Government Money

Market Recap

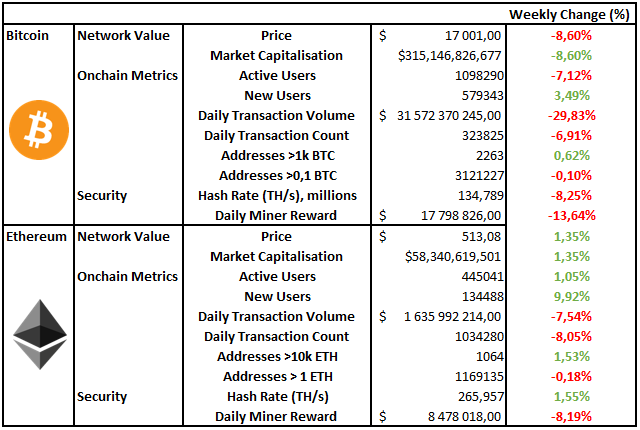

Digital Assets Take A Break After BTC Tries All Time Highs

Government Money

Our goal this week is to layout the archetype of government/state money and how they manifest in the short and long-term debt cycles. Reading financial history paints a gloomy picture for the longevity of any form of government money. There are very few examples, if any, of a state money system that was sustainable over the long term.

Before digging into the plumbing, we will make some assertions. These will enable you as a reader to look at central banking for what it is, a monopoly over the supply of a public good that is used to store, exchange and account for value.

Assertion 1: Change Starts with The Individual

Money is energy in the form of stored time. Like energy, money must abide by the laws of thermodynamics. It can neither be created nor destroyed but merely transferred or changed from one form to another.

Governments cannot create wealth or value for the individual. The individual is the only one who can do so by providing goods or services to the market. When governments pretend that they can create this wealth, those that are struggling financially wish it to be true.

People always search for someone to blame for their own shortcomings, whether it be pointing fingers at immigrants, a certain race, the poor or the wealthy. Governments use this division and mistrust, effectively weaponizing our own fears to their advantage.

The truth is that good things start with individual effort not a government stimulus check.

Assertion 2: Capitalism and Socialism

Capitalism at its most basic is an economic system whereby market participants have exclusive rights to the fruits of their labour. They own their time, sacrifice, and effort.

Socialism implies the state and people own the capital of the collective with the intention to benefit the individual. As an individual, you no longer own your time, sacrifice, or effort. Historically, central powers that attempt to use the collective’s capital have often ended up acting in their own self-interest, enriching themselves instead of benefiting the individual.

We could argue that the West does have free-market capitalism, however, the monetary system that we use to store, exchange and account for value is a centrally governed network. It is monetary socialism.

Assertion 3: The Gold Standard Didn’t Fail, Trust Did

It’s fascinating that when discussing the end of the gold standard the main reason cited for its failure was its inability to support a fast-growing economy. After World War 2 America had amassed nearly two-thirds of the worlds gold supply, this allowed them to take on the privileged position of establishing the US dollar as the global reserve currency at Bretton Woods.

The US dollar at that point was commodity money. Every US dollar was an IOU with a claim on the gold that backed it. America had been entrusted with managing the ratio of IOU’s to physical underlying gold. The world had agreed to one thing with America and that was to preserve the relationship between the amount of paper money in circulation and the gold reserves they held.

The gold standard didn’t fail because gold is a poor form of money. The gold standard fell apart when the French president, Charles de Gaulle, requested that America redeem France’s gold for the dollar notes that France held in its reserves. Richard Nixon, the president at the time realised the systemic danger of France’s request. It was dangerous because America’s centrally planned monetary system had abused the trust the world gave them at Bretton Woods. They had created too many IOU’s and didn’t have enough physical gold to pay out all the claims.

America announced that in the best interests of the American people, they would stop the convertibility of US dollars to gold. People across the globe had been providing years of work, time, and effort to accumulate US dollars or their local fiat currencies which had a fixed peg to the dollar. Overnight their money was no longer what they were promised it to be.

The US dollar we use today was therefore conceived and founded on deception.

Assertion 4: Debt is Both Good and Bad

Debt is an essential component of capital formation; without it, we would not have been able to create the world we have today. When discussing government money, we have to talk about debt, after all, every unit of government money is an IOU, it is debt.

Debt is a powerful tool and if used correctly can benefit the whole. Debt, however, is incredibly reflexive, when debt is used for productive means it produces great benefits for society. This then begins to reinforce the idea that the route to further productivity is more debt. This cycle will continue to reinforce itself until we can no longer increase our productivity.

When we reach this point, the very tool that enabled us to increase our productive abilities becomes self-defeating. This happens when our collective incomes are growing slower than the rate that our debt is growing. It begins with malinvestment as we saw in the 2000 tech boom and the 2008 housing crisis; debt is no longer being used to finance productivity but rather used to finance other debt.

The personal finance lessons of the individual are no different from those of the state. Save more than you spend, only use debt to finance productive activities that will produce a rate of return greater than the cost of capital.

Think about it this way, if governments truly couldn’t default on their debt then why does poverty exist? If we could theoretically continue to extend our debt beyond our production capabilities, why is it something we have only discovered in the 21st century?

Were all those that came before us short-sighted?

Assertion 5: People Want to be Told How to Value Things

People rely on authority and familiar figures to do this. So, here is a collection of some familiar and authoritative figures and their thoughts on our monetary system:

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

― Henry Ford

“I sincerely believe that banking establishments are more dangerous than standing armies, and that the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”

― Thomas Jefferson 1816

“I am afraid that the ordinary citizen will not like to be told that the banks can and do create and destroy money. And they who control the credit of a nation direct the policy of governments, and hold in the hollow of their hands the destiny of the people.”

— Reginald McKenna 1924

“The modern banking system manufactures money out of nothing. The process is perhaps the most astounding piece of sleight of hand that was ever invented. Banking was conceived in iniquity and born in sin. Bankers own the earth. Take it away from them, but leave them the power to create money and control credit, and with the flick of a pen, they will create enough money to buy it back again. Take this great power away from the bankers and all the great fortunes like mine will disappear, and they ought to disappear, for this would be a better and happier world to live in. But if you want to continue to be the slaves of bankers and pay the cost of your own slavery, let them continue to create money and to control credit.”

— Sir Josiah Stamp, a former Director and President of the Bank of England.

“I am a most unhappy man. I have unwittingly ruined my country. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated Governments in the civilized world no longer a Government by free opinion, no longer a Government by conviction and the vote of the majority, but a Government by the opinion and duress of a small group of dominant men.” –

— Woodrow Wilson, after signing the Federal Reserve into existence

The Short Term Debt Cycle:

This cycle is usually referred to as the 5 to 10-year business cycle. Our universities, governments and financial institutions refuse to call it the credit cycle because this would illustrate to the everyday individual the power that credit providers have.

The cycle begins with entrepreneurs, businesses and individuals recovering from a recession. As the recovery ensues, they begin to take on more leverage and risk.

This levered position assists in fast growth and is often met with rising asset prices. However, it also leaves people fragile to negative shocks or a slowdown in spending. Fragility combined with a negative catalyst triggers defaults and eventually the bankruptcy of those who took on too much risk.

As negative shocks occur the private sector experiences a deleveraging event, the credit they used to build businesses or buy things now becomes impossible to service and capital is destroyed. The money they borrowed was someone else’s deposit as for every liability there is an asset. This deleveraging is deflationary, and governments hate deflation.

So, they begin to intervene. Governments need to fill this hole of destroyed capital in an attempt to keep lenders whole, the decrease in leverage in the private sector is matched by an increase in leverage in the public sector. Federal debt increases rapidly because their tax revenues fall as economic output shrinks whilst at the same time due to the recession they need to spend more.

When the economy is operating normally and we are early in the longer-term debt cycle, the response and tools used are the lowerings of interest rates and fiscal support from the treasury. These activities actually promote further leverage in the private sector and the cycle begins again.

The main takeaway of the short-term debt cycle is that at the beginning of every new cycle there is still more debt in the system than there was in the cycle that preceded it.

The Long-Term Debt Cycle:

Whilst most people reading this will be well versed in the short term debt cycle, which many have probably seen many times in their own lives, it is less common to come across someone who has lived through many long term debt cycles.

These cycles usually take 50-70 years. Ray Dalio, a well-known and incredibly successful hedge fund manager has written about this in great detail. You can download his book “Principles for Navigating Big Debt Crises” here.

After many short-term debt cycles, the continuous lowering of interest rates, and further federal debt expansion, the amount of debt in the system relative to GDP becomes excessive. Eventually, interest rates hit the zero bound as seen in the 1930s, 2008 and now in 2020. This is where things start to change and the tools that central banks and governments used to avoid previous recessions struggle to have similar stimulative effects.

Once the zero bound in interest rates is hit, governments have a difficult time trying to push them lower. We have seen many countries enter negative interest rate territory; this essentially means savers are paying borrowers to borrow. This represents a breakdown of the first principles of debt, it makes the cost of money effectively zero.

Take a moment to reflect on what happens to present value calculations when the cost of capital is zero and, in some cases, negative. Present values of assets begin to swell as all their future earnings are added up and reflected in today’s price, leaving truly little room for further growth.

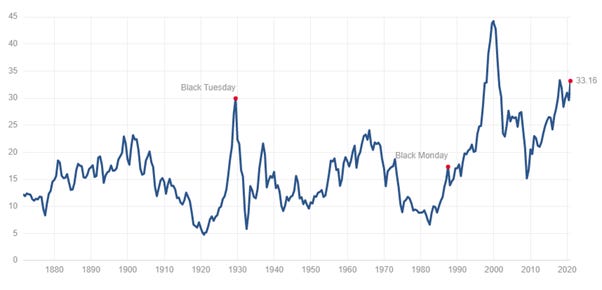

This is where malinvestment occurs because essentially any venture is now worth pursuing as the cost to finance it is zero. The figure above is the cyclically adjusted price-earnings ratio of the S&P500 which shows how these macro factors prop up stock market prices. The combination of fear over future inflation and elevated valuations due to interest rate manipulation cause assets like the stock market to skyrocket in the currency they are denominated.

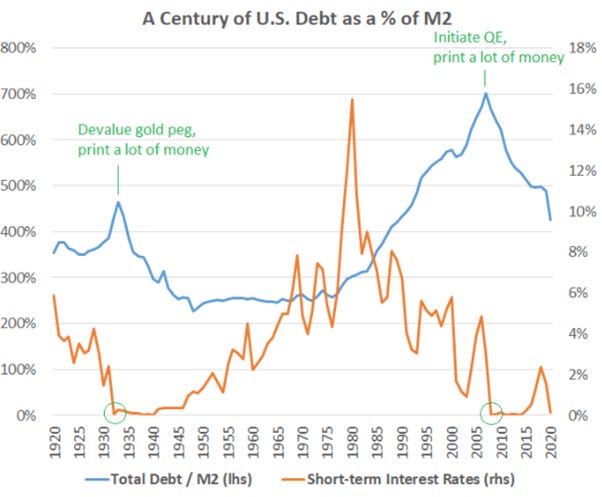

The figure above shows the relationship between total debt and M2 money supply. M2 is a broad measure of the amount of money in the system. In a normal recession when system-wide leverage is low, we can deleverage nominally. Those who took on too much risk fail and file for bankruptcy, all while innovative competitors enter the market and creative destruction ensues.

However, when there is a vast amount of system-wide debt from the sovereign to the household, it becomes exceedingly difficult to default nominally because this would cause a complete breakdown of the entire system, something I don’t think any of us would want to see. Instead, these peaks in debt to GDP tend to be delevered in real terms through massive monetary expansion.

At the end of the long-term debt cycle, we expect to see nominal debt reduce slightly but the amount of money in a system to increase dramatically.

In a study done by Hirshmann Capital, it was found that over the last 200 years there have been 52 examples of countries that have exceeded debt (government debt) to GDP ratios of 130%. Out of these 52 countries, 51 defaulted within 15 years of breaching these levels. The United States is projected to hit 141% government debt to GDP by the end of 2020.

This default can happen in a couple of ways:

1. A hard default- this would be a nominal default, one where capital is nominally destroyed. It would be the least socially acceptable way of dealing with the problem. Depositors/savers would take an absolute beating and not be returned the same nominal amount they invested.

2. A system-wide debt restructuring- whilst a “jubilee year” is possible, this event would involve governments writing off large amounts of debt. Depositors and savers would once again bear the brunt of the government’s decision.

3. A soft default- this seems to be the most likely possible path for governments to undertake. It’s the magic trick of finance, the most socially acceptable way to default. Instead of nominally reducing debt we can instead attempt to inflate it away by destroying the value of the currency it is denominated in. It’s socially acceptable because depositors will see their savings go up in nominal terms. However, what this money can now buy them is more than likely nothing compared to what it originally could.

So, what are bond buyers and fiat currency holders doing right now? They are buying bonds at record high prices at a time where the sovereign is least likely (98% probability based on 200 years of evidence) to be able to pay down these debts.

Risk-free? I think not.

Over the next three weeks, Etherbridge will take you through the above cycle and show you how it plays out in practice. We will use the rise and fall of our last three world superpowers, The Dutch Republic, British Empire and finally the USA to show how this archetype repeats over time.

Notable Articles and News Stories This Week:

BlackRock’s Chief Investment Officer Says Bitcoin Could Replace Gold to a Large Extent

The CIO of Blackrock Rick Rieder (the world’s largest asset manager) has stated that he believes digital assets are here to stay. He even goes as far as to say that it may at some point in the future replace gold as an investment due to its functionality. In an extract from the interview, he states, “Do I think it's a durable mechanism that ... could take the place of gold to a large extent? Yeah, I do because it's so much more functional than passing a bar of gold around".

Read the article here

Ethereum 2.0 Deposit Contract Secures Enough Funds to Launch

Ethereum is currently in the process of transitioning from a Proof of Work to a Proof of Stake consensus system dubbed Ethereum 2.0. This should increase its usability and help it scale to a greater extent. It has been a slow process ensuring that everything works as expected and there are no bugs in its code. This week they secured the amount of Ethereum to launch the first phase of Ethereum 2.0, something that the digital asset world has been very excited about for a long time.

Read about the upgrade here

Janet Yellen Is About to Become Bitcoin’s Greatest Ally

According to Morgan Creek Digital co-founder Anthony Pompliano, the appointment of Janet Yellen is “bright” for bitcoin. He believes that whether or not the dollar is actually inflated the fear that it may be devalued is enough to cause a rise in the bitcoin price. Anthony goes on to state: “Essentially, Janet Yellen is likely to be Bitcoin’s greatest ally over the coming 4-8 years. She has never seen an opportunity to print money that she didn’t like. She has never seen a situation of high inflation that scared her. Given that we are currently living during a period of high unemployment due to the coronavirus, it would be my expectation that Janet Yellen will begin pulling out every tool of monetary stimulus to get unemployment lower.”

Read the full explanation here

PayPal CEO Schulman Say He’s Bullish on Bitcoin as a Currency

The CEO of PayPal Dan Schulman believes that bitcoin’s usefulness as a currency will eventually prevail over the buy-and-hold mentality that we are currently witnessing. PayPay has recently launched a service that gives consumers the ability to buy, sell, hold and pay merchants with their digital assets. Schulman said central bank digital currency is a global inevitability. As that happens, "you'll have more and more utility happen with cryptocurrencies," he said.

Read the story here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge we aim to lower the barriers of understanding this fast-growing digital economy.

If you are interested in staying up to date please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.