Crypto: A New Asset Class

Crypto: A New Asset Class

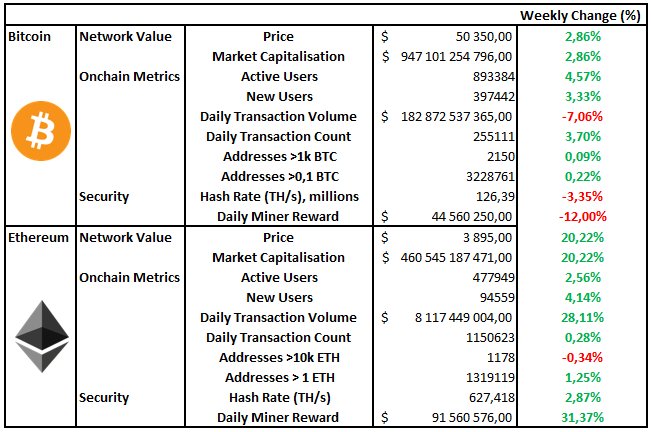

Market Recap

Ethereum Leading As Crypto Moves Upward

Crypto: A New Asset Class

In the early days of bitcoin, the industry made a grave mistake; they bundled all the projects together and dubbed them "cryptocurrencies". The term cryptocurrency has hindered the space more than any event, hack or uninformed opinion out of Wall Street. It assumes that everything in crypto is attempting to become a global currency; this couldn't be further from the truth. This weekend we will discuss what an asset is, our traditional asset classes and why, in fact, crypto can be viewed as its own class of asset.

What is An Asset?

According to Wikipedia, in financial accounting, an asset is:

"any resource owned or controlled by a business or an economic entity. It is anything (tangible or intangible) that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash (although cash itself is also considered an asset). The balance sheet of a firm records the monetary value of the assets owned by that firm."

The Oxford dictionary defines an asset as:

"a useful or valuable thing or person" and "an item of property owned by a person or company, regarded as having value and available to meet debts, commitments, or legacies."

So the definition of an asset is pretty open-ended; an asset can be anything of value that a person or entity can own. It can be both tangible or intangible, and most importantly, it can be exchanged for money or something else of value. Chris Burniske, a prominent name in early-stage financing of blockchain-based projects, released a paper called Bitcoin: Ringing the Bell For a New Asset Class, where he outlined what he calls Superasset classes.

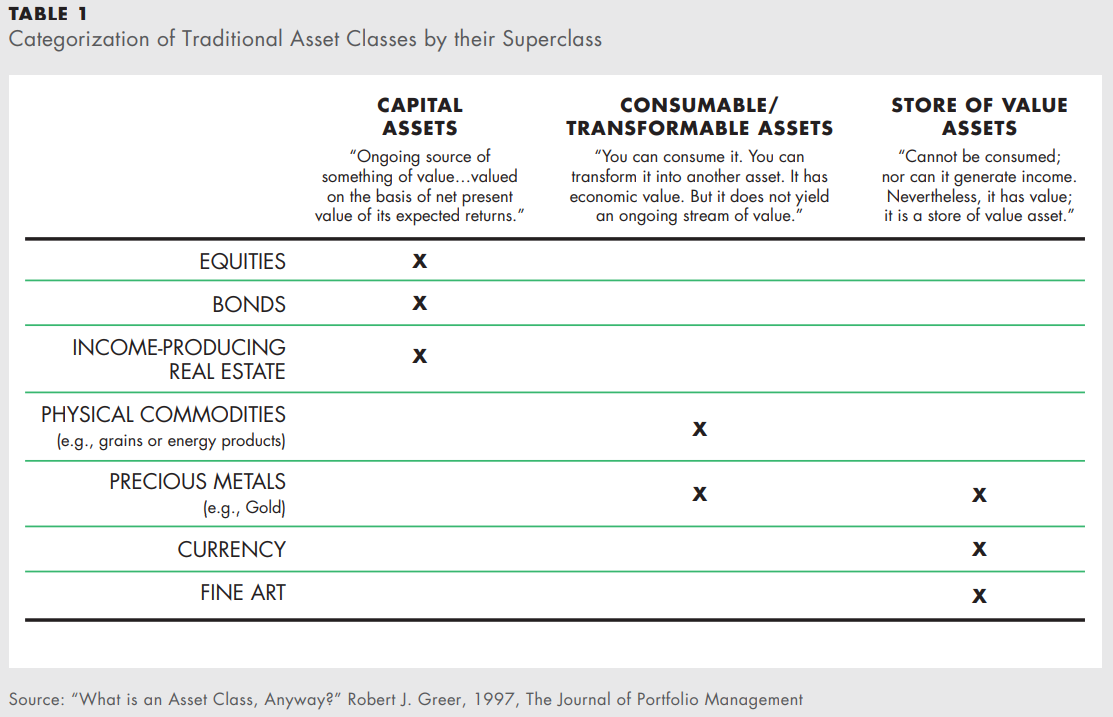

Chris outlined three distinct asset classes of the traditional world:

Capital Assets

Capital assets represent things you can own that have the ability to produce a value flow. Examples of capital assets are property, stocks and bonds. These assets produce value flows in the form of rents, dividends or interest. They are easy to understand and are usually valued based on the net present value of expected returns.

Commodities

Commodities are things that can either be transformed into something of value or consumed in the process of creating something of value. Examples of commodities are precious metals, wheat, oil or even data. These assets aren't as easy to value as their market value is constantly discovered through changes in supply and demand.

Stores of Value

These are the strangest assets of all the superasset classes. They do not produce a value flow for holders, nor can they be transformed into something of value. They have value primarily due to their perceived rarity and uniqueness. Examples of these include art and collectibles.

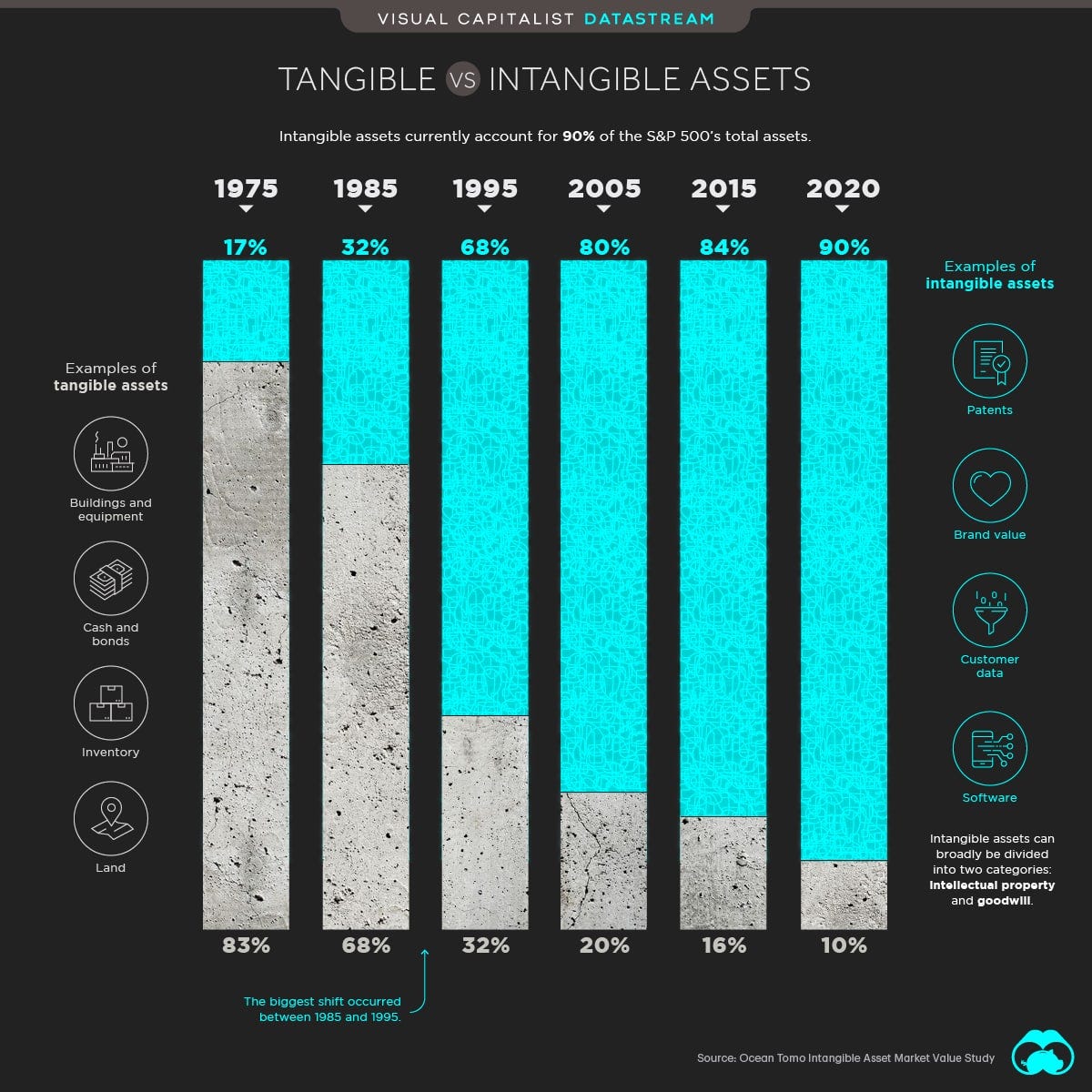

Cryptoassets are confusing to many primarily due to their intangible nature, which is surprising considering 90% of the market value of S&P500 stocks is intangible. A theme that started in the mid 70's when software began eating everything. Software together with cloud computing give these new-age businesses competitive advantages over their analogue alternatives; this theme is not new. Think about what Apple and other smartphone companies have done to calculators, calendars, photo albums, notebooks and map books, to name a few. They create these digital equivalents of real-world goods or services and then issue them to their users at zero variable cost. Within minutes, these services can be upgraded and made increasingly intelligent. A smartphone has replaced the need to go to separate places to accomplish any specific goal, from shopping to financial services. Even our raw commodities are changing, increasingly being code and data generated primarily by us on smart devices.

Another aspect that blurs the lines of recognising cryptoassets as assets is that whilst some cryptoassets are either capital, commodity or SoV in nature, some even represent a blend of these super asset classes. There are currently no valuation frameworks to understand assets like these, in the same way that there was no reliable, commonly understood and respected valuation methodologies for equities for at least 200 years after their genesis.

Bitcoin

Right now, you might be thinking about what kind of asset is bitcoin. Bitcoin, the asset, is a commodity on the Bitcoin network; you cannot use the Bitcoin network without paying for your requests in bitcoin. So the asset is essential to the functioning of the network itself. Like other commodities, bitcoins value is determined through supply and demand for bitcoin. Bitcoins supply is unlike other commodities in that it is completely impervious to changes in demand for bitcoin; you can read more about this in a previous article we did here.

Bitcoin is meant to be boring; it is built primarily for survival. We expect it to continue being a raw digital commodity.

Ethereum

Right now, Ethereum is also just a commodity. In the same way you need bitcoin to pay for requests on the Bitcoin network, you need ETH to pay for transactions of value on Ethereum. However, unlike bitcoin, these transactions are broader in terms of functionality; they could represent a payment, a loan agreement, payment for digital art, or investment into an index. With the introduction of EIP-1559, a much-anticipated improvement proposal, ETH is now actually "burnt" when used to pay for transactions. Every time you use Ethereum, you pay gas, which is made up of the base fee and a tip. The base fee is what gets "burnt" or removed from the circulating supply.

Ethereum is in the process of another upgrade that will affect both its capabilities as a technology and its characteristics as an asset. Once Ethereum successfully transitions to Proof of Stake, it will develop capital like properties as users will be able to stake their ETH in the system and earn a yield for doing so. This yield comes in the form of new issuance (inflation) and tips from processing, executing and settling transactions for users of the Ethereum network.

A successful transition to Ethereum 2.0 will make Ethereum one of the most exciting assets we have ever seen. It will be what David Hoffman describes in his essay Ether: A Triple Point Asset.

DeFi

This is where the handle "cryptocurrencies" falls short. These projects and financial primitives are not trying to become currencies. In the 2017 ICO boom, there was a lot of attention on the concept of utility tokens. These tokens were designed to be used as proprietary payment mechanisms, for example, take the theoretical idea of Music Network. Music Network is a platform where artists can create and distribute music without intermediaries, which can only be paid for using Music Coin. This type of arrangement leads to inefficient value capture as there is no real incentive to hold this token; the only thing you need it for is to buy music.

DeFi assets are not utility tokens. They are quasi equity-like instruments that can pass value through to stakeholders that need it the most. The tokens of these DeFi networks are not currencies; they are capital assets. Most of the DeFi tokens we hold provide the owner with governance rights and/or claims on underlying value flows generated by the network. Each token passes value through in its own unique way; it's almost as if we are in the very early stages of new network-based business models.

Here is a mental framework for trying to wrap your head around this concept. DeFi networks provide a service, Uniswap is an exchange, Compound and Aave are lending and borrowing facilities and yearn.finance is an asset manager. For every exchange on Uniswap, a user must pay an exchange fee; for every borrow on Compound, 10% of the interest paid is collected by the protocol; and for every investment into a yearn.finance vault, management fees and performance fees are charged.

Pretty simple right? However, this is where it gets slightly complicated; usually, the money generated from these activities would pay off the businesses expenditures, and the rest would either be reinvested in the business or distributed to shareholders. DeFi assets are far more expressive than this; they can direct value flows in almost any way as long as the community is in agreement. These value flows can either be considered protocol revenue, supply-side revenue or demand-side revenue. Protocol revenue is as good as dammit retained earnings; the other two, however, are new paradigms only possible in stakeholder networks.

Here are some examples to help you better understand this:

Uniswap has no protocol revenue. All of the value flows produced by Uniswap (currently equal to exchange volume * 0,30%) are directed toward liquidity providers, or the Uniswap supply side. This is important because Uniswap needs to keep their exchange pairs liquid, so incentivising people to contribute assets and make markets creates a better experience for traders and users. Uniswap has done $54 billion in exchange volume and paid $112 million to liquidity providers in the last month. As a UNI holder, you are currently not entitled to a claim on these value flows; nonetheless, you do possess the ability to vote on changes to the protocol. We expect that just as early-stage businesses avoid paying dividends until they are sustainable and mature, Uniswap governance will do the same.

Aave has both protocol and supply-side revenue. For every loan originated on Aave, a borrower can decide between either a variable or fixed rate and to take out the loan is required to post collateral. 90% of interest earned is directed toward the supply side, people who deposit assets into various Aave markets to earn an interest rate. 10% of interest earned is protocol revenue which is automatically deposited into Aave's safety module. The safety module acts as a backstop for the Aave system as a whole.

In the event that Aave markets become under collateralised or otherwise insolvent, the safety module kicks in. Aave holders can stake their Aave tokens in the safety module to earn a proportional stake of protocol revenue and additional inflation (passive Aave holders earn no yield on the Aave they hold until staked). This carries risk because, in the event of insolvency, these stakers would act as lenders of last resort by recapitalising the system. This isn't the same as the moral hazard we see with central banking systems, where people with zero skin in the game are allowed to socialise losses by stroking their keyboards and printing money to fill the hole. In this system, the very people who vote on proposals, upgrades and strategic decisions put their capital at risk in the event their creation fails.

Yearn.finance possibly has one of the most interesting business models. It has been referred to as "buyback and build". We have seen the power of equity buybacks for a business like Apple, whose buyback value even dwarfs the market value of half the S&P500. Buybacks are just another way of returning capital to holders. When a user invests in a yearn vault, their money is put to work in various lending facilities; yearn charges users a classic 2% management fee and 20% performance fee on assets under management. These fees are all protocol revenue; they are directed to yearn's treasury. These collected fees are then used to buy back YFI on the open market. Then comes the "build" part of yearn's business model; the YFI tokens acquired in the buyback are allocated to people who are looking to contribute to the yearn ecosystem. Anyone can apply to make a contribution; it doesn't have to be technical, it could be anything.

Yearn's capital allocation seems optimal here; they charge fees for their services and use these fees to buy back tokens from YFI holders. They only pay new contributors in their network token YFI. The more revenue yearn produces, the more YFI they can remove from the open market to finance new projects. This does two incredible things, firstly it creates a constant demand for YFI; second, it takes YFI from weak investment hands and puts it into the hands of contributors and developers.

Concluding Thoughts

Cryptoassets are clearly a new asset class. There are commodities like bitcoin, capital assets like DeFi tokens and a new triple point asset, Ethereum. These networks offer similar benefits to assets of the past; they act as coordination mechanisms that people can use to create truly great organisations and networks. With the rise of a new asset class comes an enormous opportunity; if you have any thoughts on this or questions that need answering, please feel free to reach out to us.

Notable Articles and News Stories This Week:

SEC Boss Tells EU Parliament Crypto and Fintech Could Be As Disruptive 'As The Internet'

In a virtual presentation to the European Parliament, SEC Chairman Gary Gensler shared his policy recommendations regarding the regulation of cryptoassets. He emphasised the need for robust public policy frameworks that balances innovation and investor protections. He went on further to say that "I think the transformation we're living through right now could be every bit as big as the internet in the 1990s" and that crypto is, in fact, a "truly global" asset that "has no borders or boundaries. It operates 24 hours a day, seven days a week."

Read more of his comments here

Decentralised Search Engine Becomes Default Option on European Android Devices

From the first of September 2021, Presearch, the decentralised search engine, will be listed as a default option on all new and factory-reset devices sold in the United Kingdom and Europe. The decision by Google to list Presearch as a default browser option follows a protracted legal battle with the European Commission over accusations that the technology company used Android to solidify its search engine dominance. Presearch's private, decentralised search engine option will now be listed on Android devices alongside several other eligible search engines across Europe. Although the search engines will be listed randomly, Presearch may appear differently depending on the user's location.

Read more about it here

Japan's SBI Holdings to Launch Crypto Fund

Japanese financial conglomerate SBI Holdings Inc. aims to launch the country's first cryptocurrency fund by the end of November that can give individual investors a way to diversify their broader portfolio.

The fund could grow to several hundred million dollars invested in coins including Bitcoin, Ethereum, XRP, Bitcoin Cash, Litecoin and possibly others, said Tomoya Asakura, who oversees asset management for Japan's biggest online brokerage. Investors may need to put in a minimum of roughly 1 million yen ($9,100) to 3 million yen and it will mainly be aimed at people who understand risks associated with crypto.

Read about the announcement here

Whilst we all have the option to look, to seek to understand, it’s often easier not to. Bitcoin, Ethereum and distributed ledger technology are complex systems that require significant due diligence. At Etherbridge, we aim to lower the barriers to understanding this fast-growing digital economy.

If you are interested in staying up to date, please subscribe to our newsletter at etherbridge.co

This is not financial advice. All opinions expressed here are our own. We encourage investors to do their own research before making any investments.