to know that betting against them is a solid strategy. In fact there is even a website dedicated to just that and the stats are truly illuminating.

Bitcoin has been declared dead 467 times by reasonably well known sources. (Probably way more in other parts of the internet and corporate board rooms)

If you invested $100 every time an obituary was published that portfolio would be worth $69m today…

This time must be different, right?

The narratives backfilling today’s price action are quantum fears, value capture fears, the four year cycle and a new Fed Chair who apparently will not print money and rather just let nature take its course. I have even had people ask me if Epstein is Satoshi. From where I sit, these narratives are consensus, nothing new and are becoming exhausted. More importantly the big ones quantum and value capture are resolvable and market signals of crashing prices have merely increased the urgency to find resolutions.

This market is doing exactly what it always does, deep drawdown, tests your conviction, rips faces off and repeats. We are only 17 years into the blockchain movie, it’s easy to look at crypto charts and over index to all the fear mongering and narratives attempting to explain it. It took the Nasdaq 17 years to 5x, 17 years of fear, doubt, ridicule and uncertainty before becoming one of the great investment stories of all time.

My thesis has and will continue to be that BTC and ETH are new superior forms of money, built specifically for an era dominated by cyberspace over meatspace, in 2026 even intelligence is moving into cyberspace. Money is the best product in the world, the reason Gold remains the largest single asset in the world is simple, everything else orbits around it. The same will be true for the economies built on BTC and ETH and like Gold the aggregate sum of businesses built on top of them will be massive.

Crypto in 2026 is back where we like it, contrarian, hated and dismissed by weak regurgitated consensus arguments or headwinds that can quickly become tailwinds. When I started out in crypto, I would always say to people that every reason or smart idea they had for why crypto would fail was just another business opportunity waiting to be solved by an entrepreneur. I still hold this view. Being long crypto is being long human ingenuity, it’s a global code enforced monetary and trust network emerging during a time of great uncertainty and the collapse of the old rules based order.

The Bottom is in or Close to Being in

We are hitting historical extremes across a variety of indicators. The recent downturn has been six months of consecutive red candles. The most difficult part of this is that the environment and the front windshield have been positive for crypto, this makes the doomsday narratives much more pungent, it opens the conversation to whether something structural about crypto has broken.

Crypto conditions index remains positive.

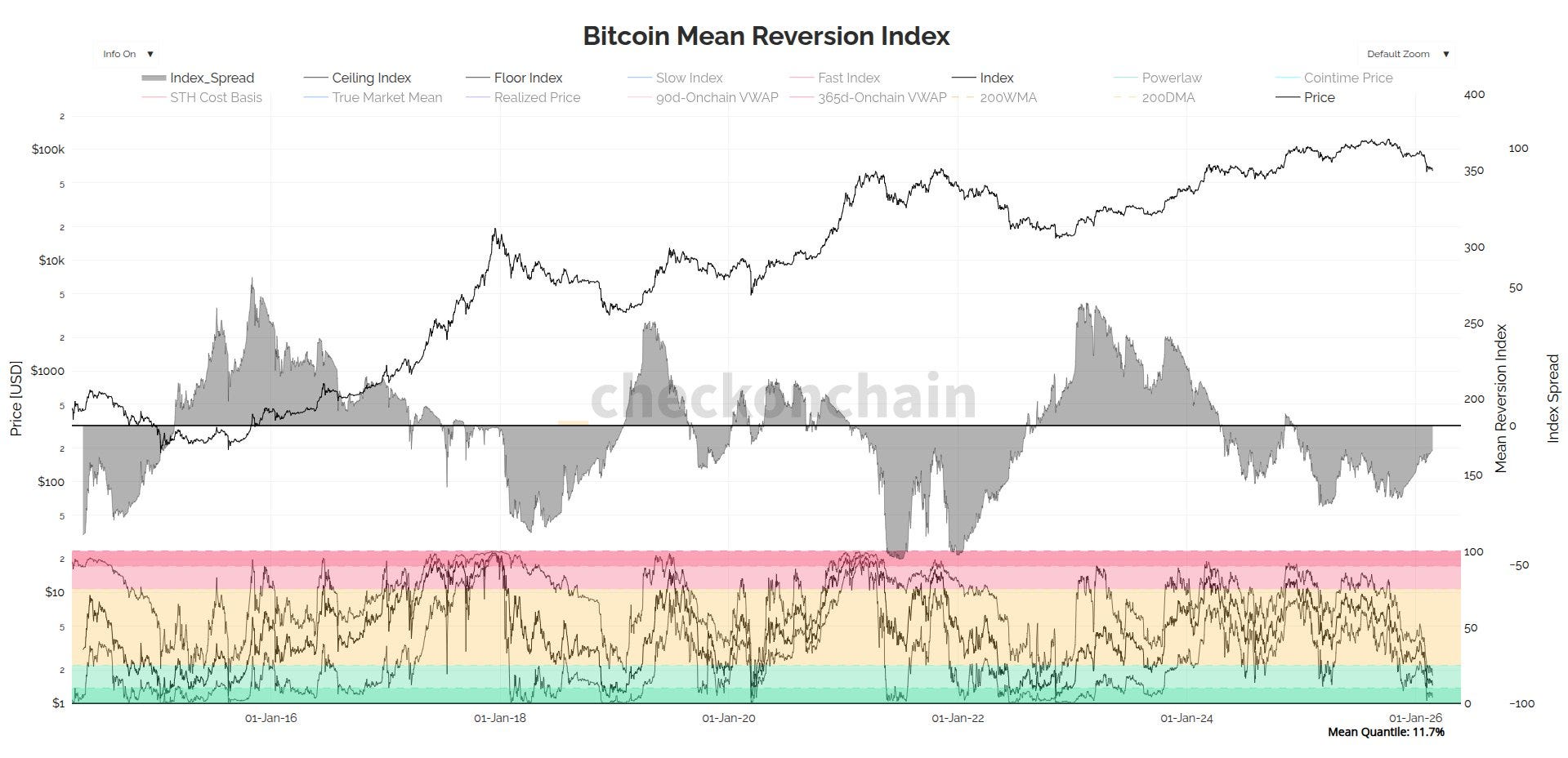

BTC RSI at extremely oversold levels and price is retesting 2021 highs

BTC is now trading at production cost, a historical floor price.

Every mean reversion model, from technical to onchain, is trading within bottom formation levels, typically seen after the price capitulation event ( Dec 2018 and Jun 2022).

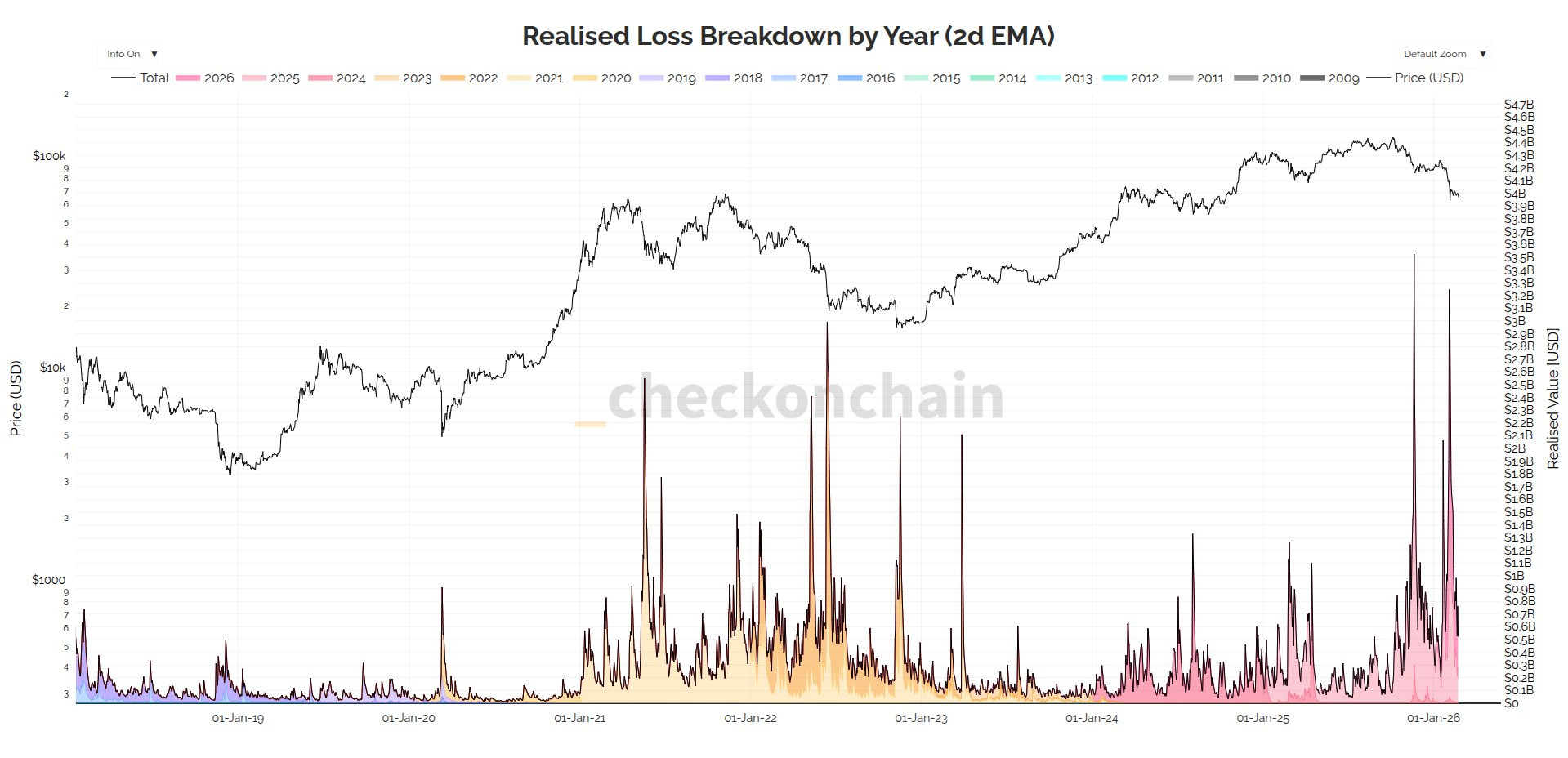

Both sell-offs in November and February are in the all time greatest realised losses onchain, a true capitulation that is potentially exhausted.

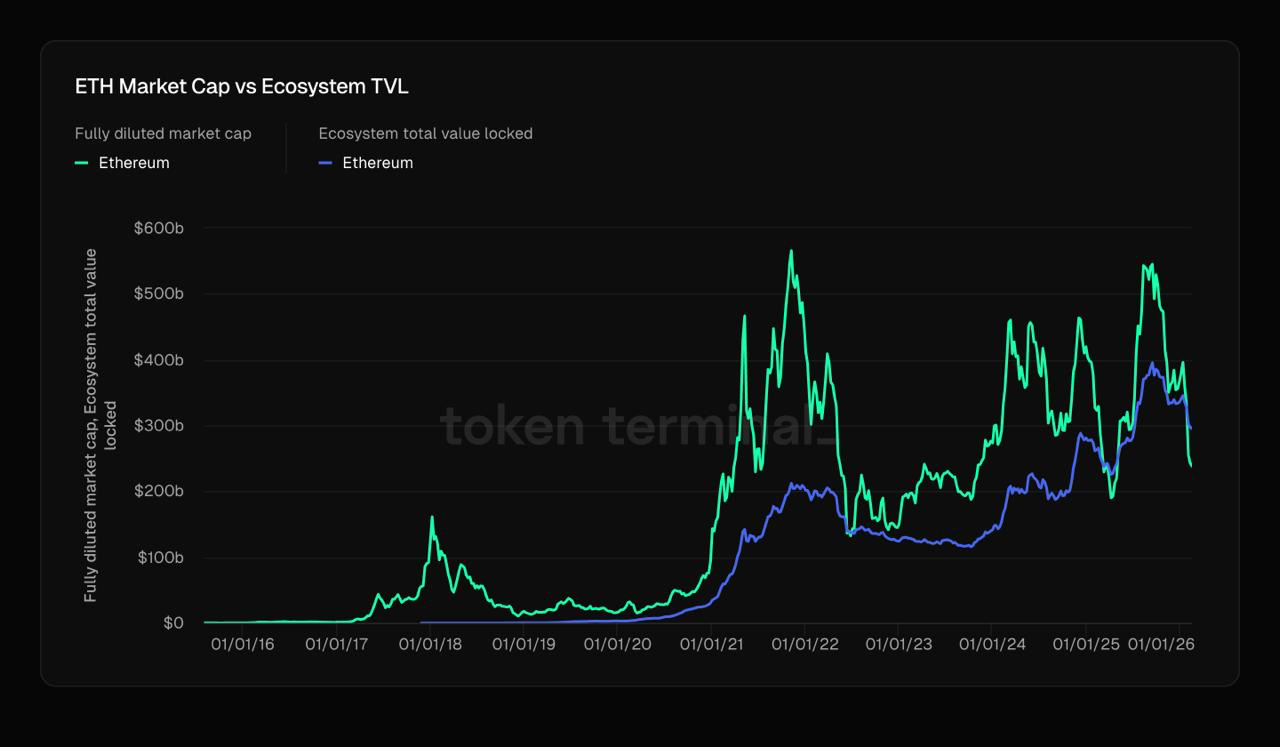

ETH is now trading below the value it secures in smart contracts.

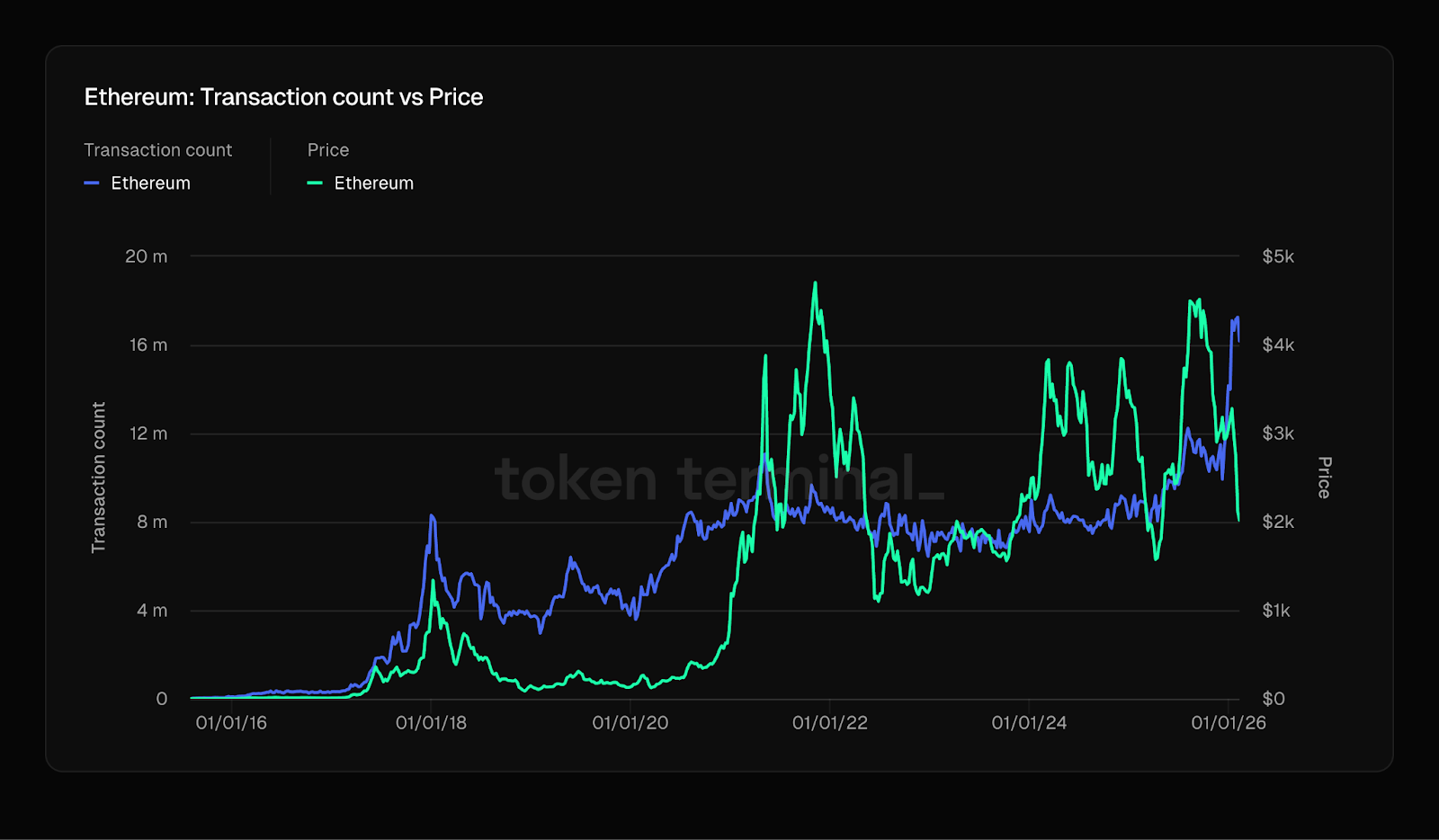

ETH transaction activity continues to trend higher.

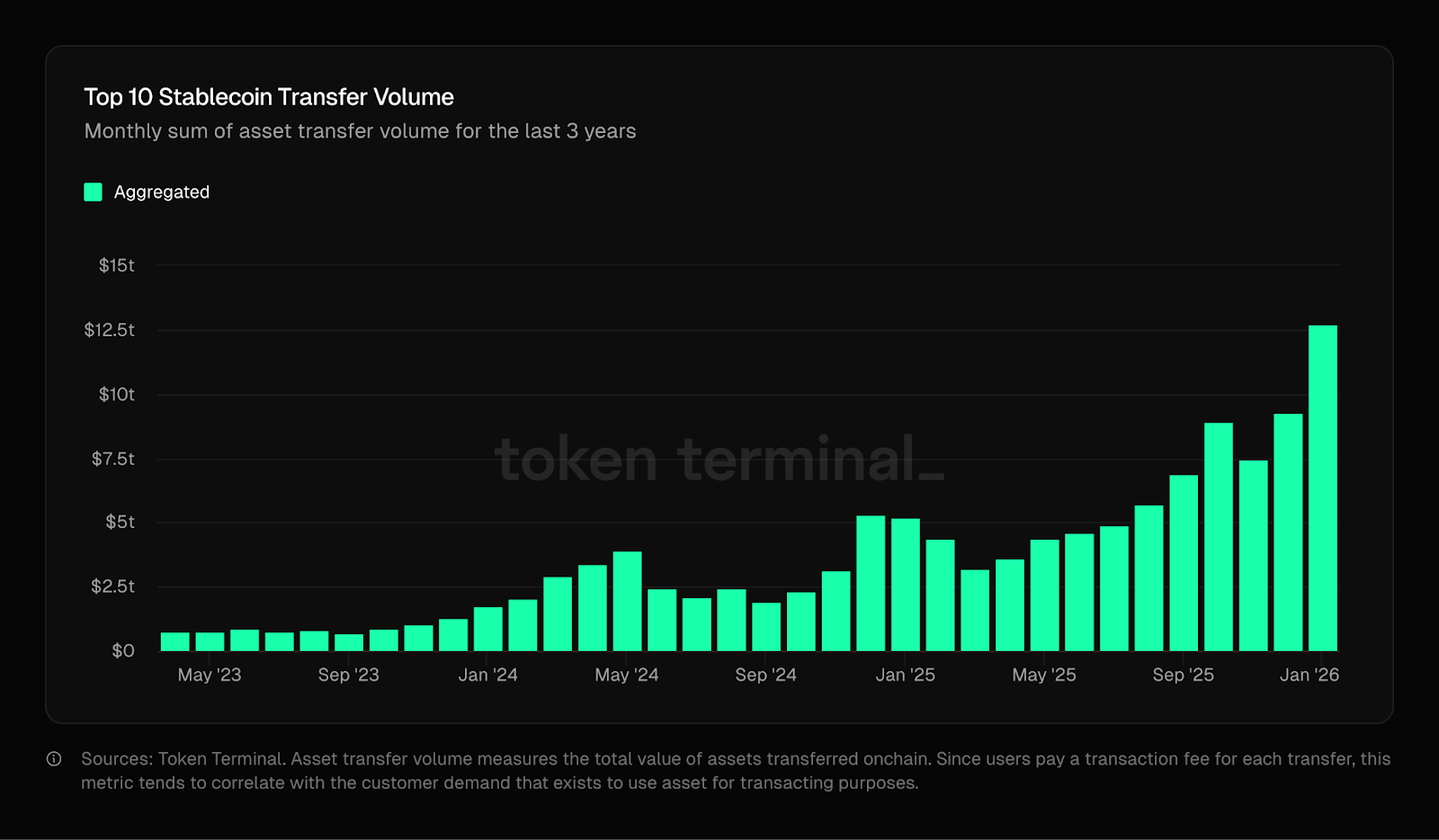

Stablecoin transfer volumes are exploding, blockchains processed over $10T in stablecoin volumes in January alone.

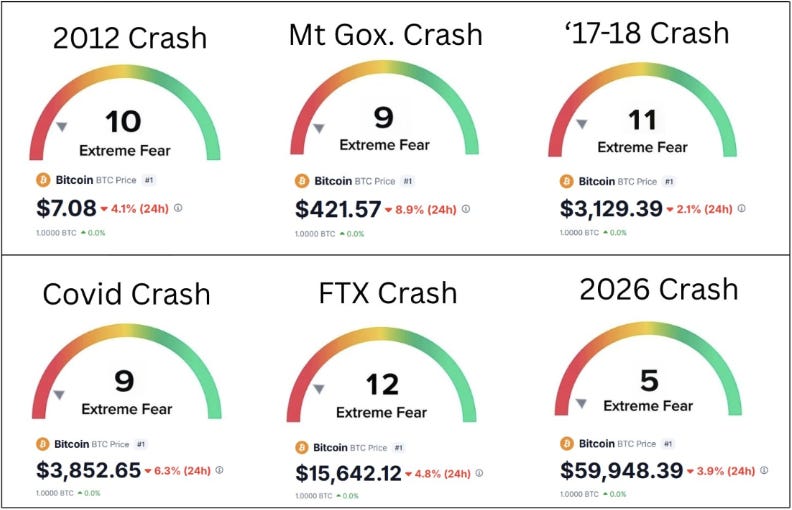

The fear and greed index has hit its lowest levels ever recorded. Just think about that, more fear today than during a global pandemic and the FTX bust…

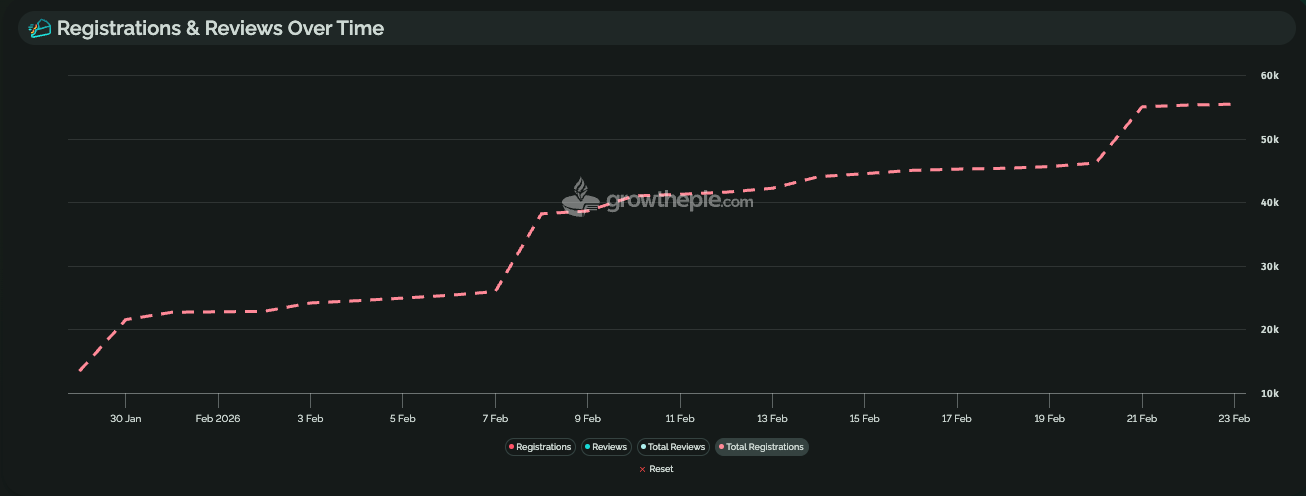

A new mega trend is emerging, AI agents coming onchain. Over 50k registrations so far.

This is the inflection point, sentiment in the gutter, crypto obituaries all over and the seeds of the next bull in sight.

Narratives Of The Next Bull Market

This was the biggest talking point during our offsite, the idea that the map is not the territory. The realisation that price (the map) shapes narratives, capital flows and even the fundamentals themselves. I see this dynamic everywhere I go, the fear of missing out (when it’s rising) and the fear of more losses (when it’s falling). The “I wish I bought back in April Tariff Tantrum, when it was dead” at $126k and the “It’s getting commoditised, quantum, Satoshi is Epstein” at $60k.

We are so quick to point out drivers of price but in reality it’s never one thing, but rather price reinforcing a collection of stories. I think this best describes crypto today.

The reality is more supply has come to market than demand has met it. But this dynamic can quickly reverse, and it is positioned well to do so given the amount of capitulation we have seen. The market has become blind to the positive catalysts on the horizon, as price action continues to reinforce the bear cases. All it takes is a few good trading sessions for these positive narratives to take hold and change the story.

The first is blockchains becoming the center of payment settlement. Stablecoins usage is exploding, 50m active addresses doing over $120T in annualised volumes.

The second will be blockchains becoming the center of asset settlement. Whether its tokenised funds, commodities, stocks or bonds, blockchains are just a better, faster and cheaper way to settle these instruments and open will win because it reinforces itself. You don’t want to be on a local network, you want to be ON THE NETWORK, and it’s called Ethereum.

The third will be the shock and horror of Kevin Warsh turning on the printing press at the first sign of liquidity stress. This anxiety that Warsh will embrace his inner libertarian and let nature take its course while Trump occupies the White House is one of the worst reads on the market I have ever come across. As Lyn Alden so eloquently says, nothing stops this train. The system is geared 50x, a 1% deleveraging in 2008 is known as the Great Financial Crisis, a deleveraging is not a viable path. Net payers of tax don’t want to vote for higher taxes and net tax recipients don’t want to vote for less entitlements. The most likely path ahead continues to be excessive money printing.

The fourth will be the embrace of the DeFi Mullet, I wrote about this in Chain Street (Part 4). More and more fintechs and forward thinking financial firms will embrace blockchain as a backend, not just for asset issuance but for utilisation in lending, borrowing, exchange, asset management and derivatives.

The fifth is regulatory clarity and a resolution to protocol business models. I underestimated the damage Gary Gensler’s SEC reign and predatory VCs did to business models in crypto. The problem was further exacerbated by memecoins and scams. The consensus today is that protocols won’t change their business models and that they will become invisible but vital infrastructure like TCP/IP. What if they do change their business models when regulatory clarity arrives and they are finally allowed to do so? What happens if protocols are more like AWS, invisible and monetised via usage fees? What if I told you they are already doing so? More on this in Chain Street (Part 5) on Token Rights.

The sixth is the one that takes us to insane price targets, it’s the latent demand that we couldn’t have possibly forecasted, its AI agents coming onchain. As I was writing Chain Street, I came to two realisations, the first was that Chain Street is written for a human to human future, it encapsulates the original peer to peer, trust minimised future enabled by blockchains. The second was that blockchain was never meant for humans. This will be the topic of my next series, Agentic.

I think we are completely and utterly underestimating the demand for blockspace over the next decade. The Jevons Paradox is an economic theory stating that as technology increases the efficiency with which a resource is used, the total consumption of that resource increases rather than decreases. This occurs because higher efficiency lowers the relative cost of using the resource, leading to increased demand and, often, new applications for it. The resource in this case being trust, coordination and the ability to transact, blockchains collapse the cost of doing these things into a single gas fee and AI agents will super charge its usage.

My equity friends keep flagging low Ethereum fees in an environment where usage is surging. My answer is simple, Ethereum is building capacity, and we are going to need a lot of it. You are underestimating the future usage that this network is going to attract.

Keep a lookout for Chain Street (Part 5) where I will get into the weeds on Token Rights.

While it’s easier to look away, seeking to understand is the only path to a more enlightened and empowered world. Change is now exponential and blockchain technology sits at the centre transforming money, finance and what it means to sovereign. Join me in exploring this new world by subscribing.

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments. Collective Investment Schemes (CIS) are generally medium to long term investments. The value of participatory interests may go down as well as up. Past performance, forecasts or commentary is not necessarily a guide to future performance. As neither Lima Capital LLC nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice.