Blockchain and Africa

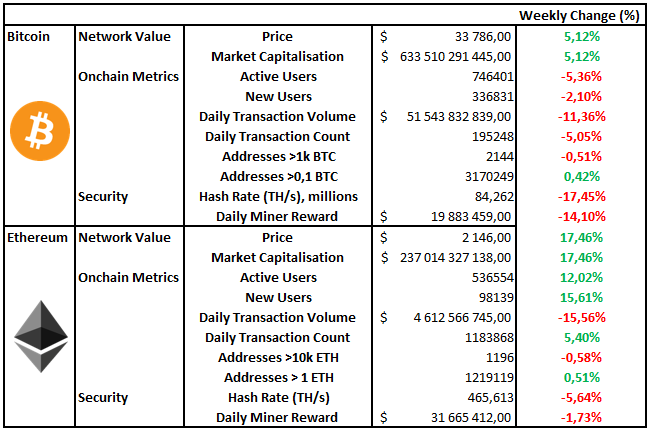

Market Recap

A Better Week For Digital Assets

Blockchain and Africa

According to Oxford, blockchain is a foundational technology. Similar to how the internet created a new foundation for disseminating and using the information in society, blockchains pose an opportunity to transition to a new means of communicating, accounting for, and executing transactions of value. Some countries and continents stand more to gain than others by adopting this technology, namely third-world countries. This is generally because they lack access to robust financial networks and low-cost contractual agreements.

It is projected that by 2100 five of the largest ten countries in the world will be in Africa; the need to create an economic and legal system where people can thrive is paramount.

But how can blockchain enable this?

What are blockchains?

Blockchains at their most basic are a new type of settlement infrastructure. They can process, execute and settle transactions and basic conditional agreements known as smart contracts. They are global systems, and all that is required to access them is an internet connection. This makes them extremely powerful in providing access to those who previously could not access financial networks or those who could not trust the current infrastructure in place to function as expected. When the latter happens, the ability to conduct business becomes prohibitively expensive and severely inhibits an economy's growth potential. Let's look at Africa's current state of infrastructure to understand precisely where blockchain can be used.

Current State of Infrastructure

Many third-world countries across the globe do not have robust economic and legal infrastructure in place. None so much as Africa, which leads to poor economic growth, widespread corruption, and a lack of accurate record-keeping systems, which means it can become problematic for people to prove what is theirs.

For capitalism to thrive in Africa, we need to establish systems that help enforce property rights; without robust property rights, capitalist ideas can quickly become controlled and abused by those in power.

Unbanked

According to the World Bank, there are around 1.7 billion people that are unbanked across the globe. This includes people who either don't have access to traditional banking infrastructure or use mobile money payment solutions.

In Sub-Saharan Africa, around 80% of the population are unbanked. Even with the rise of mobile money solutions like the M-Pesa across the continent, there still remains a lot to be desired. Blockchains can help create efficiencies that these centralised money solutions cannot. This is achieved by transitioning from brand-based trust systems held together by recourse deterring guarantees and enforced by weak legal codes to a universal math-based trust system. This will bring transparency, efficiency, and the reduction of costs in both transactions of value and contractual agreements.

If you look at the current state of the remittance market in Africa, it is not uncommon to be paying around 20% of the value of your transaction when sending money back to your family. As more people start leaving their smaller towns to work in the bigger cities, the demand for remittance services will grow. These people need a low-cost alternative that will give them peace of mind and not absorb a large portion of the value they want to give to their families to put food on the table.

Cost of contracts

"the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment in the Third World." - Douglass North

Why is this true? Well, how does one conduct business if you cannot trust the other party to honour an agreement? This creates massive friction when conducting business and incentivising investment. Therefore, if there was a globally accessible settlement and record-keeping system, the ability to conduct business and trust all parties involved significantly reduces these frictions. This, in turn, inspires further growth creating a virtuous cycle.

The World Bank has conducted studies on both what it costs to enforce contracts as a % of their claim value and how long average resolution takes across the globe. These are already high, even in developed markets. For example, in Australia, it takes 402 days on average to settle a contract dispute and around 23.2% of the cost. However, in Sub-Saharan Africa, that goes up to 654.9 days and 41.6% of the contract value.

Contractual enforcement is also only as good as the records used to dispute an argument. Having a robust record-keeping system also opens up other economic possibilities. As an example, 90% of the land is undocumented or unregistered in rural Africa. The community in these areas generally has a "mental ledger" who owns what, but this isn't good enough for a financial institution. This means that they cannot use this land as collateral if they wanted to borrow against it or sell it to anyone outside of the community or people keeping the "mental ledger". The ability to accumulate assets and then leverage those assets to further grow ones wealth can be hindered.

54 Sovereign States

Africa has a population of 1 374 114 971, split between 54 sovereign states with their own economic, political and cultural systems. This creates massive complexity when it comes to conducting business between countries, especially ones that lack an infrastructure that all parties can agree on. There have been talks and ideas to implement an African Union similar to Europe, but the current economic and legal systems make it unfeasible because we cannot manufacture enough trust between countries. Therefore, a shared protocol like Ethereum could inspire enough trust to start conducting business across the continent. If leveraged, the ability to participate in the entire African Union's economic activity will be contingent on an internet connection and a smartphone.

Imagine the possibilities for investments that may open. We can exchange and transfer value seamlessly across borders and manufacture trust where it was too expensive to have before. Africa has generally been too risky to make investments into because the ability to understand where your money was going and how it was being spent relied on trust manufactured by centralised institutions, who generally have quite the track record of abusing trust. Blockchains and apolitical settlement systems can bring transparency to African investments and guarantee that funds cannot just be seized or censored by authoritarian governments. Where brand based trust has failed in Africa, we can now replace it with the guarantees of math.

But is it being used?

Blockchain is already finding practical use by people and countries across Africa, albeit it is a small number or still in beta stages. Some are leveraging private blockchains and some public. However, what has been emerging is that it is creating these efficiencies that blockchain promises. There are people such as Abolaji Odunjo, who owns and runs a small business selling mobile phones in Lagos that have made the decision to start paying his Chinese suppliers in bitcoin. According to him, this has allowed his company to boost its profits as he no longer has to use Nigerian naira to purchase dollars and can avoid the high cost of remittance.

"Bitcoin helped to protect my business against the currency devaluation, and enabled me to grow at the same time." Abolaji Odunjo

Overall, blockchain has the ability to manufacture trust and provide the necessary infrastructure for Africa to flourish. The supporting technology that will enable it is being built out as we speak, penetration of smartphones is at an all-time high and constantly increasing. Projects like Starlink will also provide high-speed internet where there is none. For the first time, Africa may have the ability to form an economic union that could rival even America and Europe.

Notable Articles and News Stories This Week:

George Soros' Investment Fund Has Reportedly Started Trading Bitcoin

George Soros, otherwise known as the man who "broke the Bank of England," has reportedly started trading Bitcoin. Soros Fund Management's chief investment officer Dawn Fitzpatrick had given "the internal green light to actively trade Bitcoin."

It still remains to be seen how or what they will do with this opportunity; however, it will probably affect the markets in some way significantly. It is interesting to see how institutions attitudes are changing towards the asset class and the different reasons and ways they are using the assets to create returns.

Read more about it here

Germany's New Law Means 4,000 'Spezialfonds' Can Now Invest In Bitcoin

Germany's 'Fund Locations Act' came into force today, meaning that thousands of institutional investment funds will now be eligible to invest in Bitcoin and other cryptoassets for the first time. Spezialfonds are favoured by institutional investors, and the new law allows fund managers to allocate up to 20% of a Spezialfond to cryptoassets.

These Spezialfond's currently manage around $2.2 trillion, and therefore and allocation may have favourable effects on the market.

Read more about the new law here

Binance Not Authorised to Operate in the Cayman Islands, Says Regulator

The Cayman Islands' financial regulator has joined a list of watchdogs globally that are scrutinising Binance and its business dealings. "Binance Group and Binance Holdings Limited are not registered, licensed, regulated or otherwise authorised by the Authority to operate a cryptocurrency exchange from or within the Cayman Islands," the islands' Monetary Authority said in a press statement Friday.

This comes on the back of regulatory pressure on cryptoasset service providers from countries and governments across the globe. This can be seen as positive as it should give investors and users of these services greater confidence.

Read more about the decision here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.