Chain Street (Part 5) - Token Rights

What am I even buying? Classification and holder revenue on Chain Street.

This is part five of a series on Chain Street.

Chain Street (Part 1) - The Opportunity

Chain Street (Part 2) - The Challenges

Chain Street (Part 3) - Open vs Closed

Chain Street (Part 4) - The DeFi Mullet

A Framework For Clarity

Before we get into the business of Chain Street, I want to give you a lens through which to view it.

The Three Sigma team developed a classification framework for protocol tokens that I’ve found genuinely useful. Let’s walk through it.

Every time you encounter a token on Chain Street, you’re really asking a single question: what am I actually buying? The Three Sigma framework breaks that question into four layers, each of which will develop your understanding of where value lives and whether any of it will ever reach you.

The first layer is structural. Is the token transactional or non-transactional? ETH is a transactional token, the Ethereum network doesn’t function without it. Most Chain Street protocol tokens are non-transactional. They aren’t essential to the protocol’s day-to-day operations, which immediately tells you that their value isn’t in powering the protocol but rather in serving as a claim on value flows, and that this needs to be explicitly designed for.

That design question is what the next three layers reveal. What value flows are even on offer? Inflationary rewards, a revenue share, governance rights, or some combination? How do you actually access those value flows? Do you need to stake, and if so, is that a hard lockup or can you exit freely? And finally, how does the money move? A dividend paid in stables or the protocol token, a buyback, a burn, or quietly accumulated in a treasury where it may never reach you at all?

Run every token through that sequence: transactional or not → what rewards exist → how to access rewards → how they reach you. It won’t necessarily make you money, but it will stop you from buying something you don’t understand.

This article focuses primarily on non-transactional tokens, the bulk of which represent Chain Street protocols. These are pseudo-equity tokens that, if designed correctly, can, through code-enforced mechanisms, pass value to token holders.

The Business of Chain Street

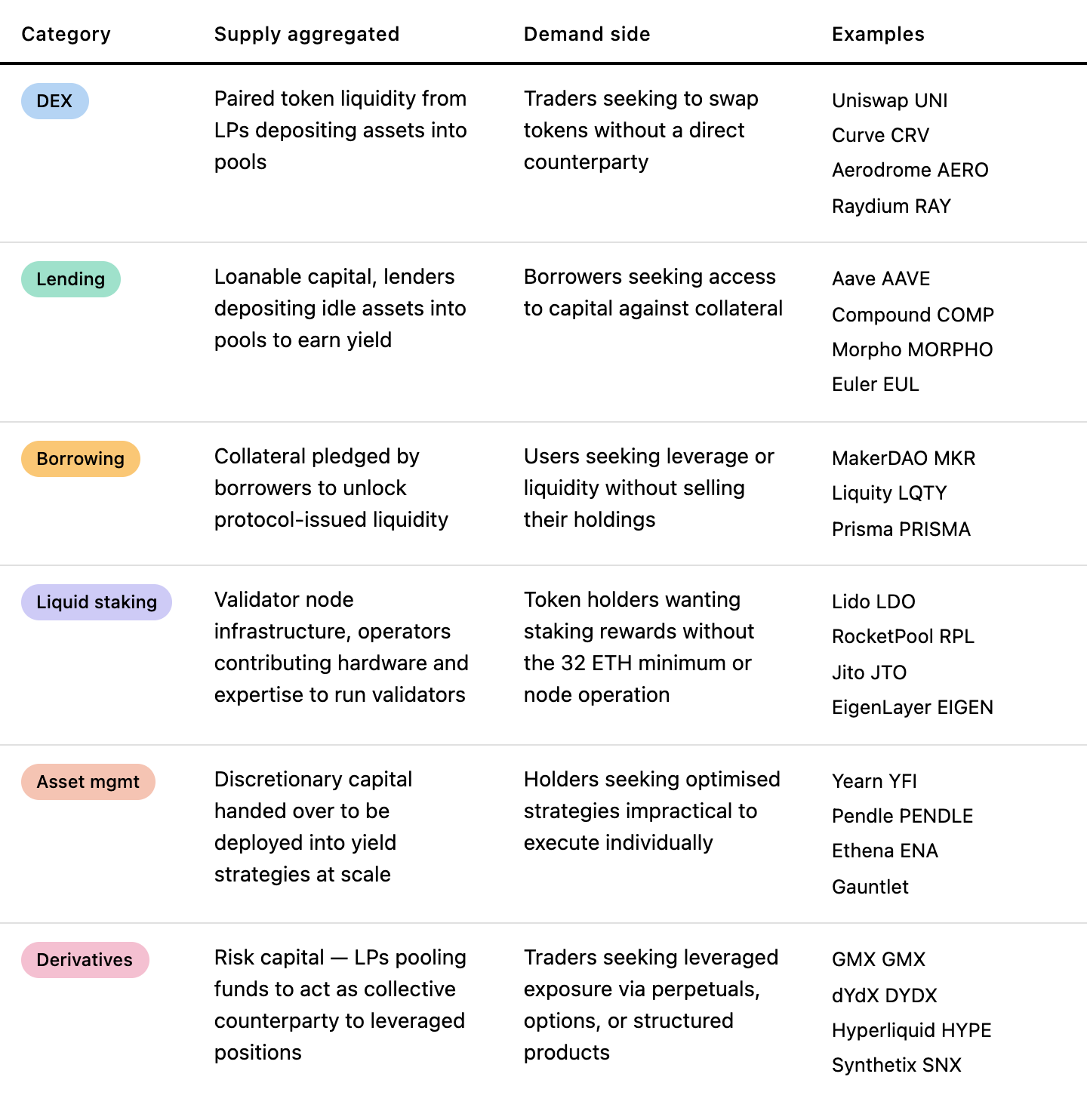

A quick 101 on protocol business models. Most of Chain Street’s protocols are double-sided marketplaces. Each protocol aggregates supply to service demand.

A vending machine is a useful conceptual comparison here.

A vending machine aggregates a supply of chips, cold drinks and chocolate bars from various suppliers. People walk by and, every now and then, grab a snack. The total sales are the vending machine’s fees, accumulated in its money box. The vending machines’ first line of costs is to pay on the supply side, the providers of chips, cold drinks and chocolate bars, this is the vending machines’ supply side fees. What is left is the vending machine’s revenue, and what is paid out to the vending machine’s owners is the owner’s revenue.

A vending machine is a real-world protocol. Put some coins in, select the item you want. The machine checks whether the supplied coins are greater than or equal to the product’s value. If so, the rules require giving the client the product. It’s a machine that follows basic IF, AND, and OR logic. It’s a physical embodiment of a smart contract.

With a couple of different words, that is exactly how chain street applications work. These applications are not in the business of selling snacks, they are in the business of exchange, lending, borrowing, derivatives, asset management and liquid staking.

At the core, Chain Street protocols are capital aggregators. What varies is the function that capital performs: market-making, lending, collateralisation, validation, strategy execution, or risk absorption. On Chain Street, the difference between Uniswap and Aave is what’s stocked on the shelves, not the fundamental mechanics of aggregating supply to service demand.

The point to drive home is that, like a vending machine, chain street protocols aggregate a supply and charge a fee for every interaction.

Revenue Waterfall and Holders Revenue

Value flows through a chain street protocol much like it flows through a vending machine.

Quantity of chips and cold drinks sold —> Total Sales —> Supply side costs —> Vending Machine Revenue —> Owner Revenue

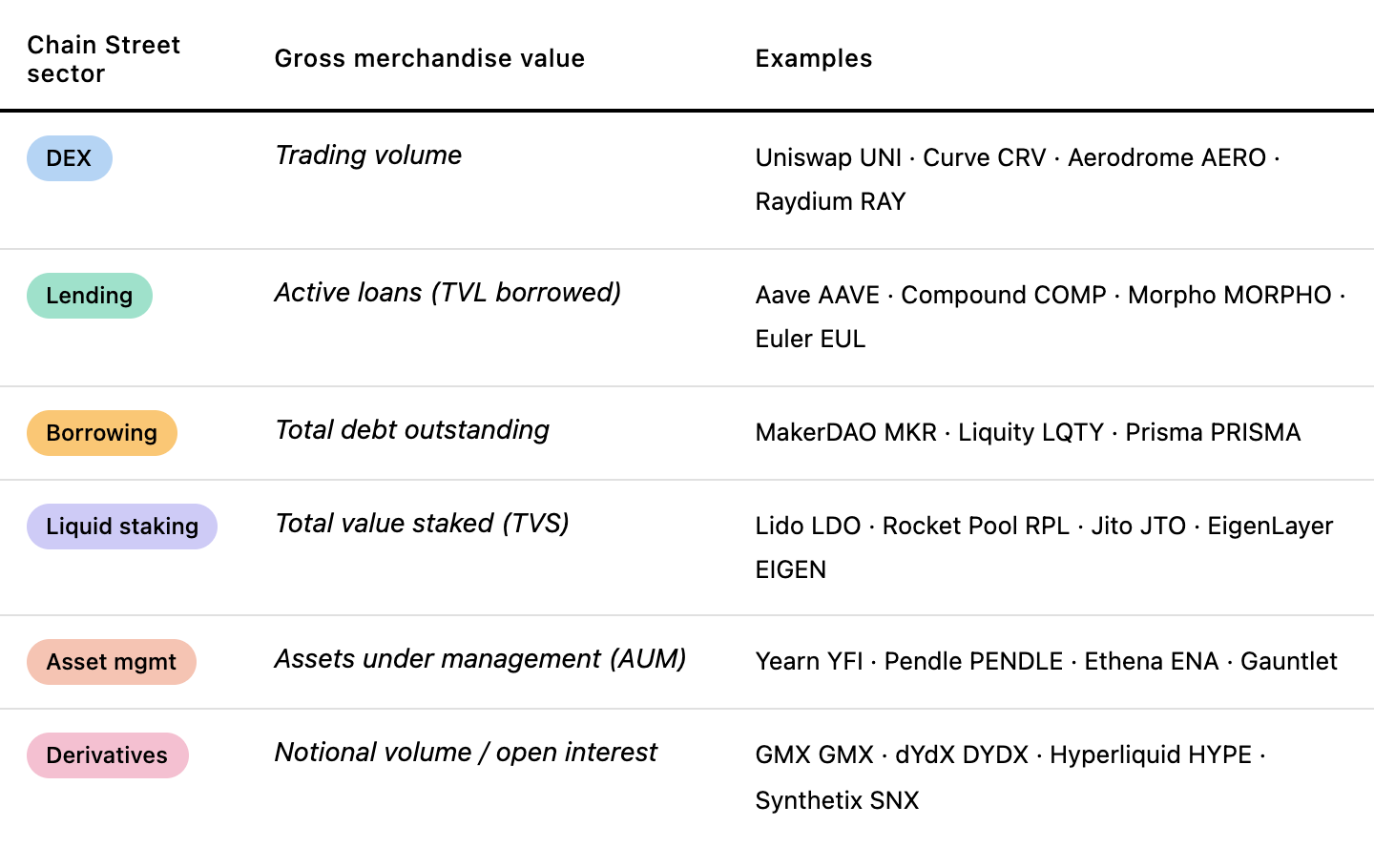

Gross merchandise value —> Fees —> Supply Side Fees —> Protocol Revenue —> Holder Revenue

The function each Chain Street sector serves differs, and therefore its core gross merchandise value metric changes accordingly. This is the driver: all else being equal, increasing GMV leads to higher fees, which lead to higher protocol revenue, and, if structured correctly, increased holder revenue.

Growing gross merchandise value drives higher fees, but top-line fees don’t tell us much and, in many cases, understate current valuations. As investors, we want to know what’s in it for tokenholders. Well-designed tokens reward tokenholders, they have good token rights. Poorly designed tokens don’t reward tokenholders and force us to ask, “why am I even holding this?”.

We don’t want governance tokens loosely tied to the success of a protocol; we want token rights, tokens whose value is directly tied to the financial success, traction, and network effect of the underlying protocol.

What’s in it for Token Holders

This section is here to help you distinguish between protocols with sound token rights versus those with poor token rights, this is a design feature. This is important because Chain Street applications are not encapsulated within business structures, nor do they confer legal claims to the assets or revenues of the underlying company.

The only claims that can exist on Chain Street are those that are code-enforced and programmatically distributed as a dividend, a buyback or a token burn.

Protocol Take Rate

Protocol Revenue/Fees

The protocol take rate allows us to assess what percentage of top-line fees are captured by the protocol itself. Aave, for example, does $580m in annualised fees, but only captures 13.5%, the rest is returned to Aave’s supply side, the lenders. Aerodrome and Hyperliquid, on the other hand, capture the majority of top-line fees into protocol revenue. Morpho, an early-stage lender, captures no protocol revenue as they are optimising for bootstrapped early-stage growth, focusing more on aggregating a sustainable supply of capital than on capturing value. SKY (formerly MakerDAO), the issuer USDS, sits in the middle, capturing 48% of top-line fees as protocol revenue. Compound stands out here, capturing only 3% of fees as protocol revenue.

Holder Take Rate

Holder Revenue/Protocol Revenue

Protocol take rates tell us one part of the story, but what’s most important to us as investors is the Holder take rate, the portion of protocol revenue returned to us as tokenholders. Again, we can see different approaches. Morpho generates no holder revenue, it’s too early stage to be returning capital to tokenholders. Aave, Aerodrome and Hyperliquid pass through almost all protocol revenue to tokenholders as holder revenue. Sky and Maple Finance only return a portion of protocol revenue to tokenholders, the rest is internalised into the protocol itself and allocated at the discretion of DAO voting. Compound displays further poor token design here, as zero protocol revenue is captured as holder revenue. Unlike Morpho, Compound is a Chain Street OG that has been around for a long time and is past its bootstrapping days.

Outstanding FDV to Holder Revenue (P/HR)

Outstanding Fully Diluted Value/ Holder Revenue

This is the multiple that matters to you as a Chain Street investor. P/HR is the closest thing crypto has to a price-to-earnings ratio. Remember, tokens do not confer legal claims over revenue internalised into the protocol, what the DAO decides to do with this surplus may not be beneficial to the protocol or tokenholders. More importantly, using price-to-fee (P/F) or price-to-protocol revenue (P/S) ratios may understate how expensive a token is.

This is true for all tokens covered in this short list. Aave’s P/F suggests it is trading at a 3.3x, but when we adjust to using Holder revenue, again, what we as token holders are entitled to via code-enforced mechanisms, the multiple is closer to 25x, an 800% understatement. The problem is even worse with poorly designed tokens like Compound. P/F at 10.6x may seem appealing, but none of that passes through to us. On a P/S basis, the Compound is trading at 349x.

Future Dilution

Outstanding FDV / FDV = Outstanding Supply / Max Supply

This ratio shows the percentage of the total max supply that has already been minted/issued.

(100%) → All tokens already exist, no future minting dilution

(60%) → 60% minted, 40% still to come

(20%) → Early stage, 80% of the supply hasn’t been created yet. These tokens carry high future dilution risk.

Early-stage protocols leverage ongoing token emissions and supply unlocks to attract capital and reward early community members and core team members. Supply-side emissions can be thought of as ongoing customer-acquisition costs and unlocks, as Chain Street’s equivalent of stock-based compensation. Both of these dilute existing token holders.

I wouldn’t completely write off a token because it has dilution as a headwind but it does help add context to how a token is priced. Aerodrome, for example, is the cheapest on P/HR basis but only has 49% of tokens in circulating supply, its compressed multiple is warranted as investors don’t want to get dumped on by liquidity farmers or the team’s token unlocks. SKY and Aave present a more mature picture, with almost all tokens issued and multiples that reflect high growth expectations for Chain Street’s blue-chip protocols.

Hyperliquids multiple tells a different story: its growing success and narrative as the everything exchange commands a steep P/HR multiple of 40x, yet there is much dilution ahead. Hyperliquid is also unique among the assets covered here, as it is the only transactional token in the mix. Hyperliquids primary success is its derivatives and spot platform, but sitting behind that is a blockchain of its own. This could explain the elevated multiples as blockchains tend to trade at significant premiums to protocols.

Some Guidelines to Keep you on the Right Side of Token Rights

I personally stick to Chain Street protocols with evidence of growing GMV. I take this further by narrowing the investable universe down to protocols that exhibit market power, clear dominance in their peer group.

No protocol revenue or holder revenue implies no value flows back to you as the tokenholder. I don’t want to hold these. Perhaps a vote to turn on or increase holder revenue take rates could present an opportunity.

I don’t automatically write off tokens with high future dilution; they may still be bootstrapping the protocol and using those tokens to acquire new customers. You need to be confident that the dilution will be worth it though, ongoing emissions and unlocks could trigger a market event that causes the token price to fall as new supply comes to market.

A Tool For Our Readers

I have put together a screener that will help you screen through some chain street protocols, and compare them on protocol revenue take rate, holder take rate, holder revenue multiple and future dilution. You can find it here.

Please remember, this is just a screener, it’s just a tool. Always do your own research.

Chain Street Cash Machines

In Chain Street Part 4, The DeFi Mullet, I explained that Chain Street Protocols have two paths ahead of them.

Path 1 is foundational, indispensable infrastructure, but unable to capture that value, like TCP/IP. - Commoditised Infrastructure.

Path 2 is invisible infrastructure to the end user but captures enormous value through usage-based fees, like AWS. - Cash Machines.

It’s obvious, even after 5 minutes of research, that Chain Street Protocols are usage-based and charge fees. What’s not obvious is how that value flows to us as tokenholders. This is the piece of the puzzle that matters most to us as investors and helps us distinguish between tokens with code-enforced rights and those without.

I believe path 2 is inevitable, and I am actively fading the calls for commoditisation. The game on Chain Street is one of the winner-takes most. The winners will be protocols that develop defendable network effects and transform a financial service from a company into an always-available fee-based protocol. It’s the network effect that drives market dominance and preserves its role as the best place to lend, borrow, exchange, stake or trade derivatives. You can’t fork a network effect, you can’t fork liquidity.

As I walk down Chain Street, I am looking for these protocols, these cash machines that will power the next chapter of finance.

While it’s easier to look away, seeking to understand is the only path to a more enlightened and empowered world. Change is now exponential and blockchain technology sits at the centre transforming money, finance and what it means to sovereign. Join me in exploring this new world by subscribing.

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments. Collective Investment Schemes (CIS) are generally medium to long term investments. The value of participatory interests may go down as well as up. Past performance, forecasts or commentary is not necessarily a guide to future performance. As neither Lima Capital LLC nor its representatives did a full needs analysis in respect of a particular investor, the investor understands that there may be limitations on the appropriateness of any information in this document with regard to the investor’s unique objectives, financial situation and particular needs. The information and content of this document are intended to be for information purposes only and should not be construed as advice.