Decentralised Synthetic Assets

Decentralised Synthetic Assets

Market Recap

DeFi Leads The Pack

Decentralised Synthetic Assets

Blockchains have ushered in an era of accessible, inclusive, and expressive financial services. There are multiple subcategories within the DeFi movement, from spot exchanges, lending and borrowing to derivatives, also known as synthetic assets. One of the most significant opportunities in DeFi is a decentralised synthetic asset protocol. This facility would allow anyone with an internet connection to gain exposure to any asset without physically settling the underlying.

Multicoin Capital, in an essay titled "Trade-offs in the Decentralised BitMEX Space", outlines why the idea of a decentralised synthetic asset exchange is appealing; here are the main points they made:

No centralised exchange operator, therefore lower fees in the long run

Permissionless access across borders

Censorship resistance such that no one can shut down the exchange

No counterparty risk because users hold their own funds

No withdrawal limits and/or trading size limits

No way to change the rules of the exchange unilaterally

Any asset with a public price feed can be traded

We have seen multiple attempts at creating a decentralised synthetic asset platform, all of which have taken different routes to solve the same problem. You can check out Synthetix, the current leader in the space or UMA, Mirror Protocol, or Injective Protocol. All of these projects are exciting and have grown tremendously since their genesis. Summarised below are the pros and cons of each design choice outlined in Multicoin's essay.

Today there is a new and novel design emerging, pioneered by Float Capital. One which we believe solves some of the most pressing issues faced by synthetic asset platforms. The rest of today's article will be dedicated to exploring Float Capital in more detail.

Float Capital has set out to create one of the easiest and most efficient ways to gain both long and short exposure to any asset. Core to the design choices that the engineers at Float have chosen is to no longer have liquidations, no more over-collateralisation, no front running and no trading fees. This is no small feat, and the solution they have produced is truly elegant.

How Does Float Capital work?

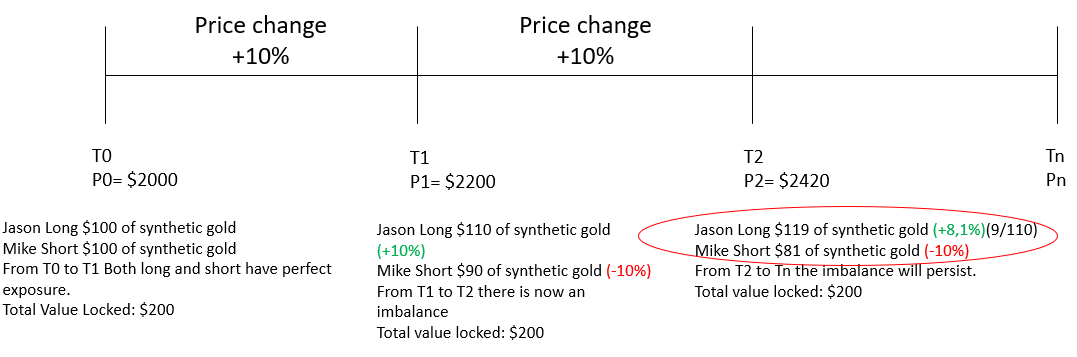

A user can mint (take a position) either long or short tokens for any asset listed on Float. This would require the user to convert ETH or DAI for a synthetic long or short token (ERC-20). Float then creates a zero-sum game between the long and short tokens where gains by longs are losses for shorts and vice versa. The problem that arises from this design choice is that the protocol could experience large imbalances between longs and shorts, meaning that one side of the trade no longer has "perfect exposure". I.e., for every % change in the underlying, the synthetic asset value changes by the same %, this exposure actually floats between 0-100% of the underlying's price change.

You can see how at T1, this imbalance creates a situation where the long exposure is reduced from 100% at T0 to 81% ($90/$110) at T1; this is the floating exposure element of Float Capitals design. This obviously begs the question as to how Float will reduce this exposure shortfall. Most synthetic asset platforms utilise over-collateralisation to make up for imbalances between longs and shorts, Float's approach is very different.

This is where Float's "yield manager" contract comes in. The yield manager takes the ETH or DAI used to acquire a synthetic token and puts it into a lending protocol. At the moment, Float Capital utilises Aave as its decentralised bank for its collateral; however, its contracts have been written in such a way that they could extend this to other protocols such as Compound or even optimised yield aggregators such as yearn.finance.

Once the collateral hits Aave, it starts to earn interest. This is where the genius of Float Capital comes in and what we find so elegant about its design. Instead of requiring users to be and remain over collateralised, the interest generated in Aave is used to balance out imbalanced markets.

There are two splits that the yield manager contract will perform here.

Split between markets and float treasury- in the event that markets in general on Float are balanced, then a higher portion of the interest earned will go to Floats treasury for later use by the community. However, the opposite is true when markets are very imbalanced; in this scenario, the majority of interest will be directed to markets to bulk up liquidity where it is needed the most.

Split between long and short sides- this split comes after the first split and ensures that interest is directed to the side of the market where the imbalance occurs.

In an attempt to further stabilise and balance these markets, Float also has a staking contract. Once you have bought your synthetic asset, you can stake it in the staking contract and earn FLT. The staking contract may not be for everyone, but if you want to earn the FLT token (Floats native token), you will need to stake. The amount of FLT you earn depends on how much you are staking as a proportion of the entire network and how long you decide to stake it for.

This incentive creates a scenario where token holders or interested participants can earn FLT tokens by helping correct imbalances in Float Capital markets. Imagine a scenario where the Float Capital community members actively help in essentially making markets by providing liquidity and participating in this zero-sum game.

The more balanced long and short markets are, the more interest is generated on the collateral, and therefore, more will be allocated to the treasury. The bigger the treasury gets, the more valuable the ability to govern the use of that treasury becomes and, therefore, the more valuable the FLT token becomes. In addition to this, Floats treasury has another revenue stream in the form of a fee charged when a staker redeems their staked synthetic asset.

At no point in time as a user will you have to worry about whether you will be liquidated or otherwise stare aimlessly at your computer in an effort to manage your collateralised debt positions. Additionally, there are no fees charged on making trades; the only fee is for unstaking a synthetic asset.

The last feature that we find really interesting about Float Capital is how they have tackled front running. Front running in DeFi protocols can occur due to stale data from oracle systems; you can read an article we did on oracles here.

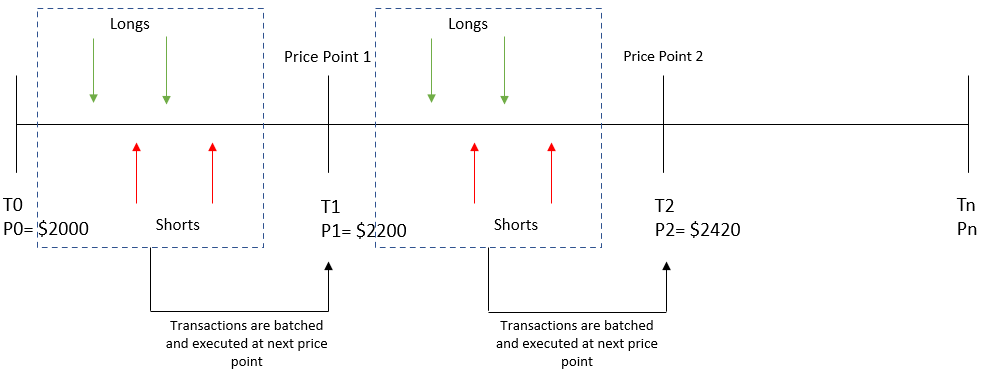

Depending on the feed or oracle system, price updates can range from 30 seconds to 5 minutes. Front running can occur if a user knows the underlying asset's price before oracles report these prices to a protocol like Float Capital. Let's assume the theoretical example of an Elon Musk tweet. Elon makes a Tweet just after T0. Dave, the day trader, sees the tweet, rushes to Float Capital to make a trade and executes it at the price of T0 because it's the last available price given before the oracles update. Meanwhile, the price has already adjusted significantly, and Dave has managed to get a much cheaper price, essentially front running the Float Capital system.

Float Capital engineers have solved this problem by utilising next price execution. This works by allowing traders to place orders between price points but only executes these orders using the next available price.

Float Capital's unique approach to synthetic assets will put it in a class of its own. It offers a straightforward means by which everyday individuals can gain exposure to any asset on the planet. We are blown away by the sheer amount of original thought and hard work that the team at Float Capital have put in. Not only is the service offered by Float Capital useful for many people, but they have also paid careful attention to the internal tokenomics of FLT token.

We look forward to participating in and watching the growth of this exciting venture going forward. If you would like to get involved with Float or have any questions for the team, you can find them here:

*Please note: Float Capital is in Alpha phase of development and will be using the next weeks to refine what they have created. At the time of publishing, the Etherbridge team is actively participating in Float Capital markets and staking synthetics to earn “alphaFloat” token. Participating in early stage projects like Float Capital carries risk that you should assess for yourself before contributing any meaningful capital.

Notable Articles and News Stories This Week:

Revolut Is WeWork’s First Enterprise Member to Pay for Office Space in Bitcoin

Office-sharing giant WeWork said that U.K.-based digital bank Revolut has become its first enterprise member to pay for office space using cryptocurrency.WeWork said Revolut will use bitcoin to pay for its 300-employee office space at a WeWork site in Dallas, its largest office in the U.S. The office space provider first began accepting cryptocurrency as payment in April, with Coinbase paying for its membership with crypto. “We’re excited to continue on our rapid growth trajectory with an innovative partner like WeWork that affords us the flexibility to pay using cryptocurrency – a technology whose future we vehemently believe in – as Revolut expands in the U.S. and around the world,” said Rhebeckha D’Silva, Revolut’s global head of real estate.

Read the full article here

Solana Recovers After 10-hour Outage

This week the Solana blockchain suffered a major outage, which ultimately forced a network restart following a hurried bug-fixing upgrade, to curtail uncontrollable forking of the chain. Although still technically in beta, the protocol’s growing DeFi ecosystem has amassed nearly $11 billion in total value locked, and Solana has also tapped into the latest NFT mania, propelling its $SOL token into the top 10 by market cap at over $47 billion. A patch was released Tuesday afternoon, requiring the community of validators who operate the network to coordinate a software update and restart the chain, a process which was completed early Wednesday, according to the Solana Foundation.

Read the full story here

Evergrande Is Suspending Trades Friday, Here’s What That Means

Hengda Real Estate Group Co Ltd, the parent company of China Evergrande Group, applied on Thursday to suspend trading of onshore corporate bonds. Historically, this move is likely to be followed by a restructuring or default. Chinese authorities alerted Evergrande’s major lenders that the property developer giant may default on interest payments due September 20, Bloomberg reported Wednesday. Evergrande, which has been cash-strapped for months, is sitting on about $300 billion in debt, making it the most indebted developer in the world. The situation has led to intensifying protests across China as investors, homeowners and buyers are left with unpaid debts and unfinished properties.

Read more about the situation here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.